Rigid Plastic Packaging Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Material (Polyethylene terephthalate (PET), Polypropylene (PP), High density polypropylene (HDPE), Others), By Production Process (Extrusion, Injection Molding, Blow Molding, Thermoforming, Others), By Product (Bottles & Jars, Trays & Clamshells, Tubs, Cups, and Pots, Pallets, Drums & Barrels, Crates, Others) By End-user Industry (Food and Beverage, Personal Care, Household, Healthcare, Others) and Geography

2025-10-31

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Rigid Plastic Packaging Market Overview

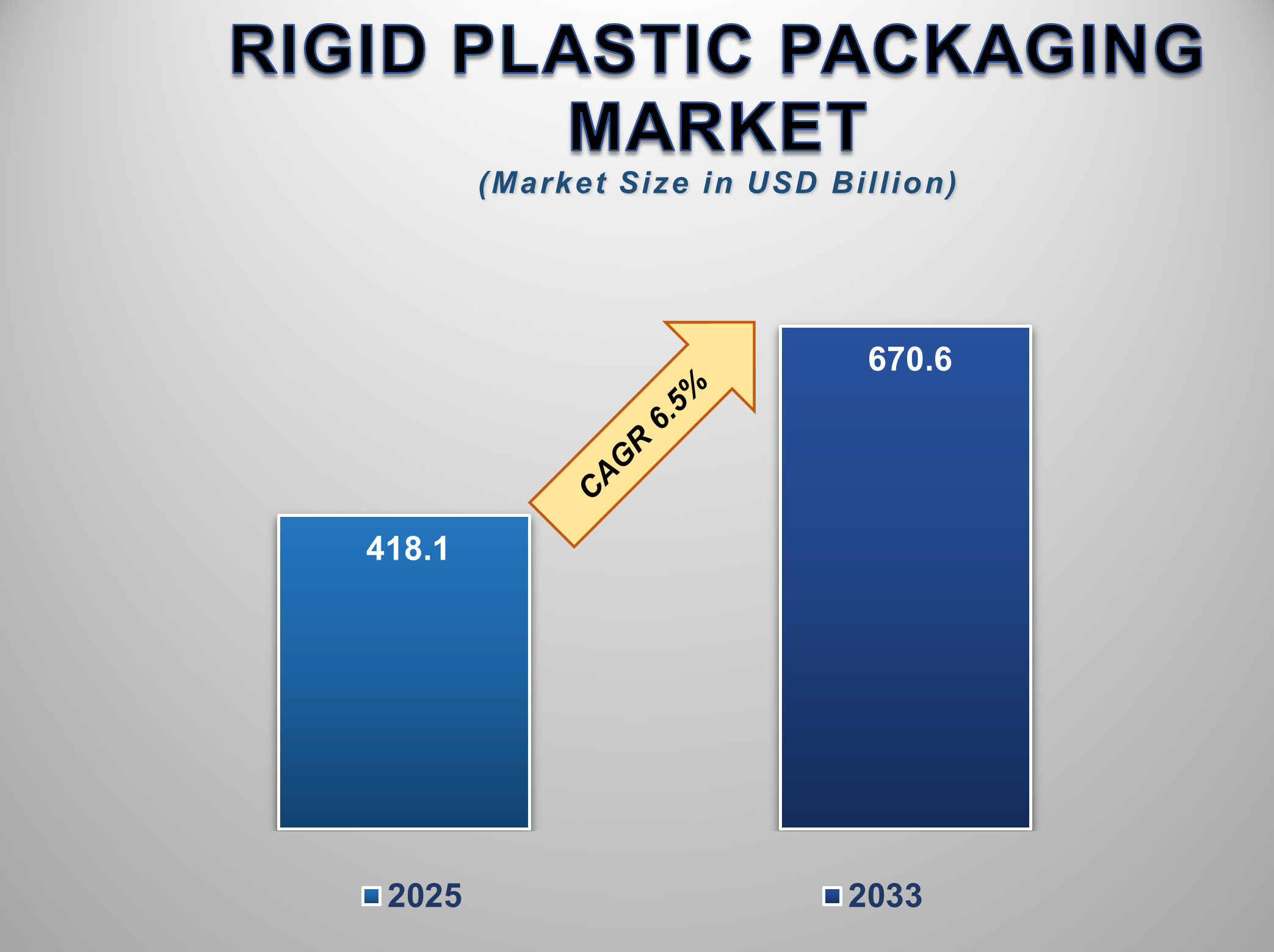

The global Rigid Plastic Packaging Market is projected to grow from USD 418.1 billion in 2025 to USD 670.6 billion by 2033, expanding at a CAGR of 6.5% during the forecast period. Rigid plastic packaging refers to non-flexible plastic formats such as bottles, containers, trays, jars, and closures, typically made from polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), and polystyrene (PS). Its widespread application across industries stems from its durability, product protection, and ability to preserve freshness.

Growth in this market is being

driven by rising packaged food consumption, particularly in urban markets where

convenience and ready-to-eat products are increasingly in demand. Changing

consumer lifestyles, coupled with higher disposable incomes, are prompting

greater reliance on rigid packaging for both perishable and non-perishable

goods. In the pharmaceutical sector, the need for protective, tamper-evident,

and contamination-resistant packaging has fueled adoption, ensuring safe

delivery of medicines and sensitive products. Additionally, the cosmetics and

toiletries industry relies heavily on rigid plastics for their aesthetic

appeal, high barrier properties, and brand differentiation opportunities.

Rigid Plastic Packaging

Market Drivers and Opportunities

Increasing demand from the food & beverage industry is

anticipated to lift the rigid plastic packaging market during the forecast

period

The food and drink sector

continues to be among the largest contributors to the size of the worldwide

rigid plastic packaging industry, driving steady growth and innovation

opportunities. As consumers increasingly opt for convenience, convenient

ready-to-go food, as well as green packaging, rigid plastics provide a perfect

answer through durability, versatility, and protection of the freshness of

products. Packaging containers such as PET bottles, HDPE containers, and

polypropylene tubs are widely used to pack a variety of drinks, sauces, dairy,

and frozen foods. Furthermore, food protection laws in most nations have

increased the demand for rigid plastic materials that are highly protective

against contamination. This has created significant advances in barrier

technology, tamper evidence, as well as resealable covers—all of which are

critical in modern food-grade packaging. Furthermore, the growth of the

worldwide food supermarket market, especially in developing nations, has fueled

demand for attractive-looking as well as convenient packaging. Consequently,

the food and drink sector continues to drive the industry’s strong growth,

enabling it to continue dominating its position in packaging.

Advancements in recycling and sustainability practices are a

vital driver for influencing the growth of the global rigid plastic packaging

market

Sustainability and recycling

innovations are driving the worldwide rigid plastic packaging industry ahead.

As regulatory pressure and consumer awareness continue to rise around

environmental impacts, packaging companies are investing in circular business

models and green product development. Recycling technology, including

closed-loop systems and chemical recycling, is being adopted in rigid plastic

production, making post-consumer plastic waste recyclable into high-end

applications. Bio-based and biodegradable rigid plastics are also being

developed to minimize fossil fuel dependency and carbon footprints. Global

companies are launching recyclable rigid lines of packaging to respond to

consumer needs for more environmentally friendly options. Blending performance

with sustainability—in lightweight designs, in lower materials usage, and in

recyclability feasibility—reshapes the landscape of the industry. These

innovations are not only satisfying compliance requirements but are also

creating new business opportunities, driving brand loyalty, and enabling

long-term market growth.

Rising demand in the healthcare and pharmaceutical sectors is

poised to create significant opportunities in the global rigid plastic

packaging market

The healthcare and pharma

industries worldwide are growing at a fast clip, presenting significant

opportunities to makers of rigid plastic packaging products. Packaging of

medicine, drugs, and healthcare products needs high standards of safety,

protection from contamination, and extended shelf life—all qualities

well-handled by packaging in rigid plastic. An aging population coupled with

increased demand for healthcare services, particularly from growing economies,

has increased the amount of pharma products on the move, both now and in future

years. Also, the pandemic environment has mounted pressure on secure,

tamper-proof, and traceable packaging, especially of vaccines, injectables, and

diagnostic kits. Packaging in rigid plastic provides benefits in terms of

excellent barriers, ease of cleanliness, and formats tailored to suit

customers' preferences (e.g., vials, blister packets, and pill boxes). Also,

the shift towards personalized drugs and in-home, at-home, and point-of-care

solutions raises demand for convenient, portable packaging formats, heightening

demand for packaging in rigid plastic. Regulatory agencies worldwide are

promoting innovation in pharma packaging to ensure patient protection and

compliance, too. Firms specializing in healthcare products using specialized,

compliance-friendly, and innovative rigid plastic packaging are set to

capitalize on long-term growth and profitability in this highly regulated,

high-stakes business opportunity.

Rigid Plastic Packaging Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 670.6 Billion |

|

Market Forecast in 2033 |

USD 418.1 Billion |

|

CAGR % 2025-2033 |

6.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors, and more |

|

Segments Covered |

●

By Material ●

By Production Process ●

By Product ●

By End-user Industry |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

China 9)

India 10)

Japan 11)

South Korea 12)

Australia 13)

Mexico 14)

Brazil 15)

Argentina 16)

Saudi Arabia 17)

UAE 18) South Africa |

Rigid Plastic Packaging Market Report Segmentation Analysis

The Global Rigid Plastic

Packaging Market industry analysis is segmented by Material, by Production

Process, by Product, by End-user Industry, and by Region.

The Polyethylene terephthalate (PET) segment is anticipated

to hold the highest share of the global Rigid Plastic Packaging Market during

the projected timeframe.

The global rigid plastic packaging market is segmented by material into Polyethylene Terephthalate (PET), Polypropylene (PP), High-Density Polyethylene (HDPE), and Others, with PET expected to dominate market share during the forecast period. PET's leadership position stems from its exceptional combination of durability, lightweight properties, optical clarity, and superior moisture/oxygen barrier capabilities, making it the material of choice for beverage bottles, food containers, and personal care packaging. The food and beverage sector, particularly bottled water and soft drink applications, represents the primary growth driver, as manufacturers increasingly favor PET for its ability to maintain product freshness while meeting stringent safety standards.

The injection molding segment dominated the market in 2024

and is predicted to grow at the highest CAGR over the forecast period

By Production Process, the market

is segmented into Extrusion, Injection Molding, Blow Molding, Thermoforming,

and Others. Injection Molding led the market in 2024 and is expected to

register the highest growth rate in the forecast period. Injection Molding

permits high-volume output of complex, detailed rigid plastic parts, making its

applications highly appropriate in food containers, bottle caps, medical

components, and consumer products. Its efficiency, reproducibility, and

capacity to generate strong, detailed packagings have established its position

as a top-preferred choice by producers opting for cost-effective mass

production. The ongoing evolution of smart molds and automation in injection

molding further increased its uptake in various industries, such as food &

beverage, as well as healthcare.

The Food and Beverage segment is predicted to grow at the

highest CAGR over the forecast period

By End-user Industry, the market

is segmented into Food and Beverage, Personal Care, Household, Healthcare, and

Others. The Food and Beverage segment is expected to grow at the highest CAGR

during the forecast period, driven by the rising demand for safe, durable, and

lightweight packaging for perishable and ready-to-eat food products. As global

urbanization accelerates and consumers gravitate toward convenience foods and

on-the-go consumption, rigid plastic containers, trays, and bottles offer

superior product protection and shelf appeal. Moreover, changing lifestyle

trends, the proliferation of online grocery and food delivery services, and

growing awareness around food hygiene and shelf-life are contributing to the

strong demand for rigid plastic packaging in this segment.

The following segments are part of an in-depth analysis of the global

Rigid Plastic Packaging Market:

|

Market Segments |

|

|

By Material |

●

Polyethylene

terephthalate (PET) ●

Polypropylene (PP) ●

High-density

polypropylene (HDPE) ●

Others |

|

By Production Process |

●

Extrusion ●

Injection Molding ●

Blow Molding ●

Thermoforming ●

Others |

|

By Product |

●

Bottles & Jars ●

Trays &

Clamshells ●

Tubs, Cups, and Pots ●

Pallets ●

Drums & Barrels ●

Crates ●

Others |

|

By End-user Industry |

●

Food and Beverage ●

Personal Care ●

Household ●

Healthcare ●

Others |

Rigid Plastic Packaging

Market Share Analysis by Region

Asia Pacific is projected

to hold the largest share of the global rigid plastic packaging market over the

forecast period

Asia Pacific led the worldwide

rigid plastic packaging industry in 2024, occupying a substantial 41.5% share

in the market, and was expected to continue driving its growth during the

forecast period. The dominance of the region can be attributed to its strong

manufacturing base, increasing consumption of packaged food products and

drinks, as well as fast-growing end-use industries like pharmaceuticals,

personal care, and housekeeping. China, India, Japan, and South Korea are

seeing a high rise in consumer purchasing power for convenient, hygienic, and

affordable packaging products, driven by urbanization, increasing disposable

incomes, and organized retail growth. The concentration of numerous plastic

producers, coupled with government-friendly initiatives aimed at encouraging

industry growth, also contributed to fueling the growth of the region’s market.

Continuous investments in lightening the weight of plastic solutions, along

with recycling, are also helping drive growth in the region. The Asia Pacific

market also reaps benefits from a thriving e-commerce sector that’s driving

demand across protective, versus non-protective, packaging formats in logistics

as well as end-of-delivery applications.

North America, on the other hand,

is forecast to record the highest compound annual rate of growth (CAGR) through

the forecast period. Such growth comes as a result of increased consumer

sensitivity towards green packaging, higher demand for recyclable plastics, and

a highly developed food and beverage industry. Pressures from regulation to cut

down on plastic waste, coupled with a higher uptake of new packaging

technology, are also fueling further developments in the region. The U.S. and

Canada are at the forefront of proposals to include post-consumer recycled

plastics, stimulating a circular model of economic stimulation in the packaging

industry.

Rigid Plastic Packaging

Market Competition Landscape Analysis

The global Rigid Plastic

Packaging Market is poised for significant growth, with key players investing

heavily in technology and packaging. These companies are actively engaged in

research and development, strategic partnerships, and large-scale project implementations

to enhance their market positions.

Global Rigid Plastic

Packaging Market Recent Developments News:

●

In November 2022,

STERIMED, the global leader in sterilization packaging solutions, unveiled its

breakthrough material innovation, POLYBOND CGP

85, specifically engineered to meet evolving

healthcare industry demands. This advanced substrate expands the company's

polymer-reinforced cellulose product line, offering enhanced performance

characteristics for medical device sterilization.

●

In November 2022,

Sealed Air launched an innovative, plant-based food packaging solution—a bio-derived resin overwrap tray designed to replace

traditional EPS (expanded polystyrene) meat and poultry packaging. This

sustainable alternative meets stringent food-contact safety standards while

addressing environmental concerns associated with petroleum-based foam trays.

The Global Rigid

Plastic Packaging Market is dominated by

a few large companies, such as

●

Amcor plc

●

Anchor Packaging LLC

●

Arabian Plastic Industrial Company Co.

●

Berry Global Inc.

●

Crown Packaging Int’l

●

DS Smith

●

Dynapackasia

●

Genpak

●

Gerresheimer AG

●

Greif

●

Greiner Packaging

●

Ladain Alyamamah Plastic Factory

●

Manjushree Technopack Ltd.

●

Mold-Tek Packaging Ltd.

●

Nuplas Industries

●

Pactiv Evergreen Inc.

●

PLASTIPAK HOLDINGS, INC.

●

S.E.A. Global Pte. Ltd

●

SILGAN PLASTICS

●

Sonoco Products Company

●

Takween Advanced Industries

●

WINPAK LTD

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Rigid Plastic Packaging Market Introduction and Market Overview

- Objectives of the Study

- Global Rigid Plastic Packaging Market Scope and Market Estimation

- Global Rigid Plastic Packaging Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Rigid Plastic Packaging Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Material of Global Rigid Plastic Packaging Market

- Production Process of Global Rigid Plastic Packaging Market

- Product of Global Rigid Plastic Packaging Market

- End-user Industry of Global Rigid Plastic Packaging Market

- Region of Global Rigid Plastic Packaging Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Key Product/Brand Analysis

- Technological Advancements

- Key Developments

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Insights on Cost-effectiveness of Rigid Plastic Packaging

- Key Regulation

- Global Rigid Plastic Packaging Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Rigid Plastic Packaging Market Estimates & Forecast Trend Analysis, by Material

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020 - 2033

- Polyethylene terephthalate (PET)

- Polypropylene (PP)

- High density polypropylene (HDPE)

- Others

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020 - 2033

- Global Rigid Plastic Packaging Market Estimates & Forecast Trend Analysis, by Production Process

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Production Process, 2020 - 2033

- Extrusion

- Injection Molding

- Blow Molding

- Thermoforming

- Others

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Production Process, 2020 - 2033

- Global Rigid Plastic Packaging Market Estimates & Forecast Trend Analysis, by Product

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Bottles & Jars

- Trays & Clamshells

- Tubs, Cups, and Pots

- Pallets

- Drums & Barrels

- Crates

- Others

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Global Rigid Plastic Packaging Market Estimates & Forecast Trend Analysis, by End-user Industry

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by End-user Industry, 2020 - 2033

- Food and Beverage

- Personal Care

- Household

- Healthcare

- Others

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by End-user Industry, 2020 - 2033

- Global Rigid Plastic Packaging Market Estimates & Forecast Trend Analysis, by Region

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Rigid Plastic Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Rigid Plastic Packaging Market: Estimates & Forecast Trend Analysis

- North America Rigid Plastic Packaging Market Assessments & Key Findings

- North America Rigid Plastic Packaging Market Introduction

- North America Rigid Plastic Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Production Process

- By Product

- By End-user Industry

- By Country

- The U.S.

- Canada

- North America Rigid Plastic Packaging Market Assessments & Key Findings

- Europe Rigid Plastic Packaging Market: Estimates & Forecast Trend Analysis

- Europe Rigid Plastic Packaging Market Assessments & Key Findings

- Europe Rigid Plastic Packaging Market Introduction

- Europe Rigid Plastic Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Production Process

- By Product

- By End-user Industry

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Rest of Europe

- Europe Rigid Plastic Packaging Market Assessments & Key Findings

- Asia Pacific Rigid Plastic Packaging Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Rigid Plastic Packaging Market Introduction

- Asia Pacific Rigid Plastic Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Production Process

- By Product

- By End-user Industry

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Rigid Plastic Packaging Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Rigid Plastic Packaging Market Introduction

- Middle East & Africa Rigid Plastic Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Production Process

- By Product

- By End-user Industry

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Rigid Plastic Packaging Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Rigid Plastic Packaging Market Introduction

- Latin America Rigid Plastic Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Production Process

- By Product

- By End-user Industry

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Rigid Plastic Packaging Market Product Mapping

- Global Rigid Plastic Packaging Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Rigid Plastic Packaging Market Tier Structure Analysis

- Global Rigid Plastic Packaging Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Amcor plc

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Amcor plc

* Similar details would be provided for all the players mentioned below

- Anchor Packaging LLC

- Arabian Plastic Industrial Company Co.

- Berry Global Inc.

- Crown Packaging Int’l

- DS Smith

- Dynapackasia

- Genpak

- Gerresheimer AG

- Greif

- Greiner Packaging

- Ladain Alyamamah Plastic Factory

- Manjushree Technopack Ltd.

- Mold-Tek Packaging Ltd.

- Nuplas Industries

- Pactiv Evergreen Inc.

- PLASTIPAK HOLDINGS, INC.

- E.A. Global Pte. Ltd

- SILGAN PLASTICS

- Sonoco Products Company

- Takween Advanced Industries

- WINPAK LTD

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables