Smart Hospitality Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component: (Software and Services); By Deployment (Cloud-Based and On-Premise); By Hotel Type (Business Hotels, Heritage and Boutique Hotels, Resorts and Spas, Luxury Hotels, Cruises, Luxury Yachts and Others) and Geography

2025-11-03

ICT

Ekta Chaurasia (Team Lead)

Description

Smart Hospitality Market Overview

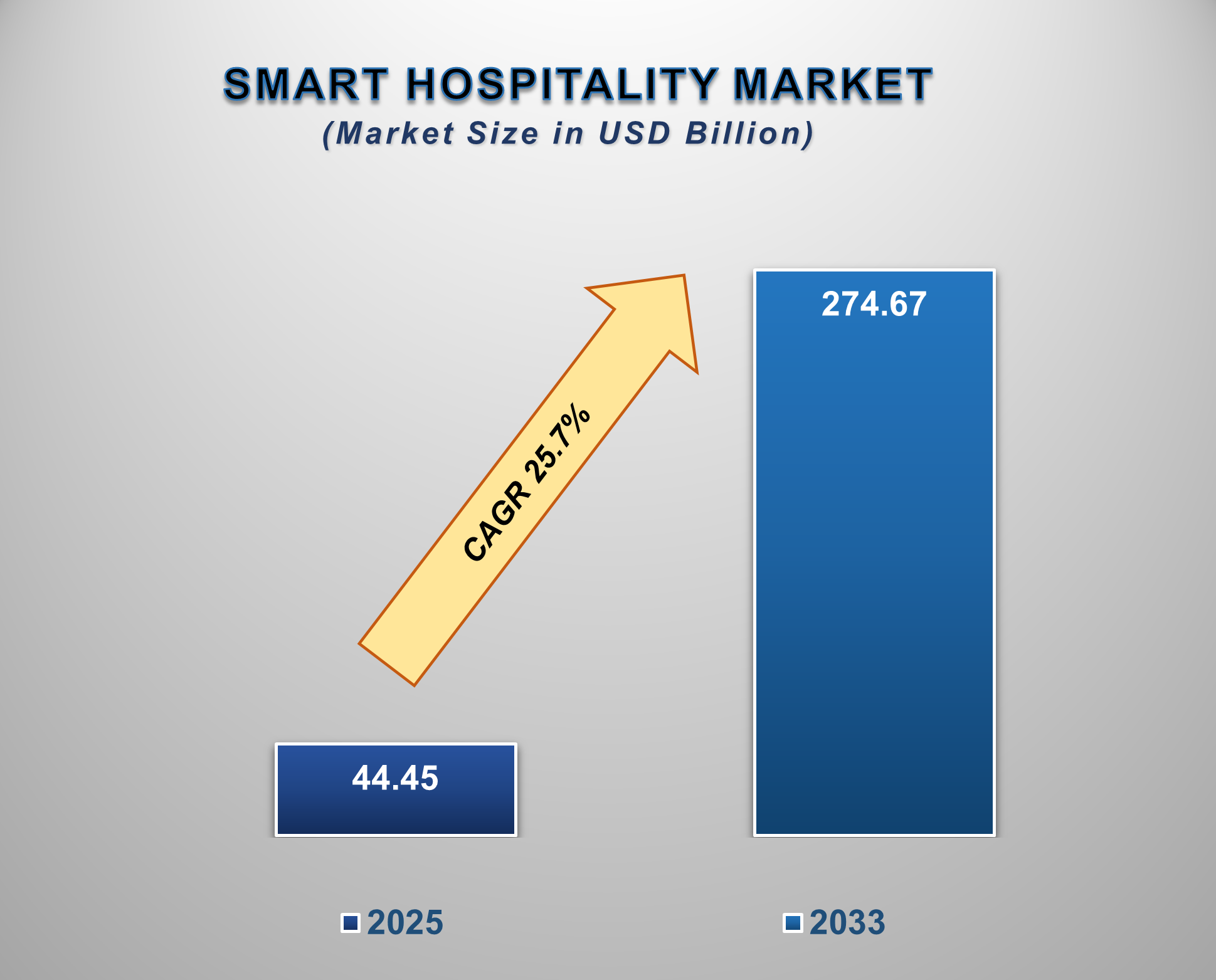

The Global Smart Hospitality Market is undergoing a significant transformation, driven by the integration of advanced technologies to enhance guest experience, optimize operational efficiency, and meet the rising demand for personalized and contactless services. Valued at USD 44.45 billion in 2025, the market is projected to reach USD 274.67 billion by 2033, growing at a CAGR of 25.7% during the forecast period.

The Global Smart Hospitality

Market refers to the market encompassing advanced technology solutions and

services designed to enhance the operations, management, and guest experiences

within the hospitality industry. The Global Smart Hospitality Market is all

about leveraging digital, automated, and IoT-enabled solutions to modernize the

hospitality sector and deliver superior guest experiences. The Global Smart

Hospitality Market is a rapidly evolving sector leveraging advanced

technologies to enhance guest experiences, optimize operations, and improve

efficiency within the hospitality industry. The global smart hospitality market

is experiencing rapid growth, driven by advancements in technology and evolving

consumer expectations.

Smart Hospitality Market

Drivers and Opportunities

Demand for Personalized Guest Experiences is anticipated to

lift the Smart Hospitality market growth during the forecast period

The demand for personalized guest

experiences is a significant driver of the global smart hospitality market,

influencing its rapid growth and technological advancements. Personalization in

hospitality involves tailoring services and amenities to individual guest

preferences, enhancing satisfaction and loyalty. This trend is propelled by

advancements in Internet of Things (IoT) technologies, artificial intelligence

(AI), and data analytics, enabling hotels to offer customized experiences that

meet the evolving expectations of modern travelers. Hotels are leveraging data

analytics and AI to understand guest preferences and behaviors, allowing them

to offer personalized services such as customized room settings, tailored

recommendations for dining and activities, and personalized communication.

Furthermore, the integration of smart technologies enables hotels to streamline

operations and improve efficiency, which contributes to cost savings and

enhanced service delivery. As guests increasingly expect personalized and

seamless experiences, the adoption of smart hospitality solutions is becoming

essential for hotels aiming to stay competitive in the market.

Adoption of Contactless and Mobile-First Solutions is a vital

driver for influencing the growth of the global Smart Hospitality market

The

pervasive adoption of contactless and mobile-first solutions is a primary

catalyst driving the lucrative growth of the Global Smart Hospitality Market,

as these technologies directly address modern guest demands for convenience,

efficiency, and safety while simultaneously optimizing hotel operations. This

movement encompasses everything from mobile check-in/out and digital key

delivery to in-app service requests and QR code-based ordering, all of which

streamline the guest journey. A key statistical driver is the sheer reliance on

mobile devices for travel: currently, more than a third of hotel bookings are

made on mobile, a figure that dramatically jumps to 80% for last-minute

bookings, compelling hoteliers to adopt a mobile-first strategy. Major chains

have validated this approach with tangible results; for instance, Hilton's

Digital Key program has been used for over 150 million room entries globally,

reducing check-in time by an average of seven minutes per guest while

maintaining high satisfaction. By automating front-desk tasks, hotels can

reallocate staff to value-adding concierge services, and the digital nature of

these interactions provides vast amounts of data for hyper-personalization,

which, in turn, boosts guest satisfaction scores by as much as 25% within six

months of implementation, establishing a powerful feedback loop for market

expansion.

Integration of Artificial Intelligence (AI) and Internet of

Things (IoT) is poised to create significant opportunities in the global Smart

Hospitality market

The convergence of Artificial

Intelligence (AI) and the Internet of Things (IoT) is set to generate a

profoundly lucrative opportunity for the Global Smart Antenna Market, primarily

by driving demand for advanced, self-optimizing wireless communication systems,

particularly with the global rollout of 5G networks. This integration elevates

smart antennas from passive components to intelligent network assets capable of

real-time, dynamic performance adjustment. For example, the need to support the

massive projected growth of connected devices, with forecasts suggesting the

number of global IoT devices could exceed 75 billion by 2025, directly propels

the smart antenna market. AI-powered smart antennas use machine learning to

execute real-time beamforming optimization, directing radio frequency (RF)

energy precisely to individual IoT devices (like sensors in a smart city or

components in an autonomous vehicle), minimizing interference, and maximizing

spectral efficiency. This intelligence is crucial for complex, high-demand

scenarios like vehicle-to-everything (V2X) communication, where continuous,

low-latency connectivity is non-negotiable. Furthermore, AI enables Predictive

Network Management, allowing antennas to anticipate traffic patterns and

interference sources across large IoT networks, thus proactively adjusting

antenna behavior to prevent connectivity issues. This symbiotic relationship

between AI, the data-generating IoT, and the enhanced capabilities of smart

antennas creates a foundation for highly efficient, reliable, and

energy-conscious wireless infrastructure, cementing their vital role in

next-generation applications.

Smart Hospitality Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 44.45 Billion |

|

Market Forecast in 2033 |

USD 274.67 Billion |

|

CAGR % 2025-2033 |

25.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Service Type, Growth Factors and more |

|

Segments Covered |

●

By Component ●

By Deployment ●

By Hotel Type |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Smart Hospitality Market Report Segmentation Analysis

The global Smart Hospitality

Market industry analysis is segmented by Component, Deployment, Hotel Type, and

Region.

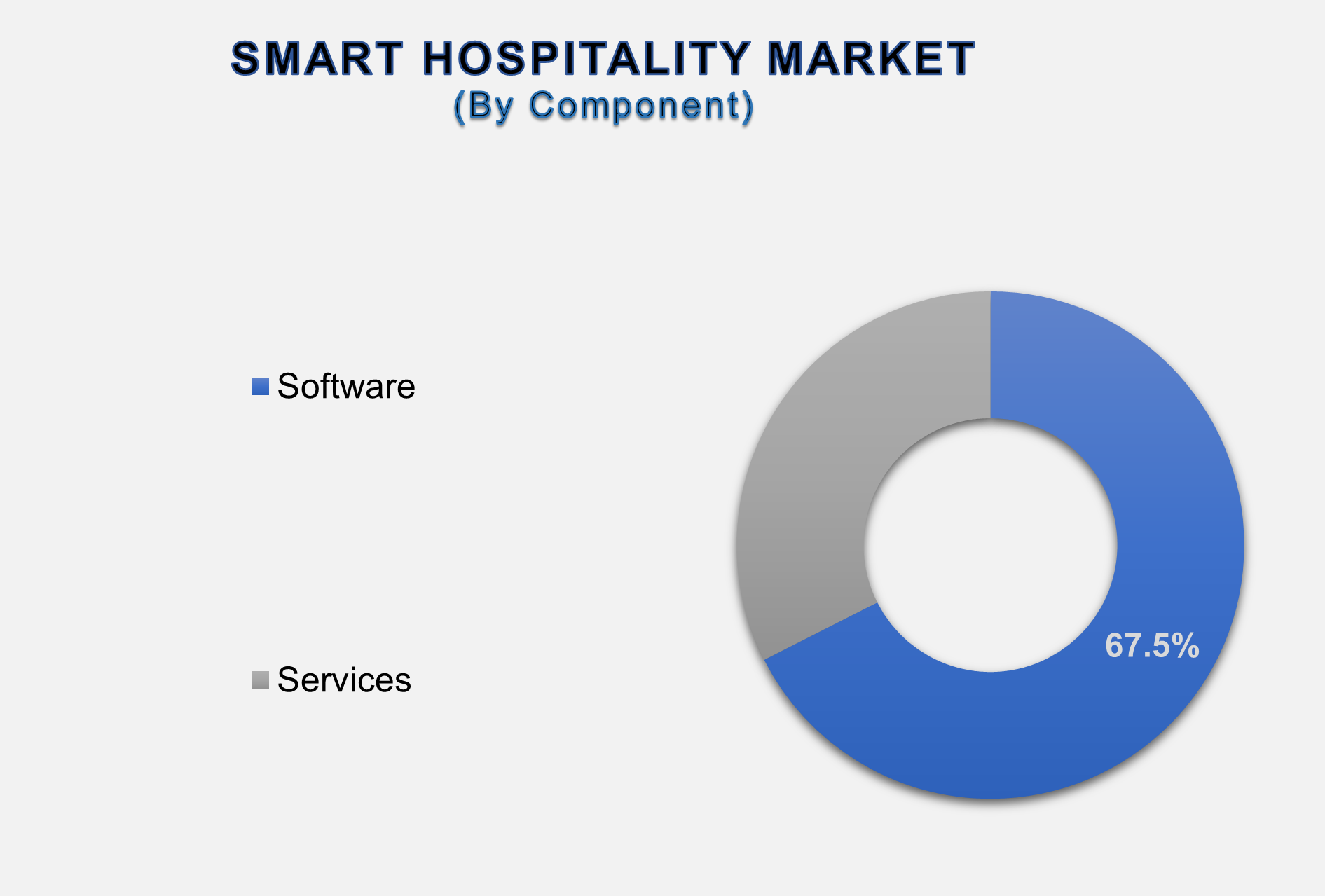

Software Dominates the Component Segment

By Component, the Smart Hospitality market is segmented into Software (Property Management System (PMS), Guest Experience Management System, Integrated Security Management, Facility Management Software/Hotel Building Automation System (HBAS), Network Management Software, Point of Sale (POS) Software, Hotel Operation Management, Revenue Management, Room Automation and Control System and Others) and Services (Professional and Managed). The software component holds the largest market share of the total revenue in 2024. This dominance is attributed to the widespread adoption of hotel management software, including property management systems (PMS), guest experience management tools, and integrated security systems, which enhance operational efficiency and guest satisfaction.

Cloud holds the highest share of the Deployment Segment

On the basis of Deployment, the

market is bifurcated into Cloud-Based and On-Premise. The cloud-based segment

holds a dominant position in the market, driven by its flexibility,

scalability, and cost-effectiveness. Cloud solutions enable remote access, real-time

updates, and integration with Internet of Things (IoT) and Artificial

Intelligence (AI) technologies, enhancing operational agility and guest

experience. The cloud segment is expected to continue its robust growth

trajectory, driven by the increasing integration of IoT, AI, and cloud-based

solutions within the hospitality industry. These technologies enable

personalized guest experiences, streamlined operations, and improved energy

efficiency.

Business Hotel Segment Leads by Hotel Type

In terms of Hotel Type, the Smart

Hospitality market is segmented into Business Hotels, Heritage and Boutique

Hotels, Resorts and Spas, Luxury Hotels, Cruises, Luxury Yachts, and Others.

Business Hotels establishments cater primarily to business travelers and are

the largest adopters of smart hospitality solutions. The integration of

technologies such as mobile check-ins, automated room controls, and data

analytics enhances operational efficiency and meets the high expectations of

corporate clients.

The following segments are part of an

in-depth analysis of the global Smart Hospitality Market:

|

Market Segments |

|

|

By Component

|

●

Software o

Property Management

System (PMS) o

Guest Experience

Management System o

Integrated Security

Management o

Facility Management

Software/Hotel Building Automation System (HBAS) o

Network Management

Software o

Point of Sale (POS)

Software o

Hotel Operation

Management o

Revenue Management o

Room Automation and

Control System o

Others ●

Services o

Professional o

Managed |

|

By Deployment

|

●

Cloud-Based ●

On-Premise |

|

By Hotel Type |

●

Business Hotels ●

Heritage and

Boutique Hotels ●

Resorts and Spas ●

Luxury Hotels ●

Cruises ●

Luxury Yachts ●

Others |

Smart Hospitality Market

Share Analysis by Region

The Europe region is projected to hold the largest share of

the global Smart Hospitality Market over the forecast period.

Europe holds the largest share of

the global smart hospitality market, accounting for approximately 33.5%. This

dominance is driven by technological advancements, a well-established digital

infrastructure, and a strong emphasis on enhancing customer experiences through

smart room solutions, energy efficiency, and AI-driven personalization.

Countries like the United Kingdom are leading the way in integrating smart

technologies into hospitality operations. Furthermore, the Asia Pacific region

is poised to experience the highest growth rate in the smart hospitality

market. This growth is driven by rapid urbanization, increasing disposable

incomes, and a burgeoning middle class, leading to higher demand for modern and

tech-enabled hospitality services. Countries like China, India, and Japan are

at the forefront of this expansion, with significant investments in smart hotel

projects and infrastructure development. For instance, India recorded a new

high with 693 hotel projects comprising 88,884 rooms under development during

the January-March 2025 quarter, marking a 19% increase in projects and a 27%

rise in rooms year-on-year.

Global Smart Hospitality

Market Recent Developments News:

- In September

2025, Marriott International expanded its footprint in India through a

partnership with CG Hospitality, launching a new midscale and

upscale-focused brand, Series by Marriott. This collaboration integrates

84 operational Fern Hotels, approximately 6,000 rooms, into Marriott’s

portfolio, supporting rapid growth in the midscale and upscale categories.

- In August 2025, Nightfood Holdings is strategically building an $80 million

portfolio of high-quality hotel assets through a series of acquisitions.

The company is leveraging AI and robotics to enhance service efficiency

and address labor shortages, reflecting the industry's shift towards

automation and smart technologies.

- In December 2024, Pyramid

Global Hospitality's European division, Hamilton Pyramid Europe, merged

with London-based Axiom Hospitality. This merger aims to strengthen their

market position in Europe, combining resources and expertise to offer

enhanced services in the smart hospitality sector.

The Global Smart

Hospitality Market is dominated by a few large companies, such as

●

Honeywell

International Inc.

●

IBM Corporation

●

Cisco Systems, Inc.

●

Oracle Corporation

●

Siemens AG

●

Samsung Electronics

Co., Ltd.

●

Intel Corporation

●

Microsoft Corporation

●

LG Electronics Inc.

●

Schneider Electric SE

●

Johnson Controls

International plc

●

ASSA ABLOY AB

●

Panasonic Corporation

●

Hitachi, Ltd.

●

Zebra Technologies

Corporation

●

Agilysys, Inc.

●

Sabre Corporation

●

Amadeus IT Group

●

NEC Corporation

●

Allegion PLC

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Smart Hospitality Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Smart Hospitality Market Scope and Market Estimation

1.2.1.Global Smart

Hospitality Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global Smart

Hospitality Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Component of

Global Smart Hospitality Market

1.3.2.Deployment of

Global Smart Hospitality Market

1.3.3.Hotel Type of

Global Smart Hospitality Market

1.3.4.Region of

Global Smart Hospitality Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Demand Supply Scenario

2.6.

Market Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact

Analysis of Drivers and Restraints

2.7.

Emerging Trends for Smart Hospitality Market

2.8.

Porter’s Five Forces Analysis

2.9.

PEST Analysis

2.10. Key

Regulation

3.

Global

Smart Hospitality Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Smart Hospitality Market Estimates & Forecast Trend Analysis, by Component

4.1.

Global Smart Hospitality Market Revenue (US$ Bn) Estimates and

Forecasts, by Component, 2020 - 2033

4.1.1.Software

4.1.1.1.

Property Management System (PMS)

4.1.1.2.

Guest Experience Management System

4.1.1.3.

Integrated Security Management

4.1.1.4.

Facility Management Software/Hotel Building Automation System

(HBAS)

4.1.1.5.

Network Management Software

4.1.1.6.

Point of Sale (POS) Software

4.1.1.7.

Hotel Operation Management

4.1.1.8.

Revenue Management

4.1.1.9.

Room Automation and Control System

4.1.1.10.

Others

4.1.2.Services

4.1.2.1.

Professional

4.1.2.2.

Managed

5. Global Smart Hospitality Market Estimates & Forecast Trend Analysis, by Deployment

5.1.

Global Smart Hospitality Market Revenue (US$ Bn) Estimates and

Forecasts, by Deployment, 2020 - 2033

5.1.1.Cloud-Based

5.1.2.On-Premise

6. Global Smart Hospitality Market Estimates & Forecast Trend Analysis, by Hotel Type

6.1.

Global Smart Hospitality Market Revenue (US$ Bn) Estimates and

Forecasts, by Hotel Type, 2020 - 2033

6.1.1.Business

Hotels

6.1.2.Heritage and

Boutique Hotels

6.1.3.Resorts and

Spas

6.1.4.Luxury Hotels

6.1.5.Cruises

6.1.6.Luxury Yachts

6.1.7.Others

7.

Global

Smart Hospitality Market Estimates & Forecast Trend Analysis, by Region

1.1.

Global Smart Hospitality Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East

& Africa

1.1.5.Latin America

8.

North America Smart

Hospitality Market: Estimates &

Forecast Trend Analysis

8.1.

North America Smart Hospitality Market Assessments & Key

Findings

8.1.1.North America

Smart Hospitality Market Introduction

8.1.2.North America

Smart Hospitality Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Component

8.1.2.2.

By Deployment

8.1.2.3.

By Hotel Type

8.1.2.4.

By Country

8.1.2.4.1.

The U.S.

8.1.2.4.2.

Canada

9.

Europe Smart

Hospitality Market: Estimates &

Forecast Trend Analysis

9.1.

Europe Smart Hospitality Market Assessments & Key Findings

9.1.1.Europe Smart

Hospitality Market Introduction

9.1.2.Europe Smart

Hospitality Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Component

9.1.2.2.

By Deployment

9.1.2.3.

By Hotel Type

9.1.2.4.

By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Netherland

9.1.2.4.7.

Rest

of Europe

10.

Asia Pacific Smart

Hospitality Market: Estimates &

Forecast Trend Analysis

10.1. Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia Pacific Smart Hospitality Market Introduction

10.1.2.

Asia Pacific Smart Hospitality Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

10.1.2.1.

By Component

10.1.2.2.

By Deployment

10.1.2.3.

By Hotel Type

10.1.2.4.

By Country

10.1.2.4.1.

China

10.1.2.4.2.

Japan

10.1.2.4.3.

India

10.1.2.4.4.

Australia

10.1.2.4.5.

South Korea

10.1.2.4.6. Rest

of Asia Pacific

11.

Middle East & Africa Smart Hospitality Market:

Estimates & Forecast Trend Analysis

11.1. Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Smart

Hospitality Market Introduction

11.1.2.

Middle East & Africa Smart

Hospitality Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Component

11.1.2.2.

By Deployment

11.1.2.3.

By Hotel Type

11.1.2.4.

By Country

11.1.2.4.1.

UAE

11.1.2.4.2.

Saudi Arabia

11.1.2.4.3.

South Africa

11.1.2.4.4. Rest of MEA

12.

Latin America Smart

Hospitality Market: Estimates &

Forecast Trend Analysis

12.1. Latin

America Market Assessments & Key Findings

12.1.1.

Latin America Smart Hospitality Market Introduction

12.1.2.

Latin America Smart Hospitality Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

12.1.2.1.

By Component

12.1.2.2.

By Deployment

12.1.2.3.

By Hotel Type

12.1.2.4.

By Country

12.1.2.4.1.

Brazil

12.1.2.4.2.

Mexico

12.1.2.4.3.

Argentina

12.1.2.4.4. Rest of LATAM

13.

Country Wise Market: Introduction

14. Competition

Landscape

14.1. Global

Smart Hospitality Market Product Mapping

14.2. Global

Smart Hospitality Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3. Global

Smart Hospitality Market Tier Structure Analysis

14.4. Global

Smart Hospitality Market Concentration & Company Market Shares (%)

Analysis, 2024

15. Company

Profiles

15.1. Honeywell International Inc.

15.1.1.

Company Overview & Key Stats

15.1.2.

Financial Performance & KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2.

IBM Corporation

15.3.

Cisco Systems, Inc.

15.4.

Oracle Corporation

15.5.

Siemens AG

15.6.

Samsung Electronics Co., Ltd.

15.7.

Intel Corporation

15.8.

Microsoft Corporation

15.9.

LG Electronics Inc.

15.10.

Schneider Electric SE

15.11.

Johnson Controls International plc

15.12.

ASSA ABLOY AB

15.13.

Panasonic Corporation

15.14.

Hitachi, Ltd.

15.15.

Zebra Technologies Corporation

15.16.

Agilysys, Inc.

15.17.

Sabre Corporation

15.18.

Amadeus IT Group

15.19.

NEC Corporation

15.20.

Allegion PLC

15.21.

Other Prominent Players

16.

Research

Methodology

16.1. External

Transportations / Databases

16.2. Internal

Proprietary Database

16.3. Primary

Research

16.4. Secondary

Research

16.5. Assumptions

16.6. Limitations

16.7. Report

FAQs

17.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables