Rigid Packaging Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Material (Plastic, Metal, Glass, Paperboard, Others); By Product Type (Bottles & Jars, Trays, Containers, Cans, Boxes & Cartons, Drums & Intermediate Bulk Containers, Others); By End-use Industry (Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, Chemicals, Industrial Goods, Household Products, Others); By Distribution Channel (Retail Packaging, E-commerce Packaging, Industrial Packaging, Institutional Packaging), and Geography

2026-06-23

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Rigid Packaging Market Overview

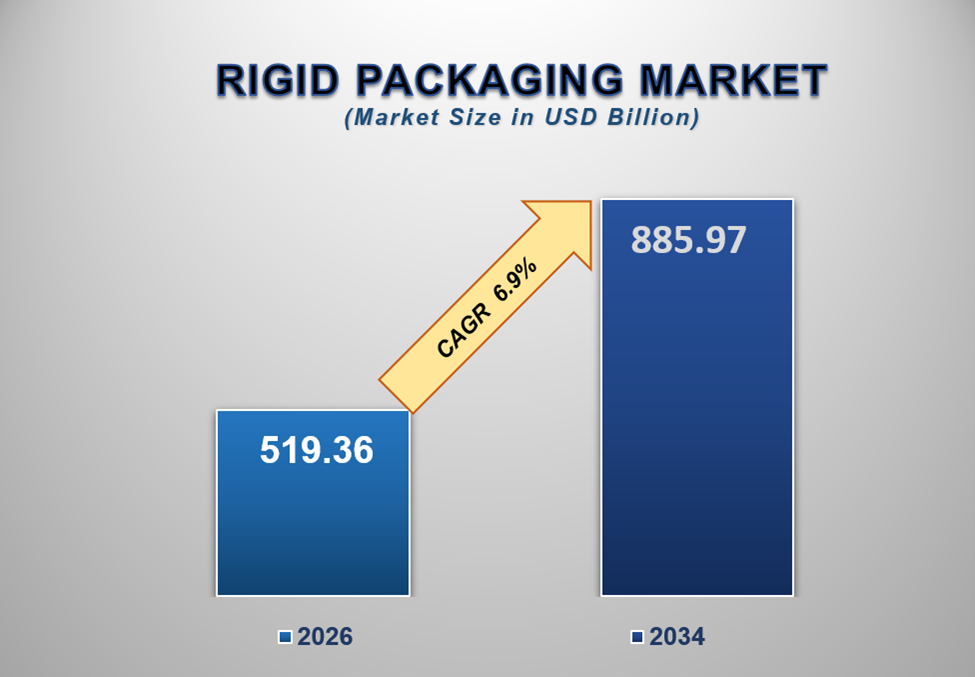

The global Rigid

Packaging Market was valued at USD 519.36 billion in 2026 and is

projected to reach USD 885.97 billion by 2034, expanding at a CAGR of 6.9%

during the forecast period. The market is experiencing consistent growth

due to increasing demand from food and beverage manufacturers, rapid expansion

of e-commerce activities, growing pharmaceutical production, rising consumer

preference for safe and durable packaging solutions, and continuous innovations

in sustainable packaging materials and manufacturing technologies.

Rigid packaging

represents one of the most widely used packaging formats globally. It

encompasses a broad range of products, including bottles, jars, cans, trays,

containers, cartons, drums, and bulk packaging solutions. Unlike flexible

packaging, rigid packaging maintains its shape regardless of the product it

contains, offering superior structural integrity, product protection,

durability, and shelf presentation.

The market plays

a crucial role in global supply chains by ensuring safe storage,

transportation, distribution, and display of products across numerous

industries. Food manufacturers, pharmaceutical companies, personal care brands,

chemical producers, and industrial manufacturers rely extensively on rigid

packaging solutions to preserve product quality, prevent contamination, enhance

shelf life, and comply with regulatory requirements.

One of the

primary factors driving market expansion is the sustained growth of the global

food and beverage industry. Increasing urbanization, changing lifestyles,

rising consumption of packaged foods, and growing demand for convenience

products are significantly increasing the need for high-performance packaging

solutions. Rigid containers provide excellent barrier protection, durability,

and handling characteristics, making them particularly suitable for food and

beverage applications.

The

pharmaceutical sector is emerging as another major contributor to growth.

Increasing healthcare expenditures, expanding pharmaceutical manufacturing,

growing demand for over-the-counter medications, and stricter regulatory

requirements for product safety are driving substantial demand for rigid

packaging formats such as bottles, vials, containers, and specialty packaging

systems.

Additionally,

the rapid expansion of e-commerce is creating new opportunities for rigid

packaging manufacturers. Online retail channels require packaging solutions

capable of protecting products during transportation while maintaining product

integrity throughout complex logistics networks. As e-commerce penetration

continues to increase globally, demand for robust packaging solutions is

expected to grow significantly.

Sustainability

is becoming a defining factor influencing market development. Consumers,

governments, and corporations are increasingly prioritizing recyclable,

reusable, and environmentally responsible packaging materials. As a result,

packaging manufacturers are investing heavily in circular economy initiatives,

lightweight packaging designs, the integration of recycled content, and

innovative material technologies.

Technological

advancements in manufacturing automation, digital printing, smart packaging,

barrier coatings, and material engineering are further transforming the market

landscape. These innovations enable manufacturers to improve production

efficiency, enhance packaging functionality, and meet evolving customer

requirements.

As consumer goods production expands, global trade increases, and sustainability initiatives gain momentum, the rigid packaging market is expected to maintain strong growth throughout the forecast period.

Rigid Packaging Market Drivers and

Opportunities

Expanding

Food and Beverage Industry Is Driving Market Growth

The food and

beverage sector remains the largest consumer of rigid packaging products and

continues to serve as a major driver of market growth.

The global

demand for packaged food products is increasing steadily due to urbanization,

rising disposable incomes, busy lifestyles, and changing consumption habits.

Consumers increasingly prefer ready-to-eat meals, packaged beverages, dairy

products, frozen foods, snacks, and convenience foods, all of which require

reliable packaging solutions.

Rigid packaging

offers several advantages that make it highly suitable for food applications.

These include excellent product protection, superior moisture and oxygen

barrier properties, enhanced product visibility, tamper resistance, and

extended shelf life.

Bottles, jars,

trays, and containers are extensively used across food and beverage categories

because they help maintain freshness while ensuring compliance with food safety

regulations.

Furthermore,

premium food and beverage brands increasingly utilize rigid packaging to

enhance product presentation and strengthen brand identity. Attractive

packaging designs influence consumer purchasing decisions and contribute to

product differentiation in competitive retail environments.

As global food production and consumption continue expanding, demand for rigid packaging solutions is expected to grow substantially.

Growing

Pharmaceutical and Healthcare Packaging Demand Is Accelerating Market Expansion

The

pharmaceutical industry is becoming an increasingly important end-user segment

within the rigid packaging market.

The growing

prevalence of chronic diseases, aging populations, increasing healthcare

access, and rising pharmaceutical consumption are generating strong demand for

safe and compliant packaging systems.

Pharmaceutical

packaging must meet stringent regulatory requirements related to product

stability, contamination prevention, tamper evidence, child resistance, and

traceability. Rigid packaging formats provide the structural integrity and

protection necessary to meet these requirements.

Glass bottles,

plastic containers, pharmaceutical jars, vials, and specialty rigid packaging

products play a critical role in safeguarding medicines throughout their

lifecycle.

The rapid growth

of biologics, specialty pharmaceuticals, vaccines, and personalized medicine is

further increasing demand for advanced packaging solutions.

In addition,

healthcare institutions, diagnostic laboratories, and medical device

manufacturers are utilizing rigid packaging systems for a wide range of

healthcare products and equipment.

As global healthcare spending continues to rise, pharmaceutical packaging demand is expected to contribute significantly to market growth.

Sustainability

and Circular Economy Initiatives Present Significant Opportunities

Sustainability

is creating transformative opportunities across the rigid packaging industry.

Governments

worldwide are implementing regulations aimed at reducing packaging waste,

increasing recycling rates, and promoting sustainable material usage.

Simultaneously, consumers are increasingly favoring brands that demonstrate

environmental responsibility.

In response,

packaging manufacturers are investing in recyclable plastics, lightweight

packaging technologies, bio-based materials, recycled content integration, and

reusable packaging systems.

The development

of closed-loop recycling systems is enabling greater material recovery and

reducing reliance on virgin raw materials. Advanced manufacturing technologies

are helping producers improve sustainability without compromising packaging

performance.

Furthermore,

major consumer goods companies have established ambitious sustainability

targets related to packaging recyclability, waste reduction, and carbon

footprint reduction.

Smart packaging

technologies that improve supply chain visibility and reduce product waste also

present promising opportunities for future market expansion.

Companies capable of delivering sustainable, cost-effective, and high-performance packaging solutions are expected to gain significant competitive advantages over the coming years.

Rigid Packaging Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 519.36 Billion |

|

Market Forecast in 2034 |

USD 885.97 Billion |

|

CAGR % 2026-2034 |

6.9% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production, Service Type, Growth

Factors and more |

|

Segments Covered |

∙ By Material |

|

Regional Scope |

● North America |

|

Country Scope |

U.S. |

Rigid

Packaging Market Report Segmentation Analysis

The global rigid packaging market industry analysis is segmented by material, by product type, by end-use industry, by distribution channel, and by region.

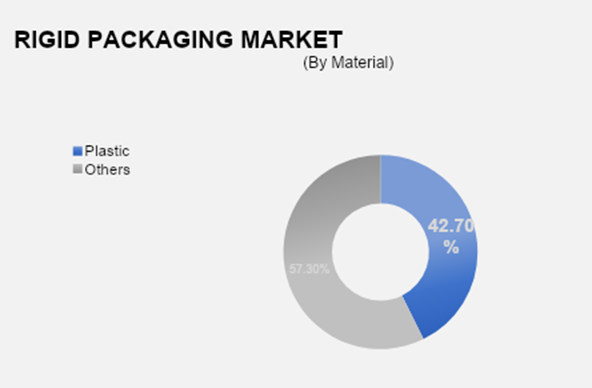

Plastic

Segment Is Expected to Dominate the Market During the Forecast Period

The plastic segment accounted for approximately 42.7% of the global market, making it the largest material category.

Plastic

continues to dominate the rigid packaging market due to its exceptional

versatility, lightweight nature, durability, cost-effectiveness, and design

flexibility. Manufacturers across multiple industries prefer plastic packaging

because it can be produced in a wide variety of shapes, sizes, and performance

specifications while maintaining relatively low production costs.

Plastic

packaging materials such as PET, HDPE, PP, and PVC offer excellent barrier

properties, impact resistance, and chemical compatibility, making them suitable

for food products, beverages, pharmaceuticals, household products, and

industrial applications.

The food and

beverage industry remains the largest consumer of rigid plastic packaging due

to its ability to preserve freshness, improve transportation efficiency, and

enhance shelf appeal. Beverage bottles, dairy containers, food jars, and

ready-meal packaging are among the most widely used applications.

In addition,

pharmaceutical manufacturers increasingly utilize rigid plastic containers

because of their lightweight characteristics, durability, and compatibility

with automated filling and packaging systems.

The segment is

also evolving rapidly toward sustainability. Manufacturers are integrating

recycled plastics, developing mono-material packaging structures, and improving

recyclability to address environmental concerns and regulatory requirements.

Despite increasing focus on sustainability, plastic is expected to maintain its leadership position due to its performance advantages, affordability, and widespread applicability across end-use sectors.

Bottles &

Jars Segment Is Expected to Lead the Market by Product Type

Bottles and jars

represent the largest product type segment within the rigid packaging market.

These packaging

formats are extensively utilized across the food and beverage, pharmaceutical,

personal care, household products, and chemical industries. Their popularity

stems from their convenience, durability, resealability, and ability to provide

superior product protection.

The beverage

industry remains a major contributor to segment growth, utilizing billions of

bottles annually for water, carbonated drinks, juices, dairy products, and

alcoholic beverages. Similarly, food manufacturers rely heavily on jars for

sauces, condiments, spreads, baby foods, and preserved products.

The

pharmaceutical industry also utilizes bottles and jars for tablets, capsules,

liquid medications, nutraceuticals, and healthcare products.

Advancements in

lightweight bottle manufacturing, sustainable resin technologies, and smart

packaging solutions are further strengthening segment growth.

Given their broad application range and essential role across numerous industries, bottles and jars are expected to remain the dominant product category throughout the forecast period.

The Food

& Beverage Segment Is Expected to Dominate the Market by End-Use Industry

The food and

beverage industry accounts for the largest share of the global rigid packaging

market.

The increasing

global population, rising packaged food consumption, urbanization, changing

dietary habits, and growth of modern retail channels are driving significant

demand for food packaging solutions.

Food

manufacturers require packaging systems that maintain product freshness,

prevent contamination, extend shelf life, and comply with food safety

regulations. Rigid packaging effectively addresses these requirements while

also providing branding and merchandising benefits.

Additionally,

the growing demand for convenience foods, ready-to-drink beverages, frozen

products, and premium food offerings is supporting increased adoption of rigid

containers.

Consumers

increasingly value packaging that offers portability, resealability,

transparency, and ease of use, all of which contribute to the continued

popularity of rigid packaging formats.

As food production and consumption continue increasing globally, the food and beverage segment is expected to maintain its dominant position.

Retail

Packaging Segment Is Expected to Lead the Market by Distribution Channel

Retail packaging

represents the largest distribution channel segment due to the extensive use of

rigid packaging across consumer-facing products.

Products sold

through supermarkets, hypermarkets, convenience stores, pharmacies, specialty

retailers, and online retail channels rely heavily on rigid packaging to ensure

product protection and visual appeal.

Brand owners

increasingly utilize innovative packaging designs to differentiate products and

attract consumer attention in competitive retail environments.

The expansion of

organized retail networks, premium product categories, and branded consumer

goods is contributing significantly to segment growth.

Additionally, increasing consumer preference for packaged and branded products continues to strengthen demand for retail packaging solutions worldwide.

The following

segments are part of an in-depth analysis of the global Rigid Packaging market:

|

Market

Segments |

|

|

By

Material |

∙

Plastic |

|

By Product Type |

∙

Bottles & Jars |

|

By Distribution Channel |

|

|

By

End Use Industry |

∙

Food & Beverage |

Rigid

Packaging Market Share Analysis By Region

Asia-Pacific is

projected to dominate the global rigid packaging market, accounting for

approximately 41.3% of total market revenue in 2026.

The region

benefits from large consumer populations, expanding manufacturing activities,

increasing urbanization, rapid industrialization, and strong growth in food

processing and consumer goods industries.

China remains

the largest market due to its extensive manufacturing base, massive consumer

market, and dominant role in global packaging production. India is emerging as

one of the fastest-growing markets, supported by rising disposable incomes,

growing retail penetration, expanding e-commerce activities, and increasing

demand for packaged products.

Japan and South

Korea continue contributing through advanced packaging technologies,

high-quality manufacturing standards, and innovation-driven packaging

solutions.

North America

represents another major market due to strong demand from food, beverage,

healthcare, and consumer goods industries. The region is also at the forefront

of sustainable packaging innovation and recycling initiatives.

Europe maintains

a significant market share due to stringent environmental regulations, advanced

packaging technologies, and strong consumer demand for sustainable products.

Meanwhile, Latin America and the Middle East & Africa are witnessing gradual growth supported by expanding consumer markets and increasing industrial development.

Rigid

Packaging Market Competition Landscape Analysis

The global rigid

packaging market is highly competitive and characterized by large multinational

packaging companies, regional manufacturers, material suppliers, and

specialized packaging solution providers.

Leading market

participants are investing heavily in sustainable packaging development,

recycled content integration, advanced manufacturing technologies, smart

packaging solutions, and capacity expansion projects.

Innovation

remains a key competitive factor as companies seek to balance performance, cost

efficiency, regulatory compliance, and environmental sustainability.

Strategic

mergers, acquisitions, joint ventures, and long-term supply agreements continue

shaping the competitive landscape. Companies are increasingly collaborating

with consumer goods manufacturers to develop customized packaging solutions

that meet evolving market requirements.

The growing focus on circular economy initiatives, lightweight packaging, digital printing technologies, and intelligent packaging systems is expected to further intensify competition during the forecast period.

Global Rigid

Packaging Market Recent Developments News:

∙ In April 2026,

major packaging manufacturers expanded investments in recycled plastic

packaging production facilities to support sustainability objectives.

∙ In February

2026, several consumer goods companies introduced packaging initiatives focused

on increasing recycled content and improving recyclability.

∙ In November

2025, packaging manufacturers accelerated development of lightweight rigid

packaging solutions aimed at reducing transportation costs and carbon

emissions.

∙ In August

2025, food and beverage companies increased adoption of sustainable rigid

packaging formats in response to changing consumer preferences.

∙ In June 2025, packaging technology providers introduced advanced smart packaging systems designed to improve supply chain visibility and product traceability.

The Global

Rigid Packaging Market is Dominated by a Few Large Companies, Such As

∙ Amcor plc

∙ Berry Global Group, Inc.

∙ Silgan Holdings Inc.

∙ Ball Corporation

∙ Crown Holdings, Inc.

∙ Sonoco Products Company

∙ DS Smith Plc

∙ Greif, Inc.

∙ Sealed Air Corporation

∙ ALPLA Group

∙ Mauser Packaging Solutions

∙ Plastipak Holdings, Inc.

∙ Ardagh Group S.A.

∙ Veritiv Corporation

∙ Reynolds Group Holdings Limited

∙ Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Rigid Packaging

Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Rigid Packaging Market Scope and Market Estimation

1.2.1.

Global Rigid Packaging Overall

Market Size (US$ Billion), Market CAGR (%), Market Forecast (2026 - 2034)

1.2.2.

Global Rigid Packaging Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1.

Material of Global Rigid

Packaging Market

1.3.2.

Product Type of Global Rigid

Packaging Market

1.3.3.

End-use Industry of Global

Rigid Packaging Market

1.3.4.

Distribution Channel of Global

Rigid Packaging Market

1.3.5.

Region of Global Rigid

Packaging Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Billion) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Packaging Regulations, Sustainability Standards and

Compliance Framework

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global Rigid Packaging

Market Estimates & Historical Trend Analysis (2021 - 2025)

4.

Global Rigid Packaging

Market Estimates & Forecast Trend Analysis, by Material

4.1. Global Rigid Packaging Market Revenue (US$ Billion) Estimates and

Forecasts, by Material, 2021 - 2034

4.1.1.

Plastic

4.1.2.

Metal

4.1.3.

Glass

4.1.4.

Paperboard

4.1.5.

Others

5.

Global Rigid Packaging

Market Estimates & Forecast Trend Analysis, by Product Type

5.1. Global Rigid Packaging Market Revenue (US$ Billion) Estimates and

Forecasts, by Product Type, 2021 - 2034

5.1.1.

Bottles & Jars

5.1.2.

Trays

5.1.3.

Containers

5.1.4.

Cans

5.1.5.

Boxes & Cartons

5.1.6.

Drums & Intermediate Bulk

Containers

5.1.7.

Others

6.

Global Rigid Packaging

Market Estimates & Forecast Trend Analysis, by End-use Industry

6.1. Global Rigid Packaging Market Revenue (US$ Billion) Estimates and

Forecasts, by End-use Industry, 2021 - 2034

6.1.1.

Food & Beverage

6.1.2.

Pharmaceuticals

6.1.3.

Personal Care & Cosmetics

6.1.4.

Chemicals

6.1.5.

Industrial Goods

6.1.6.

Household Products

6.1.7.

Others

7.

Global Rigid Packaging

Market Estimates & Forecast Trend Analysis, by Distribution Channel

7.1. Global Rigid Packaging Market Revenue (US$ Billion) Estimates and

Forecasts, by Distribution Channel, 2021 - 2034

7.1.1.

Retail Packaging

7.1.2.

E-commerce Packaging

7.1.3.

Industrial Packaging

7.1.4.

Institutional Packaging

8.

Global Rigid Packaging

Market Estimates & Forecast Trend Analysis, by Region

8.1. Global Rigid Packaging Market Revenue (US$ Billion) Estimates and

Forecasts, by Region, 2021 - 2034

8.1.1.

North America

8.1.2.

Europe

8.1.3.

Asia Pacific

8.1.4.

Middle East & Africa

8.1.5.

Latin America

9.

North America Rigid

Packaging Market: Estimates & Forecast Trend Analysis

9.1. North America Rigid Packaging Market Assessments & Key Findings

9.1.1.

North America Rigid Packaging

Market Introduction

9.1.2.

North America Rigid Packaging

Market Size Estimates and Forecast (US$ Billion) (2021 - 2034)

9.1.2.1.

By Material

9.1.2.2.

By Product Type

9.1.2.3.

By End-use Industry

9.1.2.4.

By Distribution Channel

9.1.2.5.

By Country

9.1.2.5.1.

The U.S.

9.1.2.5.2.

Canada

10. Europe Rigid Packaging Market: Estimates & Forecast Trend

Analysis

10.1.

Europe Rigid Packaging Market

Assessments & Key Findings

10.1.1.

Europe Rigid Packaging Market

Introduction

10.1.2.

Europe Rigid Packaging Market

Size Estimates and Forecast (US$ Billion) (2021 - 2034)

10.1.2.1.

By Material

10.1.2.2.

By Product Type

10.1.2.3.

By End-use Industry

10.1.2.4.

By Distribution Channel

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest of Europe

11. Asia Pacific Rigid Packaging Market: Estimates & Forecast Trend

Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific Rigid Packaging

Market Introduction

11.1.2.

Asia Pacific Rigid Packaging

Market Size Estimates and Forecast (US$ Billion) (2021 - 2034)

11.1.2.1.

By Material

11.1.2.2.

By Product Type

11.1.2.3.

By End-use Industry

11.1.2.4.

By Distribution Channel

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6.

Rest of Asia Pacific

12. Middle East & Africa Rigid Packaging Market: Estimates &

Forecast Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa Rigid

Packaging Market Introduction

12.1.2.

Middle East & Africa Rigid

Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2034)

12.1.2.1.

By Material

12.1.2.2.

By Product Type

12.1.2.3.

By End-use Industry

12.1.2.4.

By Distribution Channel

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4.

Rest of MEA

13. Latin America Rigid Packaging Market: Estimates & Forecast Trend

Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America Rigid Packaging

Market Introduction

13.1.2.

Latin America Rigid Packaging

Market Size Estimates and Forecast (US$ Billion) (2021 - 2034)

13.1.2.1.

By Material

13.1.2.2.

By Product Type

13.1.2.3.

By End-use Industry

13.1.2.4.

By Distribution Channel

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global Rigid Packaging Market

Product Mapping

14.2.

Global Rigid Packaging Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

14.3.

Global Rigid Packaging Market

Tier Structure Analysis

14.4.

Global Rigid Packaging Market

Concentration & Company Market Shares (%) Analysis, 2025

15. Company Profiles

15.1.

Amcor plc

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

15.2.

Berry Global Group, Inc.

15.3.

Silgan Holdings Inc.

15.4.

Ball Corporation

15.5.

Crown Holdings, Inc.

15.6.

Sonoco Products Company

15.7.

DS Smith Plc

15.8.

Greif, Inc.

15.9.

Sealed Air Corporation

15.10.

ALPLA Group

15.11.

Mauser Packaging Solutions

15.12.

Plastipak Holdings, Inc.

15.13.

Ardagh Group S.A.

15.14.

Veritiv Corporation

15.15.

Reynolds Group Holdings Limited

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables