Reverse Logistics Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Return Type (Repairs & Returns, Commercial Returns, End-of-Life Returns and Recalls), By Service (Returns Management, Refurbishment, Remanufacturing, Packaging and Others), By End-User (E-commerce, Automotive, Pharmaceutical, Consumer Electronics, Retail and Others), and Geography

2025-12-02

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Reverse Logistics Market Overview

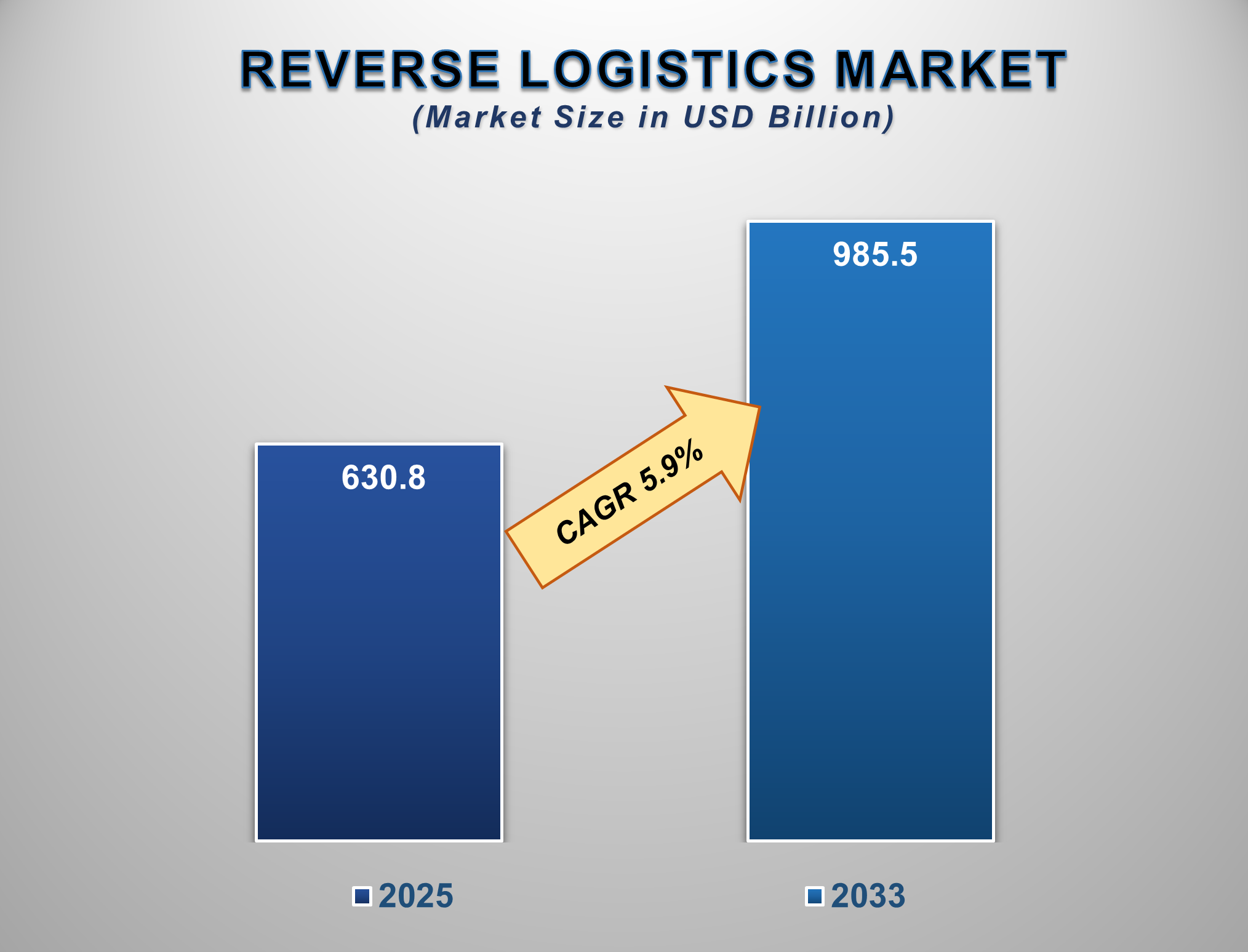

The Reverse Logistics Market is poised for a period of robust and strategic growth from 2025 to 2033, fueled by the explosive expansion of e-commerce, rising consumer expectations for returns, stringent environmental regulations, and the growing economic imperative of value recovery from returned goods. The market is projected to be valued at approximately USD 630.8 billion in 2025 and is forecasted to reach nearly USD 985.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 5.9% during this period.

Reverse logistics encompasses all operations

related to the reverse flow of products from their final destination for the

purpose of capturing value, returns management, or proper disposal. This

includes processes for returns management, remanufacturing, refurbishment,

recycling, and resale. The market's significant expansion is primarily driven

by the global e-commerce boom, which has fundamentally increased the volume of

product returns, making efficient reverse logistics a critical competitive

differentiator.

Furthermore, increasing consumer awareness of

sustainability and circular economy principles is pushing companies to adopt

responsible end-of-life product management practices. Supportive government

regulations regarding e-waste and product disposal, coupled with the

significant cost savings and revenue generation opportunities from recovered

assets, are significantly contributing to market growth. North America

currently holds a significant market share due to its mature e-commerce sector

and high consumption rates, while the Asia-Pacific region is expected to

witness the fastest growth, driven by its rapidly expanding online retail

markets and increasing manufacturing activities.

Reverse

Logistics Market Drivers and Opportunities

The Exponential Growth of E-commerce and

Evolving Consumer Return Policies is the Primary Market Driver

The relentless growth of the global e-commerce

sector is the most powerful force propelling the reverse logistics market. The

convenience of online shopping inherently leads to a higher rate of product

returns compared to brick-and-mortar retail, driven by factors such as

"bracketing" (ordering multiple sizes), products not matching

descriptions, and simple buyer's remorse. In highly competitive markets,

retailers have adopted liberal and free return policies to attract and retain

customers, further increasing the volume of reverse flows. This has transformed

reverse logistics from a cost-centric, back-office function into a strategic

front-office priority. Efficient and hassle-free returns are now a key factor

in customer loyalty and repurchase decisions. The sheer scale of returned

goods, spanning from electronics and apparel to furniture, creates an immense

operational and financial burden, making the optimization of reverse logistics

processes essential for profitability and customer satisfaction.

The global e-commerce market continues its

meteoric rise, fundamentally reshaping retail and consumer behavior. In 2024, worldwide e-commerce sales are estimated to exceed

$6.3 trillion, accounting for over 21% of total retail sales. This figure is

projected to grow to over $8.1 trillion by 2027. This growth is underpinned by

increasing internet and smartphone penetration, secure digital payment systems,

and the post-pandemic normalization of online shopping. The Asia-Pacific region

leads in market share, driven by giants like China and India, but significant

growth is observed across North America and Europe. This data underscores the

immense scale of the digital marketplace and highlights the corresponding

logistical challenge and opportunity presented

by the parallel surge in product returns, which can range from 20% to over 30%

of all e-commerce sales, depending on the

product category.

The Imperative of Sustainability and the

Circular Economy is Driving Strategic Adoption

The global push towards sustainability and the

formalization of circular economy models is a powerful catalyst for the reverse

logistics market. Businesses are facing increasing pressure from consumers,

investors, and regulators to minimize their environmental footprint and

demonstrate corporate social responsibility. Effective reverse logistics is the

operational backbone of the circular economy, enabling the recovery,

refurbishment, and reintegration of products and materials back into the supply

chain. This process reduces waste sent to landfills, conserves raw materials,

and lowers the carbon emissions associated with manufacturing new products.

Legislation, such as Extended Producer Responsibility (EPR) laws, which hold

manufacturers accountable for the entire lifecycle of their products, including

end-of-life disposal, is compelling industries to invest in sophisticated

reverse logistics networks. This shift transforms returned or end-of-life

products from liabilities into valuable assets for material recovery and

sustainable practice.

The Emergence of Advanced Technologies and

the Value of Secondary Markets Present Significant Opportunities

The strategic integration of technology and the

development of robust resale channels are creating significant growth frontiers

for the reverse logistics market. Key opportunities lie in the application of

advanced technologies like Artificial Intelligence (AI) and the Internet of

Things (IoT) to optimize reverse supply chains. AI-powered systems can automate

returns authorization, determine the optimal disposition (e.g., restock,

refurbish, recycle), and dynamically route products, thereby reducing processing

costs and time. IoT sensors can track returned assets and monitor their

condition in transit. Furthermore, the burgeoning secondary market for

refurbished and open-box goods, particularly in high-value categories like

consumer electronics, represents a massive revenue-generating opportunity. For

logistics providers and retailers, investing in automation for warehouse

sorting, developing AI-driven analytics platforms for returns management, and

building dedicated sales channels for refurbished products are key strategies

to capture untapped market potential and turn reverse logistics into a profit

center.

Reverse Logistics Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 630.8 Billion |

|

Market Forecast in 2033 |

USD 985.5 Billion |

|

CAGR % 2025-2033 |

5.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Return Type ●

By Service ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Reverse Logistics Market

Report Segmentation Analysis

The global Reverse Logistics

Market industry analysis is segmented by Return Type, by Service, by End-User,

and by Region.

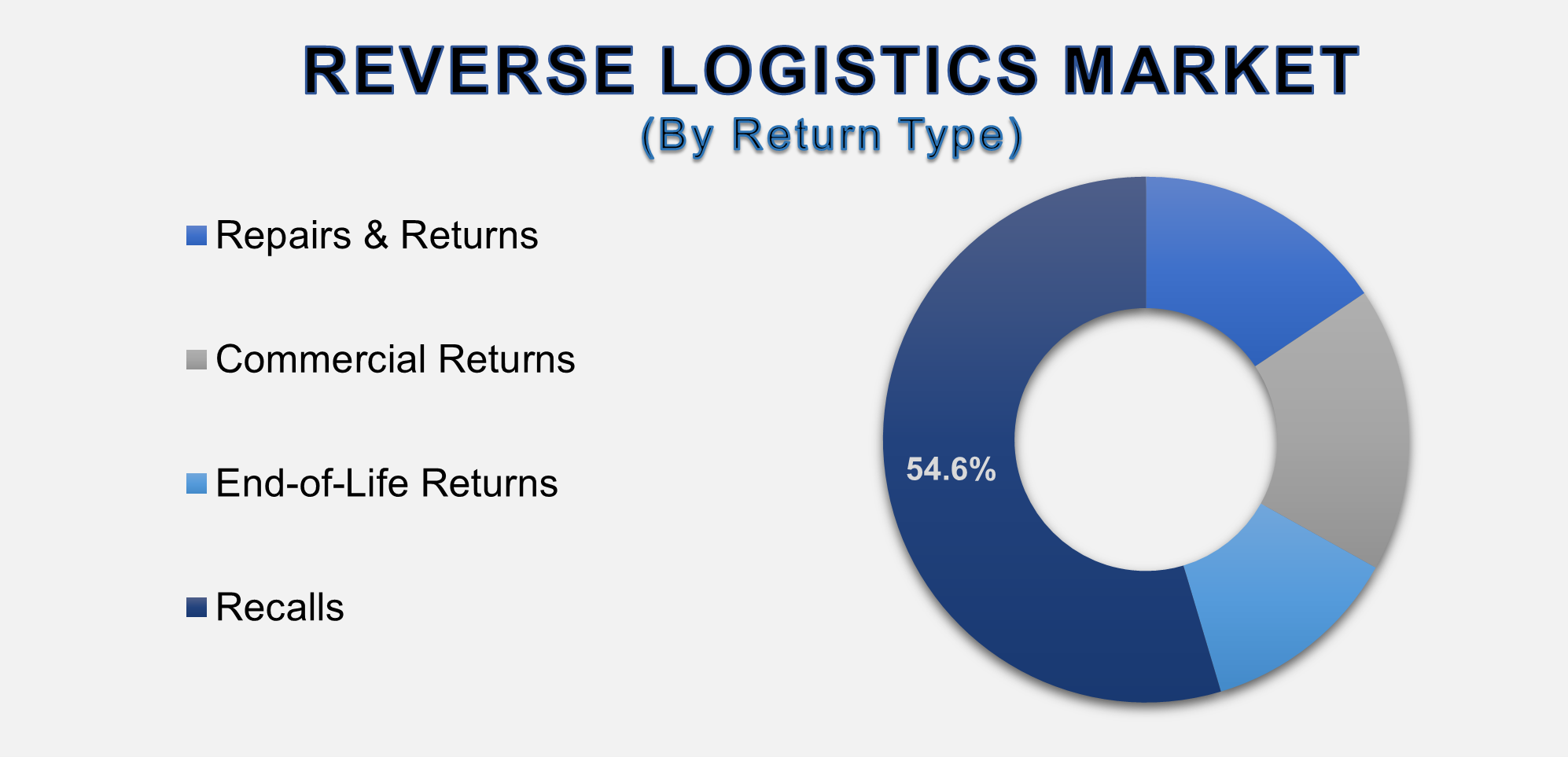

The Recalls Return Type segment is anticipated to

command a significant market share in 2025

The Return Type segment is categorized

into Repairs & Returns, Commercial Returns, End-of-Life Returns, and

Recalls. The recalls segment holds a substantial and critical share of the

market due to the high-stakes and complex nature of the process. Product

recalls, whether mandated by regulatory bodies or initiated voluntarily by

manufacturers, involve the coordinated reverse flow of potentially millions of

units from distributors, retailers, and consumers. This process is logistically

intensive, requiring meticulous tracking, specialized handling (especially for

hazardous or defective goods), and often, destruction or complex remediation.

The high costs associated with managing a recall, coupled with the severe

reputational and legal risks of mishandling, compel companies to rely on expert

reverse logistics providers. The critical importance of efficiency, compliance,

and transparency in recall management ensures this segment remains a major and

high-value component of the reverse logistics market.

The Refurbishment Service segment is projected to

grow at a significant CAGR.

The Service segment includes Returns Management,

Refurbishment, Remanufacturing, Packaging, and Others. The refurbishment

service segment's projected significant growth is directly linked to the

powerful economic and environmental logic of the circular economy.

Refurbishment involves restoring a returned product to a like-new condition,

often with updated software or replaced components, so it can be resold in

secondary markets. This process captures significant value from products that

would otherwise be sold at a deep discount or written off as a loss. The

growing consumer acceptance of certified refurbished goods, particularly in the

electronics sector (smartphones, laptops, tablets), is creating a massive and

profitable market. For companies, investing in refurbishment capabilities not

only generates new revenue streams but also enhances brand sustainability

credentials and reduces environmental waste, making it one of the most dynamic

and fast-growing service areas.

The E-commerce end-user

segment is projected to witness the highest growth rate.

The End-User segment is divided into E-commerce,

Automotive, Pharmaceutical, Consumer Electronics, and Retail. The E-commerce

segment's position as the fastest-growing channel is a direct consequence of

the sector's overall expansion and its inherent high-return nature. As

detailed in the market drivers, the volume of returns in e-commerce is immense

and continues to grow in lockstep with online sales. E-commerce companies and

the brands that sell through them are under immense pressure to manage returns

efficiently to protect margins and customer loyalty. This has led to massive

investment in dedicated returns processing centers, sophisticated returns

management software, and partnerships with third-party logistics (3PL)

providers specializing in reverse logistics. The continuous innovation in

"return-to-shelf" speed and the development of seamless return

experiences are powerful forces propelling the explosive growth of reverse

logistics services within the e-commerce industry.

The following segments are part of an in-depth analysis of

the global Reverse Logistics Market:

|

Market

Segments |

|

|

By Return Type |

●

Repairs &

Returns ●

Commercial Returns ●

End-of-Life Returns ●

Recalls |

|

By Service |

●

Returns Management ●

Refurbishment ●

Remanufacturing ●

Packaging ●

Others |

|

By End-user |

●

E-commerce ●

Automotive ●

Pharmaceutical ●

Consumer Electronics ●

Retail ●

Others |

Reverse Logistics Market

Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Reverse Logistics Market

globally throughout the forecast period.

North America's dominance is attributed to its

massive and mature e-commerce landscape, high consumer purchasing power, and a

well-developed logistics infrastructure. The region has a strong culture of

liberal return policies, which drives a consistently high volume of reverse

flows. Furthermore, the presence of major global retailers and e-commerce

giants, coupled with a stringent regulatory environment for product safety and

recalls (e.g., by the Consumer Product Safety Commission), creates a sustained

demand for sophisticated reverse logistics services. The high level of

technological adoption among logistics providers in North America to manage

these complex processes efficiently solidifies its leading position.

The United States, in particular, is the world's

largest single market for reverse logistics. The country's vast geography,

concentrated consumer base, and highly competitive retail environment make

returns management a critical business function. Major investments in

automation and AI for returns processing are often pioneered in the U.S.

market. The well-established secondary market for refurbished electronics and

other goods also provides a strong economic incentive for efficient value

recovery processes, ensuring a continuous demand for advanced reverse logistics

solutions.

Reverse Logistics Market

Competition Landscape Analysis

The global reverse logistics

market is fragmented and competitive, featuring a mix of global logistics

giants, specialized third-party logistics (3PL) providers, and in-house

operations of large retailers. Competition is intensifying and centers on service

reliability, technological capability, geographic reach, and industry-specific

expertise. Key strategies include significant investment in technology

platforms for returns visibility and management, strategic acquisitions to gain

new capabilities or geographic footholds, and the development of value-added

services like refurbishment and recommerce. The market also sees increasing

competition from tech startups offering AI-driven returns optimization software

and platform-based solutions that connect retailers with logistics networks.

Global Reverse Logistics

Market Recent Developments News:

- In January 2025, UPS announced the expansion of its

dedicated returns facilities across Europe, integrating AI-based sorting

to accelerate processing times for e-commerce returns.

- In November 2024, Optoro, a leading returns

technology platform, partnered with a major European fashion retailer to

implement a data-driven returns solution that increased the resale value of returned goods by 20%.

- In July 2024, Apple Inc. reported a record quarter

for its refurbished products division, highlighting the growing

profitability and consumer demand for certified pre-owned devices,

underpinned by its efficient reverse logistics operations.

- In September 2024, FedEx Corp. launched a new suite of circular

logistics services, focusing on the consolidation and sustainable

processing of end-of-life electronics for corporate clients.

The Global Reverse Logistics Market Is Dominated by a Few

Large Companies, such as

●

United Parcel Service,

Inc. (UPS)

●

FedEx Corporation

●

Deutsche Post DHL

Group

●

XPO Logistics, Inc.

●

GXO Logistics, Inc.

●

Kintetsu World

Express, Inc.

●

Optoro, Inc.

●

Reverse Logistics

Group

●

Liquidity Services,

Inc.

●

Arrow Electronics,

Inc.

●

Hub Group

●

C.H. Robinson

●

Ryder System, Inc.

●

Pitney Bowes Inc.

● Flexport Inc.

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Reverse Logistics

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Reverse Logistics Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Reverse Logistics

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Return Type of Global Reverse

Logistics Market

1.3.2.Service of Global Reverse

Logistics Market

1.3.3.End-user of Global Reverse

Logistics Market

1.3.4.Region of Global Reverse

Logistics Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

Reverse Logistics Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Reverse Logistics Market Estimates

& Forecast Trend Analysis, by Return Type

4.1.

Global

Reverse Logistics Market Revenue (US$ Bn) Estimates and Forecasts, by Return

Type, 2020 - 2033

4.1.1.Repairs & Returns

4.1.2.Commercial Returns

4.1.3.End-of-Life Returns

4.1.4.Recalls

5. Global

Reverse Logistics Market Estimates

& Forecast Trend Analysis, by Service

5.1.

Global

Reverse Logistics Market Revenue (US$ Bn) Estimates and Forecasts, by Service, 2020

- 2033

5.1.1.Returns Management

5.1.2.Refurbishment

5.1.3.Remanufacturing

5.1.4.Packaging

5.1.5.Others

6. Global

Reverse Logistics Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Reverse Logistics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

2020 - 2033

6.1.1.E-commerce

6.1.2.Automotive

6.1.3.Pharmaceutical

6.1.4.Consumer Electronics

6.1.5.Retail

6.1.6.Others

7. Global

Reverse Logistics Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Reverse Logistics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Reverse

Logistics Market: Estimates &

Forecast Trend Analysis

8.1. North America Reverse

Logistics Market Assessments & Key Findings

8.1.1.North America Reverse

Logistics Market Introduction

8.1.2.North America Reverse

Logistics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Return Type

8.1.2.2.

By Service

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Reverse

Logistics Market: Estimates &

Forecast Trend Analysis

9.1. Europe Reverse Logistics

Market Assessments & Key Findings

9.1.1.Europe Reverse Logistics

Market Introduction

9.1.2.Europe Reverse Logistics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Return Type

9.1.2.2.

By Service

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Reverse

Logistics Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Reverse Logistics Market Introduction

10.1.2.

Asia

Pacific Reverse Logistics Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Return Type

10.1.2.2.

By Service

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Reverse

Logistics Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Reverse Logistics Market Introduction

11.1.2. Middle

East & Africa

Reverse Logistics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Return Type

11.1.2.2.

By Service

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Reverse Logistics Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Reverse

Logistics Market Introduction

12.1.2. Latin America Reverse

Logistics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Return Type

12.1.2.2.

By Service

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Reverse Logistics

Market Product Mapping

14.2. Global Reverse Logistics

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Reverse Logistics

Market Tier Structure Analysis

14.4. Global Reverse Logistics

Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

United Parcel Service, Inc. (UPS)

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

FedEx Corporation

15.3.

Deutsche Post DHL Group

15.4.

XPO Logistics, Inc.

15.5.

GXO Logistics, Inc.

15.6.

Kintetsu World Express, Inc.

15.7.

Optoro, Inc.

15.8.

Reverse Logistics Group

15.9.

Liquidity Services, Inc.

15.10.

Arrow Electronics, Inc.

15.11.

Hub Group

15.12.

C.H. Robinson

15.13.

Ryder System, Inc.

15.14.

Pitney Bowes Inc.

15.15.

Flexport Inc.

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables