Security Service Edge Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Component (Solutions and Services), By Organization Size (Large Enterprises and Small & Medium-sized Enterprises), By Vertical (BFSI, IT & Telecommunications, Government, Healthcare, Retail & E-commerce, Manufacturing, and Others) And Geography

2025-12-05

ICT

Ekta Chaurasia (Team Lead)

Description

Security Service Edge Market Overview

The Security Service Edge (SSE) Market is poised for explosive growth from 2025 to 2033, fueled by the permanent shift to hybrid work models, widespread cloud adoption, and the increasing sophistication of cyber threats targeting distributed users and data. The market is projected to be valued at approximately USD 4.5 billion in 2025 and is forecasted to reach nearly USD 10.1 billion by 2033, exhibiting a remarkable compound annual growth rate (CAGR) of 10.9% during this period.

Security Service Edge is a foundational

cloud-based security framework that delivers integrated, secure access to the

web, cloud services, and private applications. SSE converges key security

functions, including Zero Trust Network Access

(ZTNA), Secure Web Gateway (SWG), Cloud Access Security Broker (CASB), and

Firewall as a Service (FWaaS), into a single,

unified platform. The market's expansion is driven by the critical need to

secure a borderless workforce, reduce the complexity and cost of traditional security

appliances, and enforce consistent data security and compliance policies

regardless of user location.

Factors such as the escalating frequency of data

breaches, stringent regulatory requirements, and the strategic convergence of

SSE with SD-WAN into the broader SASE (Secure Access Service Edge) framework

are key contributors to market growth. North America currently holds the

largest market share due to early technology adoption and a high concentration

of cybersecurity vendors, while the Asia-Pacific region is expected to be the

fastest-growing market, fueled by rapid digital transformation and increasing cybersecurity

investments.

Security

Service Edge Market Drivers and Opportunities

The Paradigm Shift to Hybrid Work and Cloud-Centric Operations is the Primary Market Driver

The most significant driver for the SSE market

is the irreversible transition to hybrid and remote work models. This has

dismantled the traditional corporate network perimeter, making legacy security

architectures like VPNs inadequate and vulnerable. Organizations are urgently

seeking solutions that can provide secure, seamless, and performant access to

applications hosted in public clouds or data centers for users working from

anywhere. SSE directly addresses this need by moving security enforcement to

the cloud, closer to the user and the data, enabling a "never trust,

always verify" Zero Trust approach that is essential for modern business

continuity.

Escalating Cyber Threats and Stringent Data

Protection Regulations are Accelerating Adoption

The rising volume and sophistication of

cyberattacks, including phishing, ransomware, and data exfiltration, are

compelling organizations to rethink their security posture. Simultaneously,

stringent data privacy and compliance regulations like GDPR, CCPA, and others

mandate robust data protection measures. SSE solutions provide centralized

visibility and control over data access and movement across all cloud services

and internet traffic, helping organizations prevent data loss and demonstrate

compliance. This powerful combination of threat mitigation and regulatory

adherence is a major catalyst for market growth.

The Convergence with SD-WAN and the Proliferation of AI-driven security Present Significant Opportunities

The strategic convergence of SSE with

Software-Defined Wide Area Network (SD-WAN) to form the complete SASE

architecture presents a massive opportunity for vendors and service providers.

As enterprises modernize their networks, the demand for integrated SASE

offerings is skyrocketing. Furthermore, the integration of Artificial

Intelligence (AI) and Machine Learning (ML) within SSE platforms offers a

substantial growth frontier. Opportunities lie in developing AI-powered

capabilities for advanced threat detection, anomalous user behavior analytics, and automated policy enforcement, which can

significantly improve security efficacy and reduce the burden on IT teams.

Security Service Edge

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.5 Billion |

|

Market Forecast in 2033 |

USD 10.1 Billion |

|

CAGR % 2025-2033 |

10.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Component ●

By Organisation

Size ●

By Vertical |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Security Service Edge

Market Report Segmentation Analysis

The global Security Service Edge

Market industry analysis is segmented by Component, by Organization Size, by

Vertical, and by Region.

The Solutions segment is

anticipated to command a dominant market share in 2025.

The Component segment is categorized into

Solutions and Services. The Solutions segment, which includes the integrated

platform and its core functionalities (ZTNA, SWG, CASB), is the largest revenue

generator. This is due to the critical need for the core security technology

itself. The Services segment (including professional and managed services) is

also growing rapidly as organizations seek expertise for implementation,

integration, and ongoing management of their complex SSE environment.

The Large Enterprises segment is projected to be

the major adopter, but SMEs present high growth potential.

The Organization Size segment is divided into

Large Enterprises and Small & Medium-sized Enterprises (SMEs). Large

Enterprises currently lead the market share due to their complex, distributed

IT environments, larger security budgets, and urgent need to secure a global

workforce. However, the SME segment is expected to grow at a significant rate,

as cloud-based SSE offers a cost-effective, scalable, and easy-to-manage

security solution that does not require heavy upfront investment in hardware,

making enterprise-grade security accessible to smaller organizations.

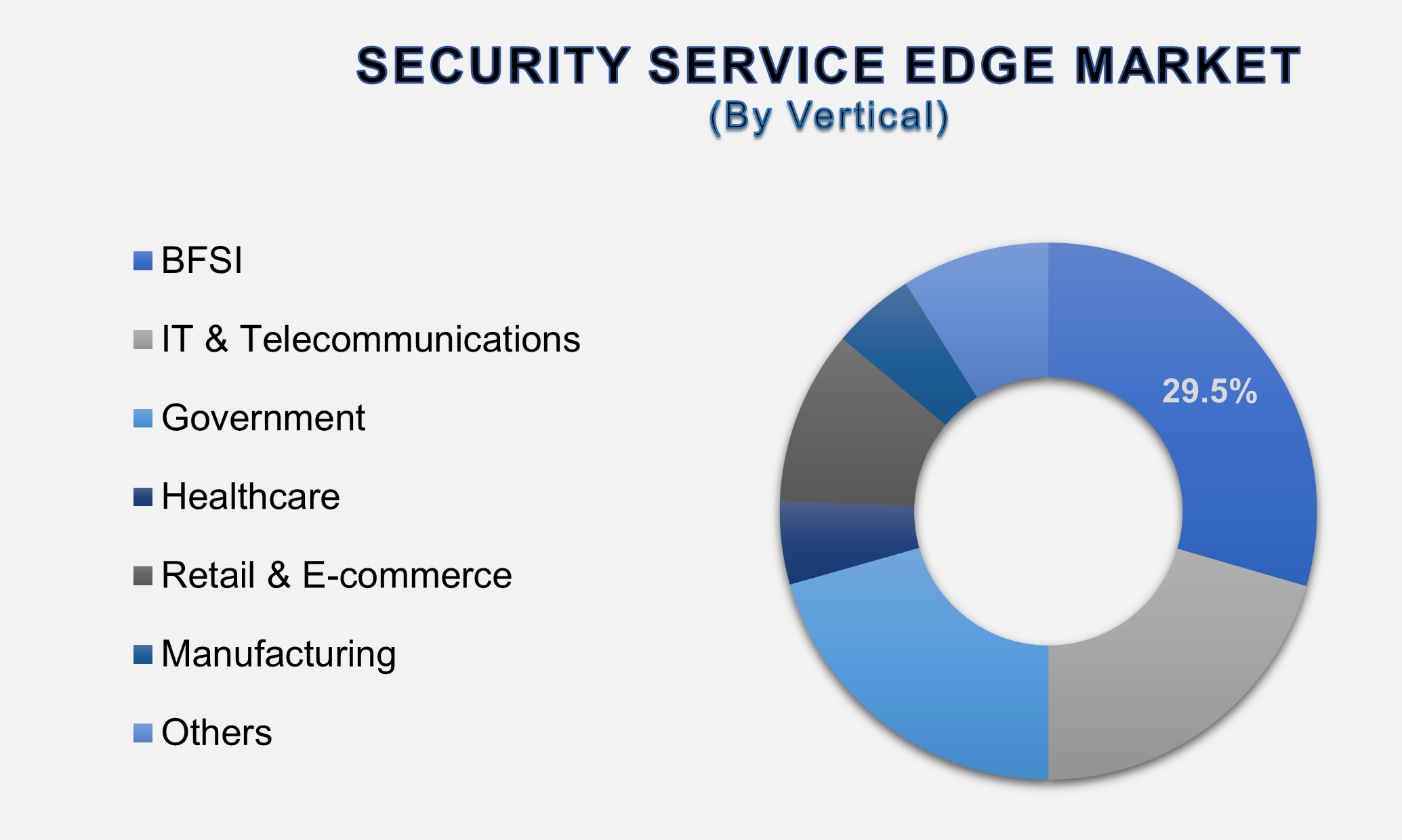

The BFSI and IT & Telecommunications

verticals hold the largest market share.

The BFSI (Banking, Financial Services, and

Insurance) and IT & Telecommunications verticals are the dominant adopters

of Security Service Edge (SSE) due to their unique and pressing security needs

in a distributed digital landscape. For the BFSI sector, the primary drivers

are the unparalleled sensitivity of financial data and the stringent, global

regulatory compliance mandates (such as GDPR, PCI DSS, and SOX). SSE directly

addresses these by enforcing a Zero Trust model, ensuring that no user or device

is inherently trusted, and providing granular control and visibility over data

access and movement. This is critical for protecting against sophisticated

threats like credential phishing and data exfiltration, which target highly

valuable financial information and customer records.

Simultaneously, the IT & Telecommunications

industry is inherently cloud-native and operates with a highly distributed,

remote, and mobile workforce. These companies are not only securing their own

internal operations but are also often the providers of the infrastructure and

services upon which other businesses rely. SSE solutions offer them a scalable,

high-performance security framework that eliminates the backhauling bottlenecks

of traditional VPNs, providing seamless and secure access to development environments,

cloud platforms, and internal applications from any location. The convergence

of their need to protect intellectual property, manage vast amounts of customer

data, and ensure constant service availability makes the integrated,

cloud-delivered security of SSE not just advantageous but a strategic

imperative for both verticals, solidifying their position as the largest market

shareholders.

The following segments are part of an in-depth analysis of

the global Security Service Edge Market:

|

Market

Segments |

|

|

By

Component |

●

Solutions ●

Services |

|

By

Organisation Size |

●

Large Enterprises ●

Small &

Medium-sized Enterprises (SMEs) |

|

By Vertical |

●

BFSI ●

IT &

Telecommunications ●

Government ●

Healthcare ●

Retail &

E-commerce ●

Manufacturing ●

Others |

Security Service Edge

Market Share Analysis by Region

The North America region is anticipated to hold

the largest portion of the Security Service Edge Market globally throughout the

forecast period.

North America's dominance is attributed to its

mature cybersecurity landscape, high concentration of leading SSE vendors, and

early and widespread adoption of cloud technologies. The region's large base of

enterprises with advanced digital transformation initiatives and a strong

regulatory environment mandating data protection further consolidates

its leading position. High awareness of Zero Trust principles and the need to

secure remote work are key factors driving the market in the U.S. and Canada.

In addition, the Asia-Pacific Security Service

Edge market is poised to be the fastest-growing. This growth is driven by rapid

economic digitalization, a booming SME sector, and increasing government focus

on national cybersecurity. Countries like China, India, Japan, and Australia

are witnessing massive investments in cloud infrastructure and a surge in

hybrid work models. The growing awareness of cyber threats and the need for

scalable, cloud-first security solutions are creating immense opportunities for

SSE providers in this dynamic region.

Security Service Edge

Market Competition Landscape Analysis

The global SSE market is

highly competitive and fragmented, featuring a mix of established cybersecurity

giants, pure-play SSE specialists, and networking vendors expanding into

security. Competition is intense and based on platform comprehensiveness, global

Points of Presence (PoP) coverage, performance, ease of use, and integration

capabilities with broader SASE and XDR ecosystems. Key strategies include

continuous feature innovation (especially in AI/ML and data loss prevention),

strategic acquisitions to fill portfolio gaps, and forming partnerships with

managed security service providers (MSSPs) to extend market reach, particularly

into the mid-market.

Global Security Service

Edge Market Recent Developments News:

- In March 2025, Palo Alto Networks announced the integration of

advanced AI-driven data classification directly into its Prisma SASE

platform, enabling automatic discovery and protection of sensitive data

across all cloud applications.

- In January 2025, Zscaler, Inc. launched a new dedicated SSE solution

tailored for the operational technology (OT) and Internet of Things (IoT)

environments, extending Zero Trust to connected devices.

- In November 2024, Netskope enhanced its NewEdge network with new

global points of presence in Latin America and Southeast Asia, focusing on

improved performance and low-latency access for regional customers.

- In September 2024, Cato Networks introduced a managed SASE service in

partnership with a global telecommunications provider, offering a fully

bundled network and security solution for multinational corporations.

The Global Security

Service Edge Market Is Dominated by a Few Large Companies, such as

●

Palo Alto Networks

(Prisma SASE)

●

Zscaler, Inc.

●

Broadcom (Symantec)

●

Cisco Systems, Inc.

●

Fortinet, Inc.

●

Netskope

●

Proofpoint, Inc.

●

Cato Networks

●

Forcepoint

●

Skyhigh Security

(McAfee Enterprise)

●

iboss

●

Check Point Software

Technologies Ltd.

●

Akamai Technologies

(Linode)

●

Trend Micro

Incorporated

●

Open Systems

●

Lookout, Inc.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Security Service

Edge Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Security Service Edge Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Security Service

Edge Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Component of Global Security

Service Edge Market

1.3.2.Organization Size of

Global Security Service Edge Market

1.3.3.Vertical of Global Security

Service Edge Market

1.3.4.Region of Global Security

Service Edge Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Security Service Edge Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Security Service Edge Market Estimates

& Forecast Trend Analysis, by Component

4.1.

Global

Security Service Edge Market Revenue (US$ Bn) Estimates and Forecasts, by Component,

2020 - 2033

4.1.1.Solutions

4.1.2.Services

5. Global

Security Service Edge Market Estimates

& Forecast Trend Analysis, by Organization Size

5.1.

Global

Security Service Edge Market Revenue (US$ Bn) Estimates and Forecasts, by Organization

Size, 2020 - 2033

5.1.1.Large Enterprises

5.1.2.Small & Medium-sized

Enterprises (SMEs)

6. Global

Security Service Edge Market Estimates

& Forecast Trend Analysis, by Vertical

6.1.

Global

Security Service Edge Market Revenue (US$ Bn) Estimates and Forecasts, by Vertical

2020 - 2033

6.1.1.BFSI

6.1.2.IT &

Telecommunications

6.1.3.Government

6.1.4.Healthcare

6.1.5.Retail & E-commerce

6.1.6.Manufacturing

6.1.7.Others

7. Global

Security Service Edge Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Security Service Edge Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Security

Service Edge Market: Estimates &

Forecast Trend Analysis

8.1. North America Security

Service Edge Market Assessments & Key Findings

8.1.1.North America Security

Service Edge Market Introduction

8.1.2.North America Security

Service Edge Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Component

8.1.2.2.

By Organization Size

8.1.2.3.

By Vertical

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Security

Service Edge Market: Estimates &

Forecast Trend Analysis

9.1. Europe Security Service

Edge Market Assessments & Key Findings

9.1.1.Europe Security Service

Edge Market Introduction

9.1.2.Europe Security Service

Edge Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Component

9.1.2.2.

By Organization Size

9.1.2.3.

By Vertical

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Security

Service Edge Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Security Service Edge Market Introduction

10.1.2.

Asia

Pacific Security Service Edge Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Component

10.1.2.2.

By Organization Size

10.1.2.3.

By Vertical

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Security

Service Edge Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Security Service Edge Market Introduction

11.1.2. Middle

East & Africa

Security Service Edge Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Component

11.1.2.2.

By Organization Size

11.1.2.3.

By Vertical

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Security Service Edge Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Security

Service Edge Market Introduction

12.1.2. Latin America Security

Service Edge Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Component

12.1.2.2.

By Organization Size

12.1.2.3.

By Vertical

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Security Service

Edge Market Product Mapping

14.2. Global Security Service

Edge Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Security Service

Edge Market Tier Structure Analysis

14.4. Global Security Service

Edge Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Palo Alto Networks (Prisma SASE)

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Zscaler, Inc.

15.3.

Broadcom (Symantec)

15.4.

Cisco Systems, Inc.

15.5.

Fortinet, Inc.

15.6.

Netskope

15.7.

Proofpoint, Inc.

15.8.

Cato Networks

15.9.

Forcepoint

15.10.

Skyhigh Security (McAfee Enterprise)

15.11.

iboss

15.12.

Check Point Software Technologies Ltd.

15.13.

Akamai Technologies (Linode)

15.14.

Trend Micro Incorporated

15.15.

Open Systems

15.16.

Lookout, Inc.

15.17.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables