Silicone Elastomers Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (High-temperature Vulcanize (HTV), Room-temperature Vulcanize (RTV), Liquid Silicone Rubber (LSR), By Application (Electrical & Electronics, Automotive & Transportation, Industrial Machinery, Consumer Goods, Construction, Others) and Geography

2025-10-31

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Silicone Elastomers Market Overview

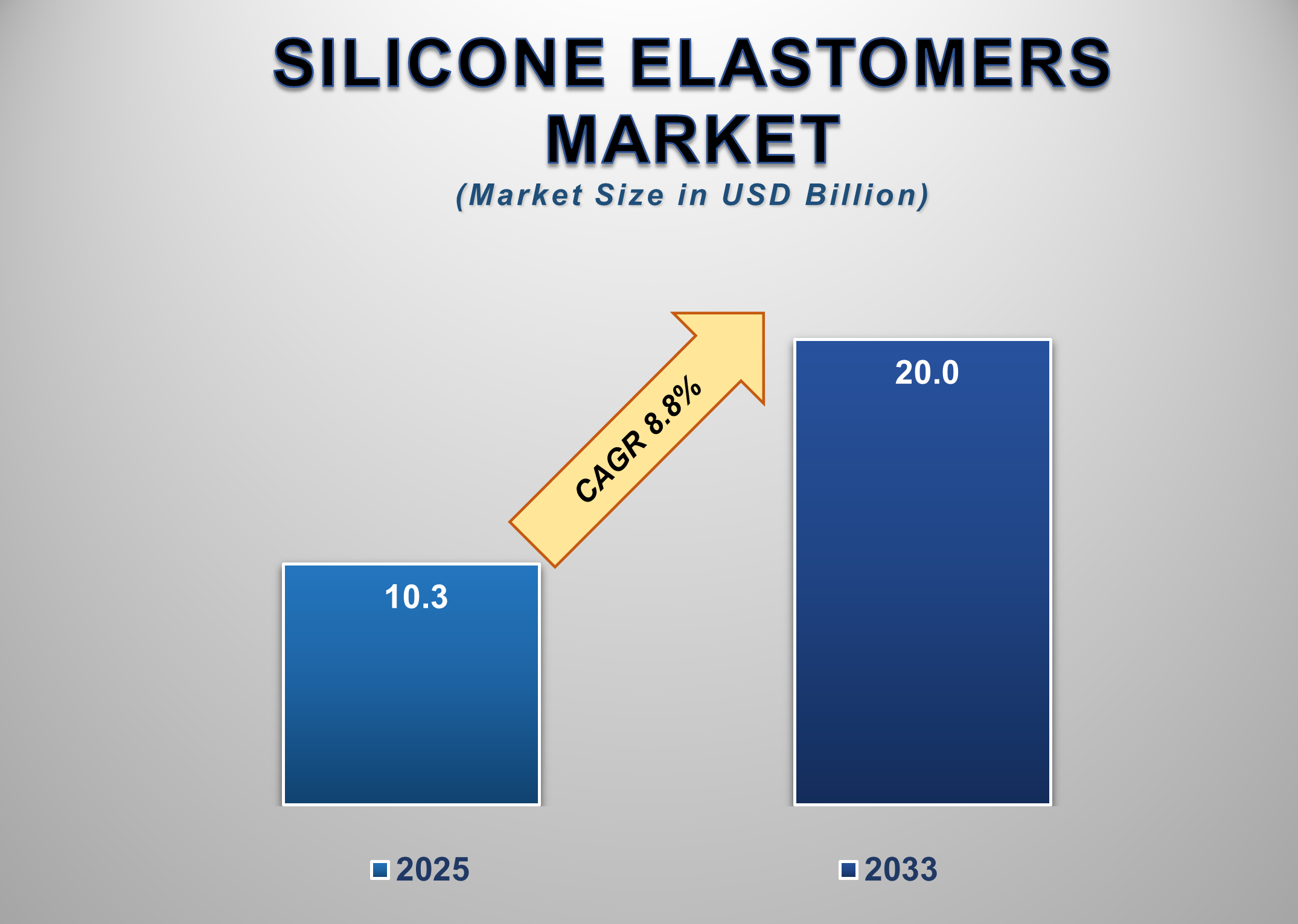

The Global Silicone Elastomers Market Size is projected to grow from USD 10.3 billion in 2025 to USD 20.0 billion by 2033, registering a CAGR of 8.8% during the forecast period. This growth is primarily driven by the expanding use of silicone elastomers across key industries such as automotive, construction, healthcare, electrical & electronics, and consumer goods.

Silicone elastomers are

high-performance synthetic rubbers composed mainly of silicone, known for their

exceptional flexibility, durability, thermal stability, weather resistance, and

biocompatibility. These properties make them ideal for demanding applications

and harsh environmental conditions, fueling global market expansion. In the

healthcare sector, the rising use of medical-grade silicone elastomers for

tubing, implants, catheters, and wearable medical devices is accelerating

demand, particularly with the rapid growth of the medical device industry in

emerging economies.

Silicone Elastomers

Market Drivers and Opportunities

Rising demand from the automotive industry is anticipated to

lift the silicone elastomers market during the forecast period

Automotive is one of the biggest drivers of the

global market for silicone elastomers. With increasing focus on vehicle

performance, safety, and durability, automotive manufacturers are increasingly

using silicone elastomers to take advantage of their high resistance to extreme

temperatures, UV light, and chemical degradation. These materials are

extensively employed in engine gasketing, seals, hoses, connectors, and

vibration-dampening components. Their flexibility and long lifespan are

particularly suitable for under-the-hood applications, particularly in electric

and hybrid vehicles, where thermal management is essential. As the drive

towards light-weighting to achieve aggressive emission standards gains ground,

silicone elastomers provide the benefit of weight savings along with improved

functionality. Moreover, with the increasing production of EVs across the

globe, the demand for high-performance materials that provide resistance to

high voltage and high temperatures is witnessing high growth. EV battery packs,

charging connectors, and cable insulation systems use silicone elastomers. The

trend is set to continue as EVs gain ground in the main markets of the U.S.,

China, and Europe. Moreover, the growth in autonomous vehicle technology and

connected car infrastructure is leading to the incorporation of sensors and

electronics that need to be protected using silicone encapsulation, creating

sustained demand.

Expanding use in the healthcare sector is a vital driver for

influencing the growth of the global silicone elastomers market

Silicone elastomers are quickly finding traction

in the medical and healthcare devices market on the back of their superior

biocompatibility, chemical inertness, and flexibility. These products find

extensive applications in catheters, prosthetics, surgical implements, tubing,

and drug delivery devices. The increasing global population and incidence of

chronic disease are fueling demand for long-term, safe, and flexible medical

components, many of which are manufactured using medical-grade silicone elastomers.

Moreover, the proliferation of wearable monitoring devices is fueling demand

for skin-congenial and breathable materials on the basis of silicone

elastomers. With the global spending on healthcare increasing and innovation in

minimally invasive devices picking up, the demand for

high-performance-elastomer components is becoming increasingly critical.

Silicone elastomers are also critical to life-saving devices such as artificial

heart valves and respiratory devices, and were showcased during the COVID-19

pandemic. Agencies such as the FDA and EMA approve the use of materials made

from silicone on the basis of established safety. Ongoing R&D on

antimicrobial and drug-eluting silicone elastomers is set to find new uses,

positioning the segment as a long-term stimulus for the market.

Innovation in sustainable and bio-based silicone elastomers

is poised to create significant opportunities in the global silicone elastomers

market

With global industries competing

to reduce the environmental footprint of their businesses, there is increasing

potential for the production of bio-based and sustainable silicone elastomers.

Conventional silicones are made from petrochemicals and energy-intensive

materials, which are facing the squeeze of tightening environmental regulations

and greater consumer sensitization. Firms now have the opportunity to achieve a

competitive edge through investment in green chemistry to produce silicone

elastomers from renewable resources or recyclable materials. This is an example

of the increasing trend of circular economy practices and sustainability

reports. Bio-based silicone elastomers can attract the eco-sensitive brands in

consumer products, healthcare, and automotive markets. Moreover, European and

North American governments are pushing the use of low-VOC and non-toxic

materials, towards which the bio-based silicones are well-positioned to meet.

If produced at cost parity to the incumbent materials and with comparable

performance, these materials can provide new markets and differentiation

opportunities. With increasing demand for green alternatives, the space has

huge long-term market potential.

Silicone Elastomers Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 10.3 Billion |

|

Market Forecast in 2033 |

USD 20.0 Billion |

|

CAGR % 2025-2033 |

8.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors, and more |

|

Segments Covered |

●

By Product Type ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19) South Africa |

Silicone Elastomers Market Report Segmentation Analysis

The Global Silicone Elastomers

Market industry analysis is segmented by Product Type, by Application, and by

Region.

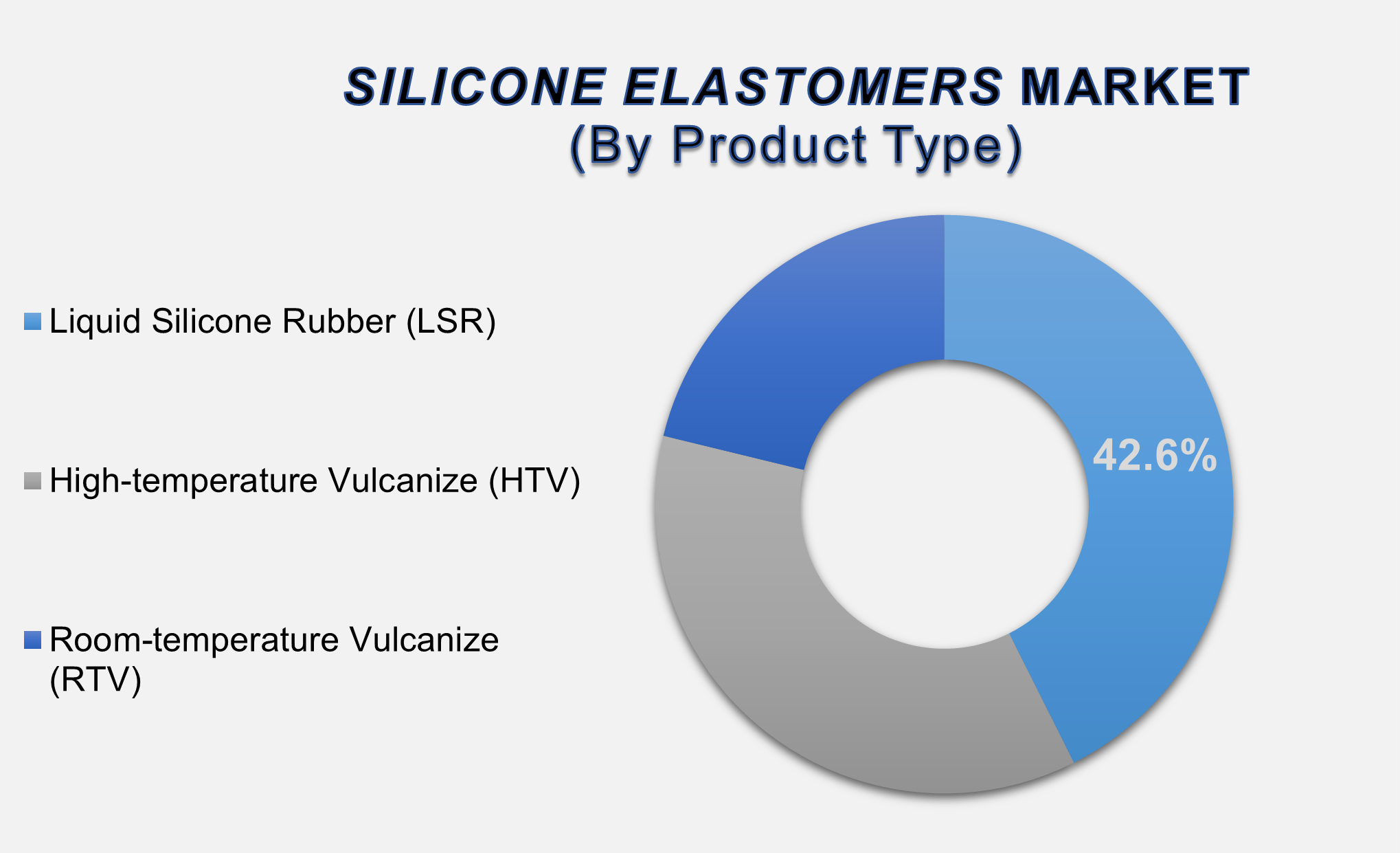

The Liquid Silicone Rubber (LSR) segment is anticipated to

hold the highest share of the global silicone elastomers market during the

projected timeframe

Based on product type, the market

is segmented as High-temperature Vulcanize (HTV), Room-temperature Vulcanize

(RTV), and Liquid Silicone Rubber (LSR). The Liquid Silicone Rubber (LSR)

segment is expected to command the largest share of 42.6% in the global market

for silicone elastomers. The demand for the product is picking up as it offers

better properties like high thermal stability, flexibility, biocompatibility,

and resistance to chemicals, UV, and environmental stress. Its viscosity is

low, and it can be efficiently processed through the use of liquid injection

molding, which makes it suitable for high-volume and precision production. The

market growth for the LSR segment is expected to grow strongly with ongoing

advancements in molding technology and automation, further strengthening it as

the market-leading product type in the industry of silicone elastomers.

The Electrical & Electronics segment is anticipated to

hold the highest share of the market over the forecast period

Based on application, the market

is segmented into Electrical & Electronics, Automotive &

Transportation, Industrial Machinery, Consumer Goods, Construction, and Others.

In 2024, the Electrical & Electronics segment is anticipated to dominate

the global silicone elastomers market over the forecast period. Silicone

elastomers are integral to the electrical industry due to their excellent

insulating properties, thermal stability, and long-term reliability in

challenging environments. They are extensively used for applications such as

cable insulation, circuit board protection, connectors, gaskets, and device

encapsulation. With expanding electronics production and technological

innovation worldwide, this segment is expected to grow consistently and offer

lucrative opportunities for market players.

The following segments are part of an in-depth analysis of the global

silicone elastomers market:

|

Market Segments |

|

|

By Product Type |

●

High-temperature

Vulcanize (HTV) ●

Room-temperature

Vulcanize (RTV) ●

Liquid Silicone

Rubber (LSR) |

|

By Application |

●

Electrical &

Electronics ●

Automotive &

Transportation ●

Industrial Machinery ●

Consumer Goods ●

Construction ●

Others |

Silicone Elastomers

Market Share Analysis by Region

North America is

projected to hold the largest share of the global Silicone Elastomers Market

over the forecast period.

The global silicone elastomers

market exhibits strong regional dynamics, with Asia Pacific emerging as the

dominant region, accounting for an impressive 52.6% market share in 2024. The

growth is largely driven by the fast-paced industrialization, large-scale

manufacturing base, and increasing demand from the leading end-use industries,

including automotive, electronics, construction, and the healthcare sector.

China, Japan, South Korea, and India are leading the growth with the help of

government initiatives to develop infrastructure, technological advances, and

increasing foreign direct investment. The spread of consumer electronics and

the growth of EVs are the key drivers that have widely supported the

consumption of silicone elastomers in products such as insulation, gaskets, and

sensor components. The well-established base of major raw material suppliers

and the leading silicone producers in the Asia Pacific supports smooth supply

chains and cost-effectiveness, which makes the region extremely attractive for

the global players. In addition, the Asia Pacific construction sector is also

poised to grow exponentially, led by population growth, urbanization, and

residential construction activities. These factors are spurring demand for

long-lasting and weather-resistant products, further fueling the growth of the

silicone elastomers market in the Asia Pacific region.

Moreover, the highest CAGR is

expected to be achieved by North America during the forecast period. The growth

is fueled by higher spending on advanced medical devices, intelligent

electronics, and green energy solutions, and higher awareness about

high-performance and eco-friendly materials across various industries.

Silicone Elastomers

Market Competition Landscape Analysis

The Global Silicone Elastomers

Market is marked by robust competition among key players focusing on

innovation, strategic expansion, and sustainability. Continuous research and

development efforts lead to the introduction of advanced Silicone Elastomers

formulations with improved performance characteristics, catering to evolving

industry demands.

Global Silicone

Elastomers Market Recent Developments News:

●

In February 2023,

Momentive Performance Materials Inc., a leading global producer of

high-performance silicones and specialty solutions, unveiled plans for a

significant expansion with a new manufacturing plant in Rayong, Thailand. This

strategic investment will strengthen the company's global supply chain while

supporting regional industrial growth across Southeast Asia.

●

In December 2023, Dow

Inc. unveiled its cutting-edge SILASTIC SA 994X Liquid Silicone Rubber (LSR)

series, a breakthrough material solution specifically engineered for the

healthcare sector. This advanced LSR product line combines exceptional

biocompatibility with superior processability, addressing critical needs in

medical device manufacturing. The new series enables manufacturers to produce

high-precision healthcare components with enhanced efficiency while meeting

stringent medical-grade material requirements.

The Global Silicone

Elastomers Market is dominated by a few

large companies, such as

●

KCC CORPORATION

●

China National

Bluestar Co Ltd.

●

Reiss Manufacturing,

Inc.

●

MESGO S.p.A.

●

AAA Acme Rubber

Co.

●

Bentec Medical OpCo

LLC

●

Rogers

Corporation

●

Elmet

Technologies

●

Cabot Corporation

●

Marsh Bellofram Group

of Companies

●

Akzo Nobel N.V.

●

Saint-Gobain

●

Stockwell

Elastomerics

●

ContiTech AG

●

CHT Germany GmbH

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global

Silicone Elastomers Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Silicone Elastomers

Market Scope and Market Estimation

1.2.1.Global Silicone Elastomers Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Silicone Elastomers

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3. Market Segmentation

1.3.1.Product Type of Global Silicone

Elastomers Market

1.3.2.Application of Global Silicone

Elastomers Market

1.3.3.Region of Global Silicone

Elastomers Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Bn) Analysis

2020 – 2024 and Forecast, 2025 – 2033

2.4. Demand and Opportunity

Assessment

2.5. Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact Analysis of Drivers and

Restraints

2.6. Key Product/Brand Analysis

2.7. Technological Advancements

2.8. Key Developments

2.9. Porter’s Five Forces Analysis

2.9.1.Bargaining Power of Suppliers

2.9.2.Bargaining Power of Buyers

2.9.3.Threat of Substitutes

2.9.4.Threat of New Entrants

2.9.5.Competitive Rivalry

2.10. PEST Analysis

2.10.1. Political Factors

2.10.2. Economic Factors

2.10.3. Social Factors

2.10.4. Technology Factors

2.11. Insights on Cost-effectiveness

of Silicone Elastomers

2.12. Key Regulation

3.

Global Silicone Elastomers

Market Estimates & Historical Trend

Analysis (2020 - 2024)

4.

Global Silicone Elastomers

Market Estimates & Forecast Trend

Analysis, by Product Type

4.1. Global Silicone Elastomers

Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2020 - 2033

4.1.1.High-temperature Vulcanize (HTV)

4.1.2.Room-temperature Vulcanize (RTV)

4.1.3.Liquid Silicone Rubber (LSR)

5.

Global Silicone Elastomers

Market Estimates & Forecast Trend

Analysis, by Application

5.1. Global Silicone Elastomers

Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

5.1.1.Electrical & Electronics

5.1.2.Automotive & Transportation

5.1.3.Industrial Machinery

5.1.4.Consumer Goods

5.1.5.Construction

5.1.6.Others

6.

Global Silicone Elastomers

Market Estimates & Forecast Trend

Analysis, by Region

6.1. Global Silicone Elastomers

Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7.

North

America Silicone Elastomers Market: Estimates & Forecast Trend Analysis

7.1.

North

America Silicone Elastomers Market Assessments & Key Findings

7.1.1.North America Silicone

Elastomers Market Introduction

7.1.2.North America Silicone

Elastomers Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Product Type

7.1.2.2. By Application

7.1.2.3. By Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8.

Europe

Silicone Elastomers Market: Estimates & Forecast Trend Analysis

8.1. Europe Silicone Elastomers

Market Assessments & Key Findings

8.1.1.Europe Silicone Elastomers

Market Introduction

8.1.2.Europe Silicone Elastomers

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product Type

8.1.2.2. By Application

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6. Rest

of Europe

9.

Asia

Pacific Silicone Elastomers Market: Estimates & Forecast Trend Analysis

9.1. Asia Pacific Market Assessments

& Key Findings

9.1.1.Asia Pacific Silicone Elastomers

Market Introduction

9.1.2.Asia Pacific Silicone Elastomers

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product Type

9.1.2.2. By Application

9.1.2.3.

By

Country

9.1.2.3.1. China

9.1.2.3.2. Japan

9.1.2.3.3. India

9.1.2.3.4. Australia

9.1.2.3.5. South Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Silicone

Elastomers Market: Estimates &

Forecast Trend Analysis

10.1. Middle East & Africa Market

Assessments & Key Findings

10.1.1. Middle

East & Africa Silicone

Elastomers Market Introduction

10.1.2. Middle

East & Africa Silicone

Elastomers Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product Type

10.1.2.2. By Application

10.1.2.3. By Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest of

MEA

11. Latin America

Silicone Elastomers Market: Estimates

& Forecast Trend Analysis

11.1. Latin America Market Assessments

& Key Findings

11.1.1. Latin America Silicone

Elastomers Market Introduction

11.1.2. Latin America Silicone

Elastomers Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product Type

11.1.2.2. By Application

11.1.2.3. By Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest of

LATAM

12. Country Wise Market:

Introduction

13. Competition Landscape

13.1. Global Silicone Elastomers

Market Product Mapping

13.2. Global Silicone Elastomers

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

13.3. Global Silicone Elastomers

Market Tier Structure Analysis

13.4. Global Silicone Elastomers

Market Concentration & Company Market Shares (%) Analysis, 2024

14. Company Profiles

14.1.

KCC CORPORATION

14.1.1. Company Overview & Key Stats

14.1.2. Financial Performance & KPIs

14.1.3. Product Portfolio

14.1.4. SWOT Analysis

14.1.5. Business Strategy & Recent

Developments

* Similar details would be provided

for all the players mentioned below

14.2. China National

Bluestar Co Ltd.

14.3. Reiss

Manufacturing, Inc.

14.4. MESGO

S.p.A.

14.5. AAA Acme

Rubber Co.

14.6. Bentec Medical

OpCo LLC

14.7. Rogers

Corporation

14.8. Elmet

Technologies

14.9. Cabot

Corporation

14.10. Marsh

Bellofram Group of Companies

14.11. Akzo Nobel

N.V.

14.12. Saint-Gobain

14.13. Stockwell

Elastomerics

14.14. ContiTech

AG

14.15. CHT Germany

GmbH

14.16. Others

15. Research

Methodology

15.1. External Transportations /

Databases

15.2. Internal Proprietary Database

15.3. Primary Research

15.4. Secondary Research

15.5. Assumptions

15.6. Limitations

15.7. Report FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables