Sciatica Treatment Market Size and Forecast (2026 – 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Treatment Type (Medication, Physical Therapy, Surgical Treatment, and Alternative Therapies); By Drug Type (NSAIDs, Corticosteroids, Muscle Relaxants, and Others); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies); By End-use (Hospitals, Specialty Clinics, Rehabilitation Centers, and Homecare Settings) and Geography

2026-03-12

Healthcare

Swetal (Research Analyst)

Description

Sciatica Treatment Market Overview

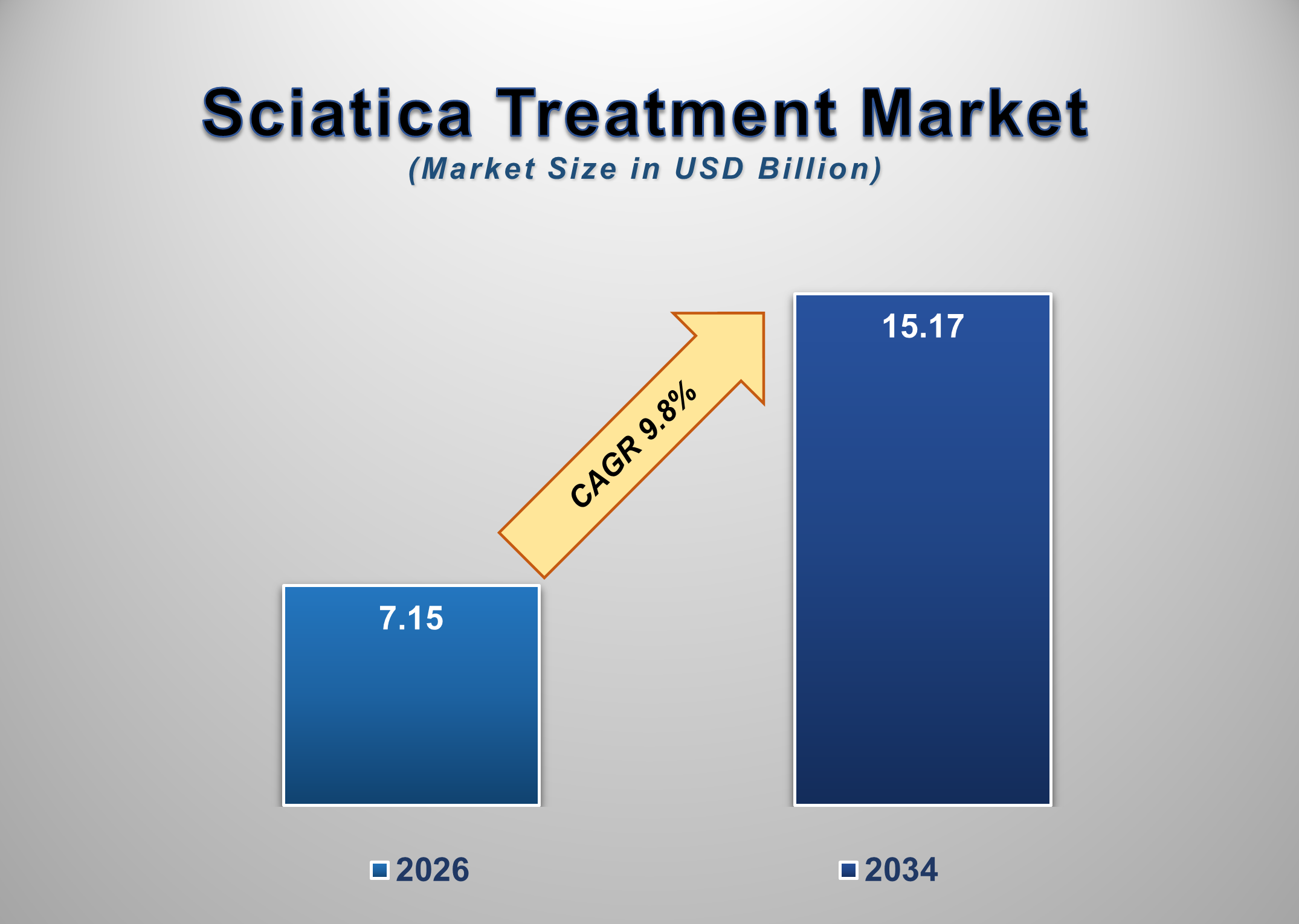

The global Sciatica Treatment Market is experiencing significant growth due to the rising prevalence of lower back pain disorders and nerve compression conditions worldwide. The market is estimated to reach USD 7.15 billion in 2026 and is projected to grow to USD 15.17 billion by 2034, registering a compound annual growth rate (CAGR) of 9.8%during the forecast period. Increasing cases of spinal disorders, sedentary lifestyles, aging populations, and growing awareness regarding early treatment options are key factors driving the expansion of the sciatica treatment market.

Sciatica is a medical condition characterized by pain that radiates along the sciatic nerve, which extends from the lower back through the hips and down each leg. The condition typically occurs when a herniated disk, spinal stenosis, or bone spur compresses part of the nerve, causing inflammation, numbness, and severe pain. Sciatica can significantly affect mobility, daily activities, and overall quality of life, making effective treatment solutions essential for patients experiencing chronic pain symptoms.

The treatment of sciatica involves a combination of pharmacological therapies, physical rehabilitation, and surgical interventions, depending on the severity of the condition. Medications such as nonsteroidal anti-inflammatory drugs (NSAIDs), muscle relaxants, and corticosteroids are commonly prescribed to relieve pain and reduce inflammation. In addition, physical therapy programs that include stretching exercises, posture correction, and strengthening routines are widely recommended to improve spinal health and prevent recurrence of symptoms.

Furthermore, advances in minimally invasive surgical techniques and spinal care technologies have improved treatment outcomes for patients with severe or persistent sciatica. Healthcare providers are increasingly adopting innovative therapeutic approaches such as nerve decompression procedures, spinal injections, and regenerative therapies to provide long-term relief. As the global burden of musculoskeletal disorders continues to increase, the demand for effective sciatica treatment solutions is expected to grow steadily.

Sciatica Treatment Market Drivers and Opportunities

Rising Prevalence of Lower Back Disorders Is Driving Market Growth

One of the primary drivers of the sciatica treatment market is the increasing prevalence of lower back disorders and spinal conditions across the global population. Lower back pain is among the most common health issues worldwide and is often associated with conditions such as herniated discs, degenerative disc disease, and spinal stenosis, which can lead to sciatic nerve compression. According to various healthcare studies, millions of individuals suffer from chronic back pain each year, with sciatica being one of the leading causes of nerve-related pain.

Sedentary lifestyles, poor posture habits, and prolonged sitting associated with modern work environments are contributing to the rising incidence of spinal health issues. Office workers, drivers, and individuals who perform repetitive physical activities are particularly vulnerable to developing sciatica symptoms. In addition, the growing adoption of digital devices and extended screen time has increased the risk of musculoskeletal problems related to improper body posture.

Healthcare systems worldwide are increasingly focusing on improving the diagnosis and management of spinal disorders. Early diagnosis and appropriate treatment of sciatica can significantly reduce long-term complications and improve patient mobility. As awareness regarding spinal health and pain management continues to grow, the demand for effective sciatica treatment solutions is expected to rise.

Growing Aging Population Increases Demand for Pain Management Therapies

The rapidly growing aging population worldwide represents another significant factor contributing to the expansion of the sciatica treatment market. Aging individuals are more susceptible to degenerative spinal conditions such as disc degeneration, osteoarthritis, and spinal stenosis, all of which can lead to sciatic nerve compression and chronic nerve pain.

Older adults often experience reduced flexibility and weakened spinal structures, making them more vulnerable to nerve compression disorders. As a result, many elderly patients require long-term treatment strategies that include medications, physiotherapy, and pain management procedures. Healthcare providers are increasingly focusing on developing comprehensive treatment plans that help elderly patients manage chronic pain while maintaining mobility and independence.

In addition, the growing number of orthopedic clinics and rehabilitation centers specializing in spinal care is improving patient access to treatment options. Governments and healthcare organizations are also investing in programs aimed at improving musculoskeletal health among aging populations. These factors collectively contribute to the growing demand for sciatica treatment services across global healthcare markets.

Advancements in Minimally Invasive Surgical Techniques Create Opportunities

Technological advancements in spinal surgery and pain management therapies are creating new growth opportunities within the sciatica treatment market. Traditional surgical procedures for severe sciatica often involved extensive spinal operations that required long recovery periods. However, modern medical innovations have introduced minimally invasive surgical techniques that allow physicians to treat nerve compression conditions with reduced tissue damage and faster recovery times.

Minimally invasive procedures such as microdiscectomy, endoscopic spinal surgery, and spinal decompression techniques have become increasingly popular due to their effectiveness in relieving nerve pressure while minimizing surgical risks. These procedures allow surgeons to remove damaged disc material or bone fragments that are pressing against the sciatic nerve, thereby alleviating pain and restoring nerve function.

Additionally, emerging treatment approaches such as regenerative medicine therapies, including platelet-rich plasma (PRP) injections and stem cell-based treatments, are being explored as potential solutions for managing nerve-related pain conditions. These innovative therapies aim to promote tissue healing and reduce inflammation around affected nerves. As medical research continues to advance, new therapeutic options are expected to further expand the range of treatment solutions available for patients suffering from sciatica.

Sciatica Treatment Market Scope

Sciatica Treatment Market Report Segmentation Analysis

The global sciatica treatment market industry analysis is segmented based on treatment type, drug category, distribution channel, end-use industry, and geographical region.

Medication Segment Dominates the Treatment Market

Based on treatment type, the market is divided into medication, physical therapy, surgical treatment, and alternative therapies. The medication segment currently holds the largest share because pharmaceutical treatments are typically the first line of therapy for patients experiencing sciatica symptoms. Pain-relieving medications and anti-inflammatory drugs are widely prescribed to reduce nerve inflammation and provide short-term relief from severe pain.

Medications such as NSAIDs, corticosteroids, and muscle relaxants help reduce swelling around the affected nerve and improve patient comfort. These treatments are commonly used in combination with physical therapy programs to improve spinal mobility and prevent further nerve irritation.

Hospital Pharmacies Hold the Largest Share

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies currently account for the largest market share due to the high volume of prescription medications provided within hospital settings. Many patients diagnosed with sciatica receive treatment through hospital-based healthcare services where medications and therapeutic interventions are administered.

Retail pharmacies also represent a significant distribution channel as patients frequently purchase prescribed medications for ongoing pain management. Meanwhile, online pharmacies are gaining popularity due to the increasing adoption of digital healthcare services and convenient medication delivery options.

Hospitals Segment Leads the End-use Market

By end-use, the sciatica treatment market is segmented into hospitals, specialty clinics, rehabilitation centers, and home care settings. Hospitals currently dominate the market because they offer comprehensive diagnostic and treatment services for patients suffering from spinal disorders and nerve-related pain conditions.

Hospitals provide access to advanced imaging technologies, specialized medical professionals, and surgical facilities required for treating severe cases of sciatica. Additionally, hospitals often collaborate with physiotherapy departments and rehabilitation specialists to develop integrated treatment programs for patients experiencing chronic nerve pain.

Sciatica Treatment Market Share Analysis by Region

North America currently holds the largest share of the global sciatica treatment market due to advanced healthcare infrastructure, high awareness regarding musculoskeletal disorders, and strong availability of specialized treatment services. The region also benefits from the presence of leading pharmaceutical companies and advanced spinal care centers.

Europe represents another significant market for sciatica treatment solutions. Countries such as Germany, the United Kingdom, and France have well-developed healthcare systems that support early diagnosis and effective management of spinal disorders. Increasing government investments in healthcare services and rehabilitation programs are further supporting market growth in the region.

The Asia-Pacific region is expected to experience the fastest growth during the forecast period. Rapid urbanization, rising healthcare expenditure, and growing awareness regarding spinal health are driving demand for sciatica treatment services across countries such as China, India, Japan, and South Korea.

Global Sciatica Treatment Market Recent Developments News

● In February 2025, Pfizer expanded its pain management research programs focusing on nerve-related pain conditions, including sciatica.

● In September 2024, Medtronic introduced advanced minimally invasive spinal surgery technologies designed to improve treatment outcomes for patients suffering from nerve compression disorders.

● In June 2024, Abbott launched new pain management solutions aimed at improving nerve stimulation therapies for chronic back pain patients.

Competitive Landscape

Major companies operating in the global Sciatica Treatment Market include:

● Pfizer Inc.

● Johnson & Johnson

● Abbott Laboratories

● Medtronic

● Novartis AG

● Eli Lilly and Company

● GlaxoSmithKline

● Sanofi

● AstraZeneca

● Teva Pharmaceutical Industries

● Boston Scientific

● Stryker Corporation

● Zimmer Biomet

● Amgen Inc.

● Bayer AG

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

Sciatica Treatment Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables