Remote Sensing Services Market Size and Forecast (2025–2033), Global and Regional Share, Trends, and Industry Analysis Report Coverage: By Platform (Satellites, UAVs, Others), By Resolution (Spatial, Spectral, Radiometric, Temporal), By End-use (Commercial, Defense), and Geography

2025-12-23

Aerospace & Defense

Ekta Chaurasia (Team Lead)

Description

Remote

Sensing Services Market Overview

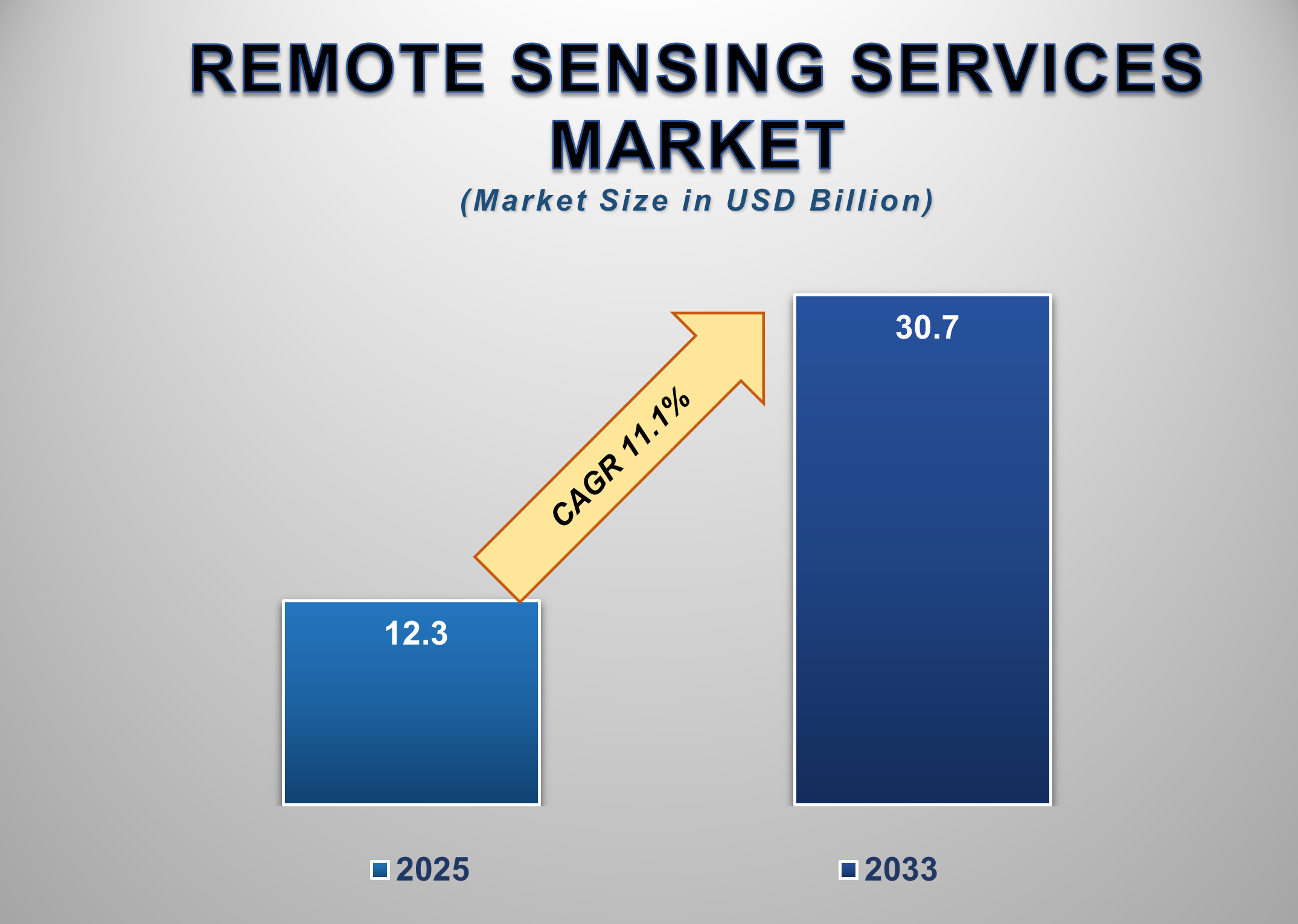

The Remote Sensing Services Market is witnessing rapid expansion as organizations increasingly depend on advanced imaging and sensing solutions to monitor assets, assess environmental conditions, enhance security operations, and support data-driven decision-making. Valued at USD 12.3 billion in 2025, the market is projected to reach USD 30.7 billion by 2033, reflecting a robust CAGR of 11.1% during the forecast period. Remote sensing has evolved far beyond traditional satellite imagery, expanding into UAV-based services, hyperspectral imaging, thermal monitoring, radiometric analysis, and AI-powered data processing. This shift reflects organizations’ growing need for precise, real-time geospatial intelligence across sectors such as commercial infrastructure, agriculture, defense, energy, and environmental management.

Increasing digitization, the

proliferation of high-resolution sensors, and greater affordability of

satellite constellations are reshaping how geospatial intelligence is generated

and consumed. Advancements in cloud computing and AI-driven analytics have

significantly increased the usability of remote sensing data, enabling faster

interpretation, automated classification, and predictive modeling for

industries. The commercial segment has become the largest end-use category,

driven by demand for urban planning, location intelligence, natural resource

monitoring, mining, and climate assessment. Simultaneously, miniaturized

satellites, reusable launch systems, and growing access to UAVs are making

remote sensing more accessible to small and mid-sized enterprises.

Remote Sensing Services Market Drivers and

Opportunities

Rising Demand for

High-Resolution Geospatial Intelligence Is Driving Remote Sensing Services

Market Growth

The rapid increase in demand for

high-resolution geospatial intelligence across commercial and governmental

sectors is a key driver for the Remote Sensing Services Market. Industries such

as agriculture, infrastructure, mining, utilities, environmental management,

and insurance increasingly rely on remote sensing data to optimize operations,

monitor assets, and improve decision-making. High-resolution imagery enables

precise mapping, real-time assessment of environmental changes, and accurate

detection of anomaly capabilities that are critical for ensuring operational

efficiency and regulatory compliance. For example, precision agriculture uses

spatial and spectral data to monitor crop health, moisture levels, and pest

activity, enabling farmers to reduce costs and increase yields.

Government agencies and

environmental bodies depend on remote sensing to track deforestation, assess

disaster impact, evaluate water resource distribution, and monitor

climate-related changes. With rising concerns around sustainability, remote

sensing has become a central tool for environmental audits, carbon stock

assessments, and land-use planning. The defense and security sectors are also

major contributors to market growth, utilizing remote sensing for border

surveillance, strategic planning, and threat detection. The ability to capture,

process, and analyze data in near real-time has significantly enhanced response

capabilities for homeland security and emergency services.

Technological advancements such

as the proliferation of small satellites, improved sensor designs,

hyperspectral imaging, and enhanced radiometric accuracy are further

accelerating adoption. The emergence of low-cost commercial satellite

constellations and drone-based platforms has democratized access to

high-quality remote sensing data, reducing dependency on expensive,

government-led space programs. Cloud-based processing, machine learning

algorithms, and data-as-a-service (DaaS) models are making remote sensing more

scalable and user-friendly for businesses. As the volume of geospatial data

continues to increase, the value of high-resolution intelligence will keep

rising, solidifying this trend as a major driver of global market expansion.

Growing Adoption of

UAV-Based Remote Sensing Is Accelerating Market Expansion

The expanding use of unmanned

aerial vehicles (UAVs) for remote sensing applications is another significant

driver shaping the market’s growth trajectory. UAVs, or drones, have

transformed remote sensing by offering flexible, cost-effective, high-frequency

data collection capabilities. Unlike satellites, which have fixed orbital

schedules and limited revisit rates, UAVs can be deployed on demand and

tailored to specific mission requirements. This makes them particularly

valuable for sectors requiring frequent monitoring or localized imaging, such

as construction, energy, utilities, agriculture, and environmental

conservation.

UAV-based remote sensing provides

exceptional spatial resolution, often surpassing that of commercial satellites.

Equipped with multispectral, hyperspectral, LiDAR, and thermal sensors, drones

can generate detailed terrain models, vegetation indices, and structural

assessments with unmatched accuracy. Industries use UAV data for site surveys,

pipeline inspections, asset mapping, power line monitoring, and land

development planning. The rise of smart agriculture has significantly boosted

drone adoption, enabling farmers to detect nutrient deficiencies, irrigation

issues, and disease outbreaks early, thereby improving productivity and

profitability.

Technological advancements in UAV

endurance, sensor miniaturization, autonomous navigation, and data processing

capabilities have expanded their commercial viability. Regulatory frameworks in

major regions such as the U.S., Europe, and the Asia Pacific are evolving to

support wider drone deployment, including beyond visual line of sight (BVLOS)

operations. This regulatory progress is creating new opportunities for

drone-based service providers. The integration of AI and machine learning

further enhances UAV capabilities, allowing automated image classification,

anomaly detection, and predictive insights. As businesses seek more flexible

and cost-efficient alternatives to traditional satellite imaging, UAV-based

remote sensing will continue to play a critical role in driving market growth.

Rising Investments in

Space-Based Imaging and Constellation Expansion Create Significant Market

Opportunities Worldwide

The emergence of low-cost

satellite constellations and increased private-sector investment in space-based

imaging present major growth opportunities for the Remote Sensing Services

Market. Over the past decade, declining launch costs, advancements in small

satellite technology, and rising commercial interest in space exploration have

significantly expanded global satellite deployment. Companies such as Planet

Labs, Maxar Technologies, and BlackSky are launching high-frequency imaging

constellations capable of capturing near-real-time global coverage. These

capabilities support a wide range of applications, including defense

surveillance, economic activity tracking, environmental monitoring, and supply

chain intelligence.

Government agencies across the

U.S., Europe, India, China, and Japan are increasing investments in earth

observation programs and collaborating with private space companies to enhance

regional monitoring capabilities. The development of hyperspectral and SAR

(Synthetic Aperture Radar) satellites expands data diversity, allowing remote

sensing services to penetrate new markets such as disaster response, maritime

surveillance, soil analysis, and climate research. SAR satellites, for example,

can capture imagery through clouds and in darkness, making them indispensable

for all-weather monitoring.

As satellite constellations grow,

so does the demand for advanced data analytics, enabling remote sensing service

providers to offer value-added solutions such as change detection, predictive

modeling, and geospatial AI analysis. The emergence of space-based IoT and

real-time imagery streaming further expands the addressable market. With

increasing emphasis on global environmental transparency, carbon monitoring,

and climate risk assessment, space-based remote sensing will play an essential

role in enabling international sustainability initiatives. These trends

position constellation expansion and space-based imaging investments as one of

the most promising global opportunities for remote sensing service providers.

Remote Sensing Services

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 12.3 Billion |

|

Market Forecast in 2033 |

USD 30.7 Billion |

|

CAGR % 2025-2033 |

11.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Platform, By

Resolution, By End-use |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Remote Sensing Services

Market Report Segmentation Analysis

The global Remote Sensing

Services Market industry analysis is segmented by Platform, by Resolution, by

End-use, and by Region.

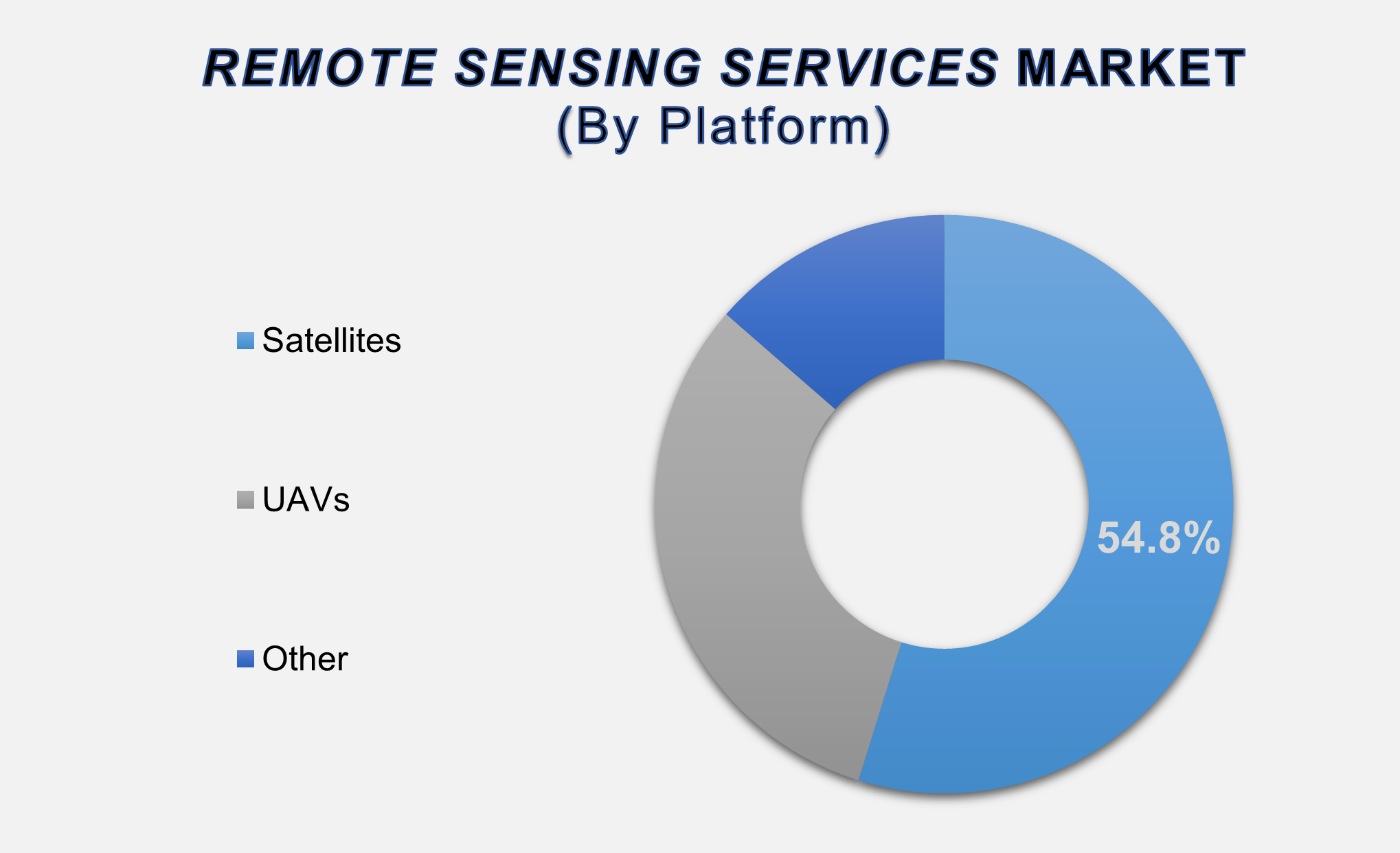

The Satellite Segment

Accounted for the Largest Market Share in the Global Remote Sensing Services

Market

The Satellites segment accounted

for the largest share of the remote sensing services market in 2025,

contributing 54.8% of global revenues. Satellites remain the backbone of the

remote sensing ecosystem by providing consistent, wide-area, and high-frequency

imagery required for strategic surveillance, environmental monitoring, resource

management, and climate analysis. Their ability to capture vast geographical

areas in a single pass makes them indispensable for national agencies, global

corporations, and research organizations. With the rapid expansion of small

satellite constellations and lower launch costs, satellite-based remote sensing

has become more affordable and powerful. The rise of commercial satellite

operators offering near-real-time imaging, high-resolution optical data, and

SAR imagery has transformed the accessibility of geospatial intelligence.

Industries such as agriculture,

infrastructure, and mining utilize satellite imagery for land analysis, crop

monitoring, mineral exploration, and disaster assessment. Defense agencies

depend heavily on satellite surveillance for intelligence gathering, border

monitoring, maritime domain awareness, and tracking geopolitical developments.

Satellite imaging is further strengthened by AI-powered analytics, which allow

automatic detection of changes, movement, or anomalies across large areas. As

demand grows for continuous environmental and security monitoring, and as

global satellite networks continue expanding, this segment will maintain its

dominant market position over the forecast period.

Spatial Resolution

Segment Leads the Global Market Due to High Demand for High-Precision Mapping

and Monitoring

The Spatial resolution segment

leads the resolution-based market, supported by strong demand for

high-precision mapping and surface detail analysis across commercial and

governmental sectors. Spatial resolution focuses on the ability to distinguish

small details on the Earth’s surface, making it the most widely used category

for applications such as urban planning, military surveillance, infrastructure

monitoring, forestry management, and environmental research. As industries seek

more accurate geospatial insights, high-resolution imagery ranging from

sub-meter to multi-meter has become essential for evaluating land use patterns,

detecting structural changes, and assessing ecological conditions.

Advancements in optical sensors,

satellite payload design, and AI-based image enhancement are enabling remote

sensing providers to deliver increasingly detailed spatial data. Additionally,

the integration of spatial data with GIS platforms facilitates advanced

modeling, predictive analysis, and decision support across industries. The

segment also benefits from growing use cases in insurance, real estate

assessment, and supply chain intelligence, where accurate spatial mapping is

critical. As more countries invest in high-resolution earth observation

programs and as commercial satellites continue to achieve improved spatial

capabilities, this segment will remain central to the global remote sensing

services market.

Commercial End-use

Segment Accounted for the Largest Share Due to Expanding Industrial and

Environmental Applications

The Commercial segment accounted

for the largest market share in the Remote Sensing Services Market and is

expected to maintain its leadership position throughout the forecast period.

Growing adoption of geospatial data across commercial industries, including

agriculture, utilities, real estate, construction, mining, transportation, and

environmental services, is driving rapid expansion. Companies increasingly rely

on remote sensing to optimize operations, reduce risk, comply with

environmental regulations, and improve asset management. For instance, mining

operators use remote sensing to track land deformation, assess mineral

potential, and ensure regulatory compliance, while utility providers leverage

imagery for powerline monitoring, vegetation encroachment analysis, and

infrastructure risk assessments.

The segment is further driven by

smart city development, which relies heavily on geospatial intelligence for

urban planning, traffic modeling, and infrastructure development. Remote

sensing also plays a crucial role in environmental impact assessments, carbon

tracking, water resource management, and disaster risk mitigation areas that

are rapidly expanding due to growing climate concerns. The increasing

availability of low-cost satellite imagery, UAV-based surveys, and cloud-based

analytics platforms is making remote sensing accessible to a broader range of

commercial enterprises. As data-driven decision-making becomes integral to

business strategy, the commercial end-use segment will continue dominating

global market revenues.

The following segments are

part of an in-depth analysis of the global Remote Sensing Services Market:

|

Market

Segments |

|

|

By Platform |

●

Satellites ●

UAVs ●

Other |

|

By

Resolution |

●

Spatial ●

Spectral ●

Radiometric ●

Temporal |

|

By End-user |

●

Commercial ●

Defense |

Remote Sensing Services Market Share Analysis by

Region

The North America region

is projected to hold the largest share of the global Remote Sensing Services

Market over the forecast period.

North America dominated the

Remote Sensing Services Market in 2025 with a 45.7% share, driven by

advanced aerospace infrastructure, strong government investment in satellite

programs, and high adoption of geospatial technologies across industries. The

U.S. leads global remote sensing innovation through NASA, NOAA, the Department

of Defense, and a thriving private ecosystem that includes players such as

Maxar Technologies, Planet Labs, and BlackSky. The region's defense sector

represents one of the largest consumers of remote sensing data, using it for

surveillance, reconnaissance, and strategic intelligence. Furthermore, North

America's commercial industries, including agriculture, forestry, utilities,

insurance, and logistics, widely employ satellite and UAV-based sensing to

improve data-driven operational efficiency.

Asia Pacific is expected to grow

at the fastest CAGR during 2025–2033, powered by increasing regional space

activities, expanding satellite programs in India, China, and Japan, and rapid

adoption of remote sensing for smart city development, agriculture optimization,

and resource management. The region’s growing industrialization and investment

in digital infrastructure will further propel remote sensing adoption. Emerging

economies in Southeast Asia, particularly Indonesia, Vietnam, and Malaysia, are

increasing their reliance on geospatial services for land management and

disaster monitoring.

Remote Sensing Services Market Competition

Landscape Analysis

The Remote

Sensing Services Market is moderately consolidated, with global players holding

significant market share and emerging companies innovating in AI-driven

analytics, hyperspectral sensing, and micro-satellite deployment. Leading

companies include Maxar Technologies, Planet Labs, Airbus, L3Harris

Technologies, and MDA, each offering extensive satellite imaging capabilities

and advanced data processing platforms. Newer players such as BlackSky,

Earth-i, and Satellogic are reshaping the competitive landscape with

high-frequency satellite constellations and cost-efficient imaging models.

Global Remote Sensing Services Market Recent

Developments News:

- In June 2022, Planet Labs, Inc., and Bayer AG entered into a contract

for Planet to provide SkySat satellite data and professional services. The

collaboration aims to develop solutions that optimize seed production,

enhance supply chain efficiency, and advance sustainable agricultural practices.

- In April 2022, Maxar

Technologies made a strategic investment in Blackshark.ai, a leading

provider of AI-powered geospatial analytics. This partnership reinforces

Maxar's commitment to advancing its 3D Earth Intelligence portfolio

through innovative, AI-driven data solutions.

The Global Remote Sensing Services Market is

dominated by a few large companies, such as

●

Maxar Technologies

●

Planet Labs

●

Airbus

●

L3Harris Technologies

●

MDA

●

Satellogic

●

URS Corporation

●

Antrix Corporation

●

Mitsubishi Electric

●

Geospatial Corporation

●

Terra Remote Sensing

●

AAM Group

●

Moscow Aerial

Photography

●

Geoserve

●

EagleView

●

Ecopia AI

●

Harris Geospatial

Solutions

●

BlackSky

●

Earth-i

●

ImageSat International

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Remote Sensing

Services Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Remote Sensing Services Market Scope and Market Estimation

1.2.1.Global Remote Sensing

Services Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast

(2025 - 2033)

1.2.2.Global Remote Sensing

Services Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Platform of Global Remote

Sensing Services Market

1.3.2.Resolution of Global Remote

Sensing Services Market

1.3.3.End-user of Global Remote

Sensing Services Market

1.3.4.Region of Global Remote

Sensing Services Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Remote Sensing Services Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Remote Sensing Services Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Remote Sensing

Services Market Estimates

& Forecast Trend Analysis, by Platform

4.1.

Global

Remote Sensing Services Market Revenue (US$ Bn) Estimates and Forecasts, by Platform,

2020 - 2033

4.1.1.Satellites

4.1.2.UAVs

4.1.3.Other

5.

Global Remote Sensing

Services Market Estimates

& Forecast Trend Analysis, by Resolution

5.1.

Global

Remote Sensing Services Market Revenue (US$ Bn) Estimates and Forecasts, by Resolution,

2020 - 2033

5.1.1.Spatial

5.1.2.Spectral

5.1.3.Radiometric

5.1.4.Temporal

6.

Global Remote Sensing

Services Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Remote Sensing Services Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

6.1.1.Commercial

6.1.2.Defense

7. Global

Remote Sensing Services Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Remote Sensing Services Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Remote

Sensing Services Market: Estimates

& Forecast Trend Analysis

8.1.

North

America Remote Sensing Services Market Assessments & Key Findings

8.1.1.North America Remote

Sensing Services Market Introduction

8.1.2.North America Remote

Sensing Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Platform

8.1.2.2. By Resolution

8.1.2.3. By End-user

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Remote

Sensing Services Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Remote Sensing Services Market Assessments & Key Findings

9.1.1.Europe Remote Sensing

Services Market Introduction

9.1.2.Europe Remote Sensing

Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Platform

9.1.2.2. By Resolution

9.1.2.3. By End-user

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Remote

Sensing Services Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Remote Sensing Services Market Introduction

10.1.2.

Asia

Pacific Remote Sensing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Platform

10.1.2.2. By Resolution

10.1.2.3. By End-user

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Remote

Sensing Services Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Remote Sensing Services Market

Introduction

11.1.2.

Middle East & Africa Remote Sensing Services Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Platform

11.1.2.2. By Resolution

11.1.2.3. By End-user

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Remote Sensing Services Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Remote Sensing Services Market Introduction

12.1.2.

Latin

America Remote Sensing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Platform

12.1.2.2. By Resolution

12.1.2.3. By End-user

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Remote Sensing Services Market Product Mapping

14.2.

Global

Remote Sensing Services Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Remote Sensing Services Market Tier Structure Analysis

14.4.

Global

Remote Sensing Services Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1. Maxar

Technologies

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Planet Labs

15.3. Airbus

15.4. L3Harris

Technologies

15.5. MDA

15.6. Satellogic

15.7. URS

Corporation

15.8. Antrix

Corporation

15.9. Mitsubishi

Electric

15.10. Geospatial

Corporation

15.11. Terra Remote

Sensing

15.12. AAM Group

15.13. Moscow Aerial

Photography

15.14. Geoserve

15.15. EagleView

15.16. Ecopia AI

15.17. Harris

Geospatial Solutions

15.18. BlackSky

15.19. Earth-i

15.20. ImageSat

International

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables