Global Scooter Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share, And Industry Analysis Report Coverage: By Product Type (Electric Scooter, Standard Scooters), By End Use (Personal Use, Commercial Use), And Geography

2025-10-31

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Global Scooter Market Overview

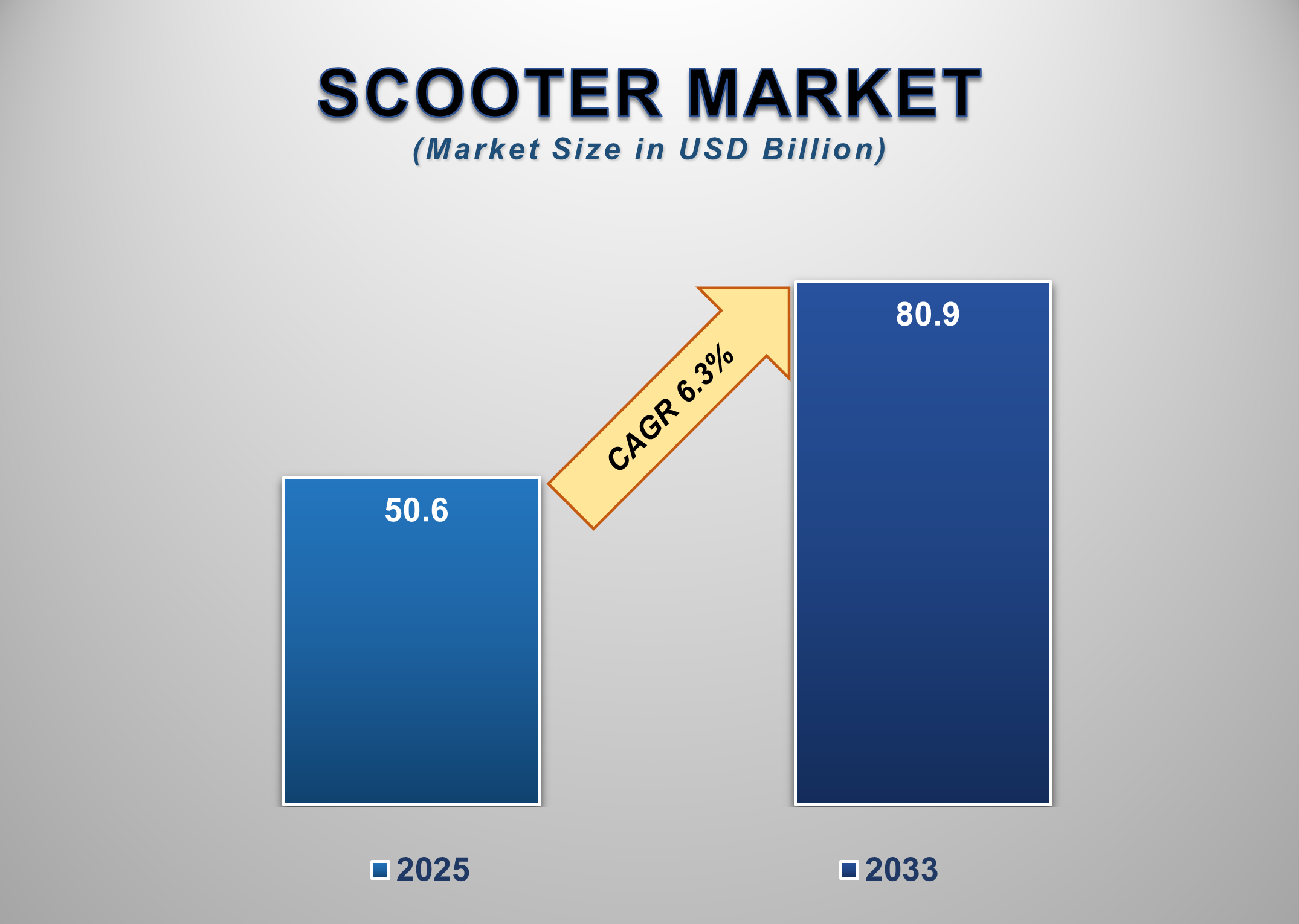

The Global Scooter Market Size is

projected to Grow from US$ 50.6 Billion in 2025 to US$ 80.9 Billion by 2033,

registering a steady CAGR of 6.3% during the forecast period. Market growth is

primarily fueled by rapid urbanization, rising fuel costs, and increasing

environmental awareness, which are reshaping urban mobility patterns worldwide.

Scooters, with their compact design, fuel efficiency, and affordability, are

emerging as a preferred mode of transport across densely populated urban

centers in Asia-Pacific, Europe, and Latin America, where traffic congestion

and limited parking are significant challenges.

A key driver of expansion is the

rising adoption of electric scooters (e-scooters), which are gaining traction

as a sustainable, eco-friendly alternative to conventional two-wheelers amid

growing concerns about climate change and vehicular emissions. Advances in

battery technology, charging infrastructure, and lightweight materials are

making e-scooters more efficient and accessible, aligning with global

sustainability goals. In addition, supportive government policies and

incentives, including subsidies for electric vehicles and regulatory

initiatives promoting clean mobility, are accelerating adoption.

Global Scooter Market

Drivers and Opportunities

Increasing Fuel Prices And Urban Congestion Is Anticipated To

Lift The Scooter Market During The Forecast Period

The global scooter market is

experiencing significant growth, driven primarily by soaring fuel prices and

worsening urban traffic congestion. As fossil fuel costs hit record highs

worldwide, consumers are increasingly turning to scooters as an economical

alternative for daily commuting. These vehicles, whether fuel-efficient

gas-powered models or electric variants, offer substantial savings on

transportation costs while addressing the practical challenges of crowded city

environments. In dense urban areas, scooters provide distinct advantages over

larger vehicles, enabling faster navigation through traffic, easier parking,

and reduced commute times.

According to data from the Bureau

of Transportation Statistics, the rapid adoption of shared micromobility

systems underscores this shift. While fewer than 80 U.S. cities had such

systems in 2015 (mostly docked bikes), today, over 200 cities offer shared

mobility options, with dockless e-scooters now the most prevalent. Beyond

convenience, the lower total cost of ownership, including maintenance,

insurance, and energy expenses, makes scooters particularly appealing to

students, delivery workers, and urban professionals. Market trends suggest

these factors will continue fueling demand, especially as urbanization

intensifies and infrastructure struggles to keep pace with growing populations.

Additionally, government incentives for electric vehicles and advancements in

battery technology are accelerating the transition to e-scooters, further

solidifying their role in sustainable urban mobility. With their affordability,

efficiency, and adaptability to congested environments, scooters are poised to

remain a critical solution for modern transportation challenges in the years

ahead.

Growth in e-commerce and last-mile delivery is a vital driver

for influencing the growth of the global scooter market.

The growth in the global

e-commerce industry has triggered huge demand for effective last-mile delivery

solutions that will positively impact the scooter market. Food delivery apps,

online shopping giants, and courier delivery have increased demand for agile,

speedy, and economical delivery vehicles. Scooters provide the perfect solution

because of their low operating costs, high maneuverability, and capability of

moving in and out of tightly packed city centers. Electric scooters

specifically are being favored among delivery fleets because businesses want to

cut down their carbon footprint and meet sustainability goals. Many delivery

companies also form alliances with scooter manufacturers to roll out customized

delivery scooters with increased storage capacity and GPS tracking. These

alliances and business model shifts are expected to drive steady growth in

scooter sales. E-commerce will continue to move in the right direction, with

rapid growth being seen in emerging economies specifically, and scooters will

be a key element of the delivery ecosystem, thus causing market size and demand

to rise substantially.

Technological Advancements in Electric Scooters are poised to

Create Significant Opportunities in the Global Scooter Market

The global scooter market is

undergoing a technological revolution, particularly in the electric segment,

driven by breakthroughs in battery and motor systems. Lithium-ion and

solid-state batteries now offer greater energy density, faster charging, and extended

range, making e-scooters viable for daily commutes and commercial delivery

services. Enhanced motor technology delivers smoother acceleration, higher

torque, and quieter operation, while regenerative braking improves energy

efficiency. Smart features like GPS tracking, Bluetooth connectivity, and

anti-theft systems are becoming standard, meeting demand for integrated

mobility solutions. Battery-swapping networks and modular designs are

overcoming charging infrastructure challenges, particularly benefiting fleet

operators and shared mobility services. Sustainability is also a key focus,

with manufacturers adopting recyclable materials and eco-friendly production

methods. Government incentives and growing environmental awareness are

accelerating adoption, positioning e-scooters as a cornerstone of urban

transportation. These advancements, combined with cost efficiency and traffic

adaptability, ensure strong market growth, with electric models leading the

charge in redefining future mobility.

Global Scooter Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 50.6 Billion |

|

Market Forecast in 2033 |

USD 80.9 Billion |

|

CAGR % 2025-2033 |

6.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors, and more |

|

Segments Covered |

●

By Product Type ●

By End-use |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19) South Africa |

Global Scooter Market Report Segmentation Analysis

The Global Scooter Market

industry analysis is segmented by Product Type, by End-use and by Region.

The Electric Scooter segment is anticipated to hold the

highest share of the global Scooter Market during the projected timeframe

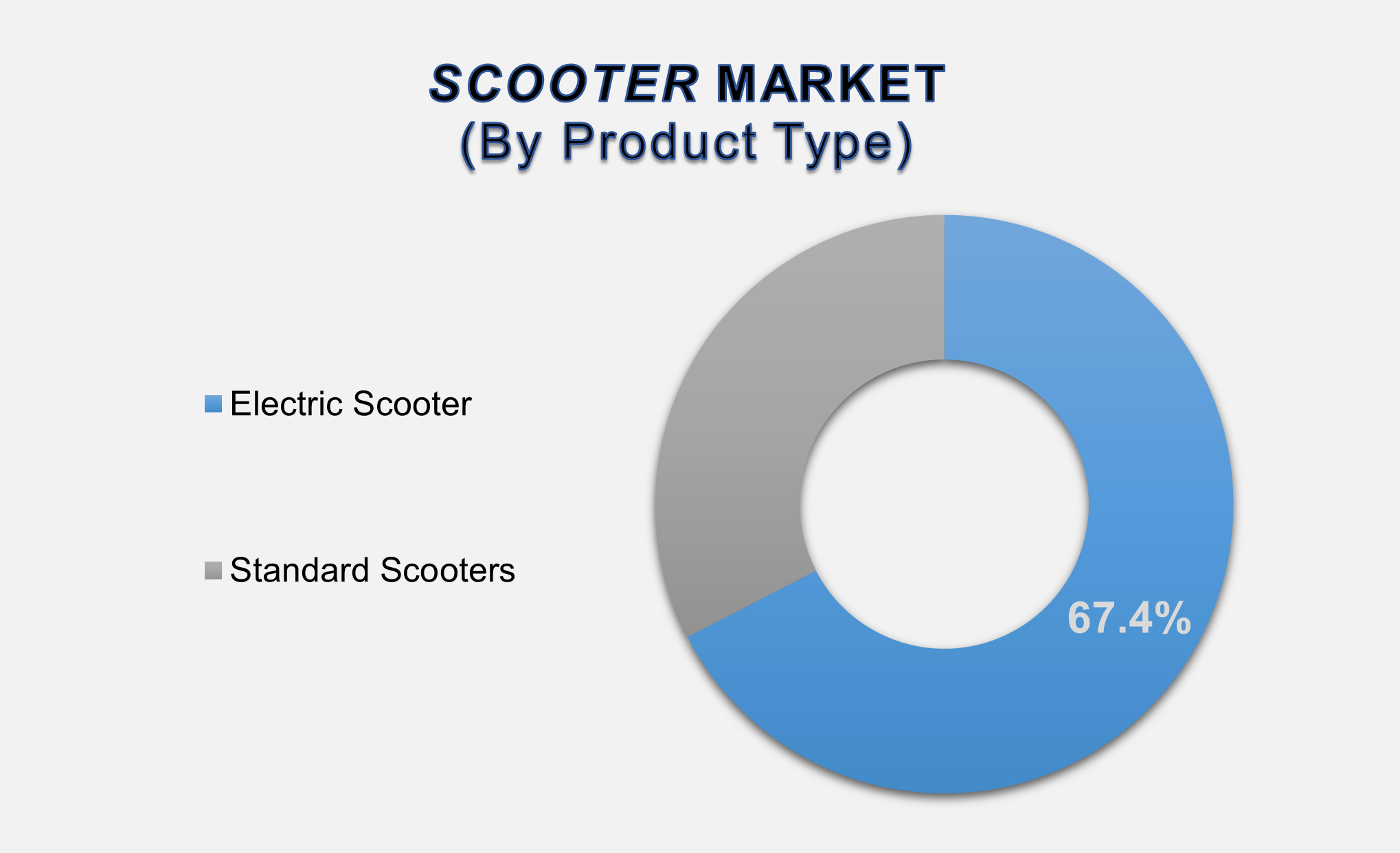

By Product Type, the market is

segmented into Electric Scooter and Standard Scooters. In 2024, the Electric

Scooter segment is anticipated to hold the highest share of over 67.4% in the

global Scooter Market. This growth is driven by their compelling economic and

environmental advantages. With significantly lower operating costs compared to

traditional vehicles and minimal maintenance requirements, e-scooters present

an attractive mobility solution for cost-conscious consumers. Technological

breakthroughs in battery systems have addressed early limitations, now

delivering extended ranges and faster charging times that enhance practicality

for daily commuting. Governments worldwide are further stimulating adoption

through financial incentives like purchase subsidies, tax rebates, and

infrastructure development programs as part of broader decarbonization

initiatives.

The Personal Use segment is anticipated to hold the highest

share of the market over the forecast period

By End Use, the market is

segmented into Personal Use and Commercial Use. The Personal Use segment is

anticipated to hold the highest share of the market over the forecast period.

The increased need for affordable, convenient, and personal transportation

options in densely populated urban areas has made scooters a preferred mode of

mobility. Consumers are increasingly opting for scooters for daily commuting,

leisure travel, and last-mile connectivity. Scooters offer cost-efficiency,

ease of parking, and agility in traffic, making them ideal for individual

users. Moreover, rising fuel prices have nudged consumers toward electric

scooters, which provide long-term cost benefits. The younger demographic,

particularly in Asia-Pacific and Europe, is adopting scooters as a stylish and

practical mobility solution. In parallel, the availability of financing

options, digital purchase platforms, and subscription-based ownership models is

making scooters more accessible. As these trends continue, the personal use segment

is forecasted to experience sustained growth, further reinforcing its dominant

position in the global scooter market.

The following segments are part of an in-depth analysis of the global

Scooter Market:

|

Market Segments |

|

|

By Product Type |

●

Electric Scooter o

Conventional

Electric Scooter o

Swappable Electric

Scooter ●

Standard Scooters |

|

By End-use |

●

Personal Use ●

Commercial Use o

Delivery &

Courier Services o

Bike-sharing

Platforms o

Rentals & Fleets |

Global Scooter Market

Share Analysis by Region

Asia Pacific Is Projected

To Hold The Largest Share Of The Global Scooter Market Over The Forecast Period

The Asia Pacific region was the

market-leading segment in the Global Scooter Market with a significant 56.8%

share in 2024. This leadership is largely attributed to the region’s large

population base, fast urbanization, and the growing demand for convenient and

affordable personal mobility solutions. Nations such as China, India, Vietnam,

and Indonesia are witnessing increasing scooter sales because of high traffic

congestion, increasing middle-class incomes, and the demand for fuel-efficient

personal mobility alternatives to cars. Moreover, having several major scooter

manufacturers and substantial local manufacturing capabilities places the Asia

Pacific in the center of both conventional and electric scooters. Rising

environment-related issues and government incentives towards electric

mobility—subsidies, incentives, and required infrastructure development—also

further speed up electric scooter adoption in the region. Increasing fuel costs

and increased e-commerce delivery logistics services also drive higher

utilization of scooters in the region to cater to last-mile delivery.

Investments in smart urban mobility solutions and ongoing innovation in battery

technology and lightweight materials in the region enhance scooter performance

and attractiveness. In total, all these trends propel the region’s long-term

growth and leadership in the global market.

At the same time, the highest

CAGR in the forecast period is expected to be registered in North America on

account of increasing use of electric scooters for personal and micro-mobility

use cases. This region is witnessing increased cultural acceptance of

eco-friendly and space-efficient urban mobility in cities such as Los Angeles,

New York, and Toronto. Favorable government policies towards green transport

and expanding venture capital investments in shared mobility startups are

contributing to market growth momentum. The convergence of smart technology and

app-based platforms is also contributing to user interaction and scooter uptake

in the market in North America.

Global Scooter Market

Competition Landscape Analysis

The Global Scooter Market is

marked by robust competition among key players focusing on innovation,

strategic expansion, and sustainability. Continuous research and development

efforts lead to the introduction of advanced features/technology in the Scooter

with improved performance characteristics, catering to evolving industry

demands.

Global Scooter Market

Recent Developments News:

●

In April 2024, Indian

EV manufacturer Ola Electric introduced its latest offering – the S1 X electric

scooter series, available in 2 kWh, 3 kWh, and 4 kWh battery configurations.

The flagship 4 kWh variant delivers an impressive 190 km range on a single

charge while boasting rapid acceleration, achieving 0-40 km/h in just 3.3

seconds.

●

In April 2024, Indian

EV maker Ather Energy launched its latest model, the Rizta, featuring a 2.9 kWh

battery pack that delivers an IDC-certified range of 123 km on a single charge.

Designed for urban commuters, the scooter balances performance and efficiency

while maintaining Ather's signature smart features and connected ecosystem.

The Global Scooter Market is dominated by a few large

companies, such as

●

Bajaj

●

Bird Rides, Inc.

●

Gogoro

●

GOTRAX

●

Hero Electric

●

Honda

●

KYMCO

●

Neutron Holdings, Inc.

●

Ninebot Ltd

●

NIU

●

OKAI Inc

●

Razor USA LLC

●

Segway Inc.

●

Spin

●

Suzuki

●

TVS

●

Uber Technologies Inc.

●

Vespa

●

Yadea Technology Group Co., Ltd.

●

Yamaha

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global

Scooter Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Scooter Market Scope and

Market Estimation

1.2.1.Global Scooter Overall Market

Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Scooter Market Revenue

Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3. Market Segmentation

1.3.1.Product Type of Global Scooter

Market

1.3.2.End Use of Global Scooter Market

1.3.3.Region of Global Scooter Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Bn) Analysis

2020 – 2024 and Forecast, 2025 – 2033

2.4. Demand and Opportunity

Assessment

2.5. Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact Analysis of Drivers and

Restraints

2.6. Key Product/Brand Analysis

2.7. Technological Advancements

2.8. Key Developments

2.9. Porter’s Five Forces Analysis

2.9.1.Bargaining Power of Suppliers

2.9.2.Bargaining Power of Buyers

2.9.3.Threat of Substitutes

2.9.4.Threat of New Entrants

2.9.5.Competitive Rivalry

2.10. PEST Analysis

2.10.1. Political Factors

2.10.2. Economic Factors

2.10.3. Social Factors

2.10.4. Technology Factors

2.11. Insights on Cost-effectiveness

of Scooter

2.12. Key Regulation

3.

Global Scooter Market Estimates & Historical Trend Analysis (2020 - 2024)

4.

Global Scooter Market Estimates & Forecast Trend Analysis, by

Product Type

4.1. Global Scooter Market Revenue

(US$ Bn) Estimates and Forecasts, by Product Type, 2020 - 2033

4.1.1.Electric Scooter

4.1.1.1.

Conventional

Electric Scooter

4.1.1.2.

Swappable

Electric Scooter

4.1.2.Standard Scooters

5.

Global Scooter Market Estimates & Forecast Trend Analysis, by

End Use

5.1. Global Scooter Market Revenue

(US$ Bn) Estimates and Forecasts, by End Use, 2020 - 2033

5.1.1.Personal Use

5.1.2.Commercial Use

5.1.2.1.

Delivery

& Courier Services

5.1.2.2.

Bike-sharing

Platforms

5.1.2.3.

Rentals

& Fleets

6.

Global Scooter Market Estimates & Forecast Trend Analysis,

by Region

6.1. Global Scooter Market Revenue

(US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7.

North

America Scooter Market: Estimates & Forecast Trend Analysis

7.1.

North

America Scooter Market Assessments & Key Findings

7.1.1.North America Scooter Market

Introduction

7.1.2.North America Scooter Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Product Type

7.1.2.2. By End Use

7.1.2.3. By Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8.

Europe

Scooter Market: Estimates & Forecast Trend Analysis

8.1. Europe Scooter Market

Assessments & Key Findings

8.1.1.Europe Scooter Market

Introduction

8.1.2.Europe Scooter Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product Type

8.1.2.2. By End Use

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6. Rest

of Europe

9.

Asia

Pacific Scooter Market: Estimates & Forecast Trend Analysis

9.1. Asia Pacific Market Assessments

& Key Findings

9.1.1.Asia Pacific Scooter Market

Introduction

9.1.2.Asia Pacific Scooter Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product Type

9.1.2.2. By End Use

9.1.2.3. By Country

9.1.2.3.1. China

9.1.2.3.2. Japan

9.1.2.3.3. India

9.1.2.3.4. Australia

9.1.2.3.5. South Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Scooter

Market: Estimates & Forecast Trend

Analysis

10.1. Middle East & Africa Market

Assessments & Key Findings

10.1.1. Middle

East & Africa Scooter

Market Introduction

10.1.2. Middle

East & Africa Scooter

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product Type

10.1.2.2. By End Use

10.1.2.3. By Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. Turkey

10.1.2.3.4. South

Africa

10.1.2.3.5. Rest of

MEA

11. Latin America

Scooter Market: Estimates &

Forecast Trend Analysis

11.1. Latin America Market Assessments

& Key Findings

11.1.1. Latin America Scooter Market

Introduction

11.1.2. Latin America Scooter Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product Type

11.1.2.2. By End Use

11.1.2.3. By Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest of

LATAM

12. Country Wise Market:

Introduction

13. Competition Landscape

13.1. Global Scooter Market Product

Mapping

13.2. Global Scooter Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

13.3. Global Scooter Market Tier

Structure Analysis

13.4. Global Scooter Market

Concentration & Company Market Shares (%) Analysis, 2024

14. Company Profiles

14.1.

Bajaj

14.1.1. Company Overview & Key Stats

14.1.2. Financial Performance & KPIs

14.1.3. Product Portfolio

14.1.4. SWOT Analysis

14.1.5. Business Strategy & Recent

Developments

* Similar details would be provided

for all the players mentioned below

14.2. Bird Rides,

Inc.

14.3. Gogoro

14.4. GOTRAX

14.5. Hero

Electric

14.6. Honda

14.7. KYMCO

14.8. Neutron

Holdings, Inc.

14.9. Ninebot

Ltd

14.10. NIU

14.11. OKAI Inc

14.12. Razor USA

LLC

14.13. Segway

Inc.

14.14. Spin

14.15. Suzuki

14.16. TVS

14.17. Uber

Technologies Inc.

14.18. Vespa

14.19. Yadea

Technology Group Co., Ltd.

14.20. Yamaha

14.21. Others

15. Research

Methodology

15.1. External Transportations /

Databases

15.2. Internal Proprietary Database

15.3. Primary Research

15.4. Secondary Research

15.5. Assumptions

15.6. Limitations

15.7. Report FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables