Global Smart TV Market Size and Forecast (2025 – 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Operating System (Android TV, Tizen, WebOS, Roku, Others), By Resolution (4K UHD TV, HDTV, Full HD TV, 8K TV), By Screen Size (Below 32 inches, 32 to 45 inches, 46 to 55 inches, 56 to 65 inches, Above 65 inches), By Technology (OLED, QLED, LED, Others), By Distribution Channel (Online, Offline), and Geography

2025-11-26

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Smart TV Market Overview

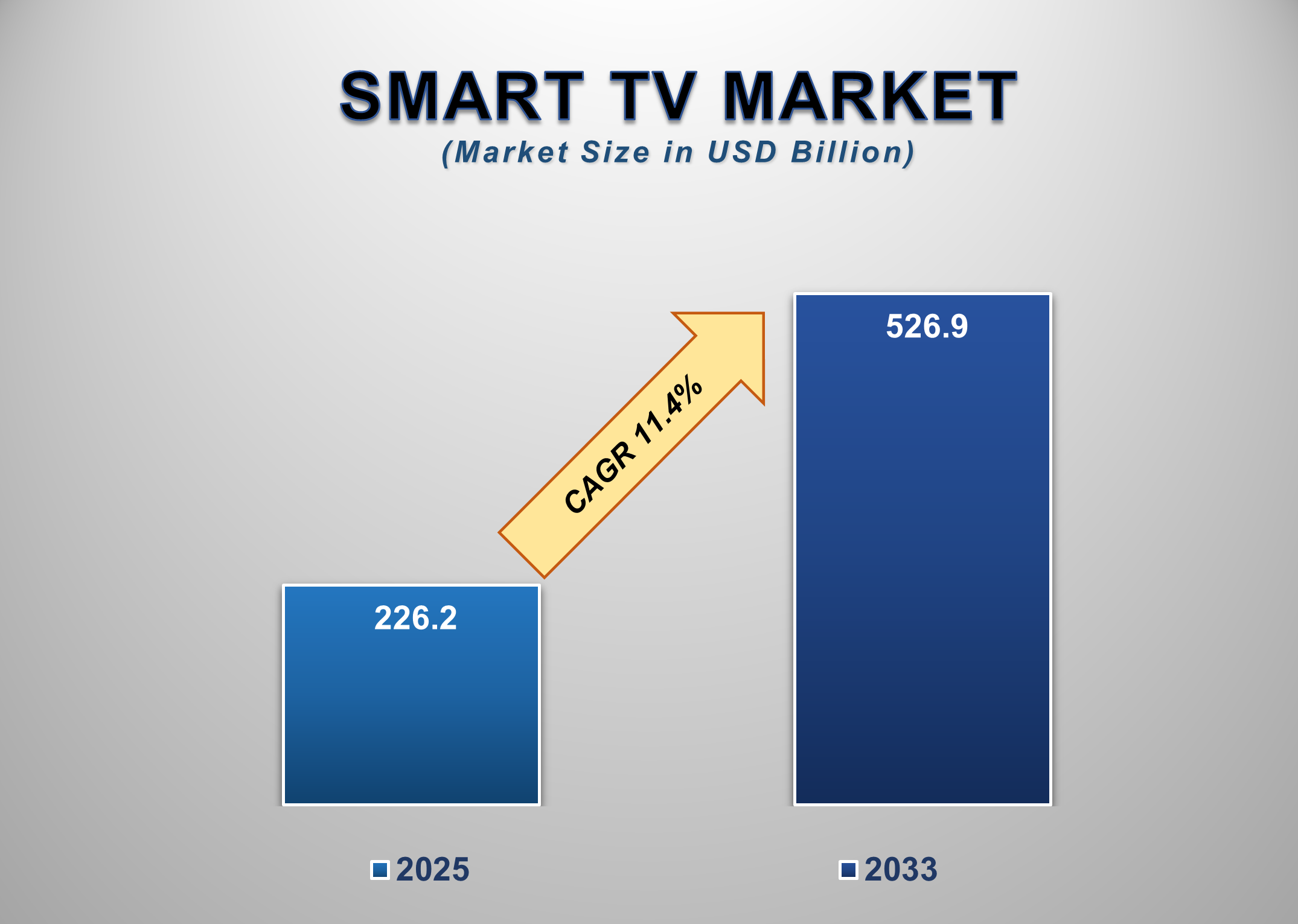

The Global Smart TV Market is projected to reach US$526.9 billion by 2033 from an estimated US$226.2 billion in 2025, growing at a CAGR of 11.4% during 2025–2033. The market is witnessing rapid expansion driven by evolving consumer preferences for connected entertainment systems, advancements in display technology, and growing internet penetration worldwide. Smart TVs, embedded with advanced operating systems, allow users to access a vast range of content, from streaming services and games to web browsing, directly from their television sets.

A rising appetite for 4K and 8K

displays, coupled with AI-integrated voice assistance and smart home

connectivity, is boosting adoption across both developed and emerging

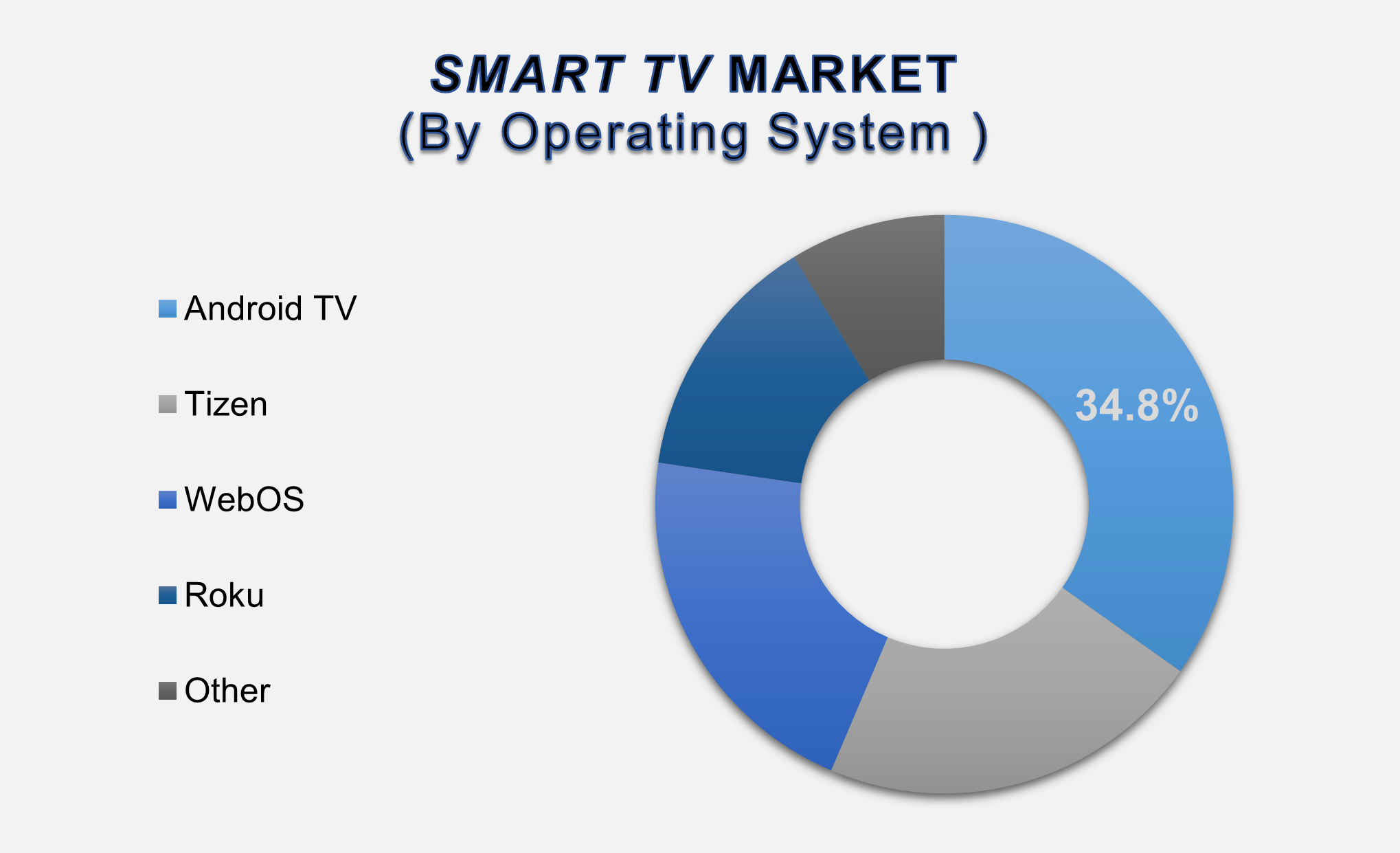

economies. Notably, Android TV leads the market with a 34.8% share due to its

flexible ecosystem and wide developer support. Meanwhile, the proliferation of

OTT platforms and reduced costs of high-resolution panels are broadening

accessibility to high-end smart TVs. Consumers are increasingly switching from

conventional televisions to smart variants, fueling intensified competition

among global manufacturers.

Smart TV Market Drivers

and Opportunities

Rising

Internet Penetration and OTT Adoption are Driving the Smart TV Market Growth

The rapid global adoption of high-speed internet services has been

a vital catalyst for the expansion of the smart TV market. With the growing

accessibility of broadband and 4G/5G mobile networks, consumers now enjoy

seamless connectivity that supports HD and 4K content streaming via popular OTT

(over-the-top) platforms. Streaming giants such as Netflix, Hulu, and Amazon

Prime Video have revolutionized media consumption by shifting audiences from

traditional broadcast models to direct-to-consumer digital platforms. This

transformation is further fueled by the rising availability of affordable data

plans and the proliferation of smart devices. As user engagement with OTT

content surges, smart TVs are becoming the preferred medium for home

entertainment, owing to their ability to provide immersive audiovisual

experiences. Moreover, young consumers increasingly favor smart TVs for their

capability to integrate social media, gaming, and music applications alongside

mainstream video streaming. Government initiatives supporting digital

infrastructure growth in emerging economies, coupled with the competitive

pricing strategies of smart TV manufacturers, have enhanced market penetration

among middle-income households. This shift in consumer behavior from passive TV

viewing to interactive content streaming is poised to significantly drive smart

TV demand during the projected period.

Technological Innovations in Display and Connectivity Are

Accelerating Smart TV Adoption

The evolution of smart TV technology has been marked by rapid

advancements in display resolution, processing power, and user-friendly

interfaces. Manufacturers are consistently improving TV panels through

technologies such as OLED, QLED, MicroLED, and Mini-LED, which offer enhanced

brightness, deep black levels, wider color gamut, and exceptional viewing

angles. Meanwhile, the integration of AI-powered features such as upscaling to

8K, adaptive contrast control, and voice-command navigation significantly elevates

the viewing experience. Moreover, the incorporation of smart home connectivity

protocols like Google Assistant, Alexa, and Apple HomeKit, along with support

for Wi-Fi 6 and Bluetooth 5.0, enables smooth multi-device communication and

home ecosystem integration. The rising adoption of cloud gaming, virtual

reality experiences, and home fitness applications has expanded the utility of

smart TVs beyond entertainment. Advanced audio technologies, including Dolby

Atmos and DTS:X, have created cinema-like audio experiences, encouraging

consumers to upgrade to premium smart TV models. These innovations not only

enhance the aesthetic appeal and technical capabilities of smart TVs but also

make them central to connected living spaces. As manufacturers continue to

differentiate through innovations in design, display sophistication, and

integrated software ecosystems, the smart TV market is expected to witness

significant growth momentum.

Emerging Economies' Growth of Smart TV Is Poised to Create

Significant Opportunities in the Smart TV Market Worldwide

Rapid urbanization, rising disposable incomes, and the expansion

of consumer electronics distribution networks in emerging economies present

promising opportunities for smart TV manufacturers. Countries across the Asia

Pacific, Latin America, and Africa are experiencing increased household

penetration of advanced digital devices, fueled by economic development and

government-backed digitalization programs. The advent of local and regional

content platforms, as well as language-specific streaming services, is further

cultivating the demand for smart TVs among previously underserved populations.

Affordable financing options, EMI schemes, and promotional discounts offered

through online retail channels have made larger screen sizes and

higher-resolution smart TVs financially accessible to a broader demographic.

Consumer preferences in high-potential markets such as India, Indonesia,

Brazil, and Nigeria are shifting away from conventional TV sets toward smart

TVs that can support online education, telehealth, and social entertainment.

Additionally, the rise of domestic smart TV manufacturers, alongside strategic

partnerships with telecom operators offering bundled broadband services, is

reshaping the competitive landscape in these regions. With OEMs focusing on customized

regional content, energy-efficient models, and modular software upgrades, the

smart TV market in emerging economies is positioned for strong future growth.

These untapped markets not only offer significant sales potential but also

provide opportunities for smart TV brands to establish long-term loyalty among

newly connected users.

Smart TV Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 226.2 Billion |

|

Market Forecast in 2033 |

USD 526.9 Billion |

|

CAGR % 2025-2033 |

11.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Operating

System ●

By Resolution ●

By Screen Size ●

BY Technology ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Smart TV Market Report

Segmentation Analysis

The global Smart TV Market is

segmented into Operating System, Resolution, Screen Size, Technology,

Distribution Channel, and Geography.

The

Android TV Segment Accounted for the Largest Market

Share in the Global Smart TV Market

By Operating System, the market is segmented into Android TV, Tizen, WebOS, Roku, and Others. The Android TV segment dominates the global market, accounting for the largest share in 2025. This dominance is attributed to Android’s open-source architecture, which enables TV manufacturers to integrate customizable software environments with extensive app compatibility. Android TVs offer seamless access to the Google Play Store, allowing users to download hundreds of apps, games, and streaming platforms. The OEM flexibility, support for Chromecast built-in, and regular software updates reinforce Android TV’s leadership. The widespread use of Android in smartphones further enhances consumer familiarity and ease of use, leading to broader adoption, especially in the Asia Pacific and Latin America.

4K

UHD TV Segment Led the Global Smart TV Market by Resolution in 2025

By resolution, the Smart TV Market is classified into 4K UHD TV, HDTV,

Full HD TV, 8K TV, and Others. The 4K UHD TV segment held the largest market

share in 2025, driven by a combination of decreasing price points and

increasing availability of 4K content across OTT platforms. The

ultra-high-definition resolution offers exceptional clarity and depth,

appealing to consumers seeking immersive visual experiences. Content providers

such as Netflix, Amazon Prime, and YouTube have significantly expanded their 4K

libraries, encouraging users to adopt 4K smart TVs. Furthermore, 4K TVs are

becoming the default resolution for mid-range and premium TV models, replacing

Full HD options, and gaining strong traction among home cinema enthusiasts.

Below

32 Inches Segment Was the Most Significant in the Global Smart TV Market by

Screen Size in 2025

By

Screen Size, the Smart TV Market is categorized into below 32 inches, 32 to 45 inches, 46 to 55 inches, 56 to 65

inches, and above 65 inches. The Below 32-inch segment captured the highest market share in 2025,

particularly due to its widespread use in small living spaces, bedrooms, and

secondary TV setups. This segment is notably popular in price-sensitive

regions, including South Asia and parts of Africa, where households prioritize

affordability and basic smart functionality. However, the market for larger

screens (above 55 inches) is expected to grow rapidly as consumers increasingly

prefer enhanced home theater-like viewing experiences and content in 4K and 8K

resolutions.

The following segments are

part of an in-depth analysis of the global Smart TV market:

|

Market Segments |

|

|

By Operating

System |

●

Android TV ●

Tizen ●

WebOS ●

Roku ●

Other) |

|

By Resolution |

●

4K UHD TV ●

HDTV ●

Full HD TV ●

8K TV |

|

By Screen Size |

●

Below 32 inches ●

32 to 45 inches ●

46 to 55 inches ●

56 to 65 inches ●

Above 65 inches |

|

By Technology |

●

OLED ●

QLED ●

LED ●

Others |

|

By

Distribution Channel |

●

Online ●

Offline |

Smart TV Market Share

Analysis by Region

The

North America region is projected to hold the largest

share of the global Smart TV market over the forecast period.

North

America dominated the global Smart TV Market in 2025, accounting for 38.9% of

total revenue. This leadership is driven by high household internet penetration

rates, a robust base of OTT service subscribers, and early adoption of premium

home entertainment systems. Consumers in the region exhibit a strong preference

for the latest-generation 4K and 8K TV panels,

alongside advanced features including voice assistants, Dolby Vision IQ, and

multi-device integration. Additionally, the presence of leading industry

players, strategic partnerships with streaming platforms, and rapidly growing

8K content availability are strengthening market traction in the U.S. and

Canada.

Asia

Pacific is anticipated to witness the fastest CAGR during the forecast period.

The region’s rapidly growing middle class, increase in disposable income, and

expansion of local manufacturing capabilities make it a significant growth hub.

Notably, high demand in China, India, and Southeast Asia, supported by

digitalization initiatives and rising broadband penetration, is fueling market

expansion. Local brands offering competitively priced smart TVs, along with

tailored regional content, contribute to the market's dynamism in APAC.

Smart TV Market

Competition Landscape Analysis

The Smart TV market is fragmented

with the presence of global giants and regional players. Key companies include

Samsung Electronics Co., Ltd., LG Electronics Inc., Sony Corporation, TCL

Electronics, and Hisense International. These players invest heavily in R&D

to innovate display technologies like QD-OLED and MicroLED. Partnerships with

content platforms and AI-chip integration serve as strategic differentiators.

Emerging companies like Vizio, Xiaomi, and OnePlus focus on affordability and

localized content. Mergers, smart home integration strategies, and voice

assistant compatibility remain core competitive elements.

Global Smart TV Market

Recent Developments News:

- In August 2024,

Haier Group Corporation introduced its premium M95E series QD-Mini LED

4K televisions in the Indian market. The new models are engineered with

advanced display, audio, and gaming technologies to deliver a high-quality

home entertainment experience.

- In July 2024,

Sony Group Corporation launched the BRAVIA 7 series, featuring Mini

LED backlighting, the Cognitive Processor XR, and XR Triluminos Pro

technology. The lineup is designed to offer enhanced picture and sound

quality, creating a more immersive and realistic viewing experience.

- In July 2024,

Koninklijke Philips N.V. released its 2024 OLED TV lineup in Europe,

including the OLED809 and OLED909 models. The OLED809 features a 144 Hz refresh rate, upgraded video

processing, and support for Apple AirPlay 2 and HomeKit. The OLED909

includes a 4-sided Ambilight system and succeeds the previous OLED908

model.

The Global Smart TV Market Is

Dominated by a Few Large Companies, such as

●

Haier Inc.

●

Hisense International

●

Intex Technologies

●

Koninklijke Philips

N.V

●

LG Electronics Inc

●

Panasonic Corporation

●

Samsung Electronics

Co. Ltd

●

Sansui Electric Co.

Ltd

●

Sony Corporation

●

TCL Electronics

Holdings Limited

●

Toshiba Visual

Solutions (TVS Regza Corporation)

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Smart TV Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Smart TV Market Scope and Market Estimation

1.2.1.Global Smart TV Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Smart TV Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Operating System of Global

Smart TV Market

1.3.2.Resolution of Global Smart

TV Market

1.3.3.Screen Size of Global Smart

TV Market

1.3.4.Technology of Global Smart

TV Market

1.3.5.Distribution Channel of

Global Smart TV Market

1.3.6.Region of Global Smart TV

Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Bn)

Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4. Demand and Opportunity

Assessment

2.5. Demand Supply Scenario

2.6. Market Dynamics

2.7. Drivers

2.8. Limitations

2.9. Opportunities

2.10. Impact Analysis of Drivers

and Restraints

2.11. Emerging Trends for

Lithium-ion Battery Recycling Market

2.12. Porter’s Five Forces

Analysis

2.13. PEST Analysis

2.14. Key Regulation

3. Global

Smart TV Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Smart TV Market Estimates & Forecast Trend Analysis, by

Operating System

4.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Operating System, 2020

- 2033

4.1.1.Android TV

4.1.2.Tizen

4.1.3.WebOS

4.1.4.Roku

4.1.5.Other

5.

Global Smart TV Market Estimates & Forecast Trend Analysis, by

Resolution

5.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Resolution, 2020 -

2033

5.1.1.4K UHD TV

5.1.2.HDTV

5.1.3.Full HD TV

5.1.4.8K TV

6.

Global Smart TV Market Estimates & Forecast Trend Analysis, by

Screen Size

6.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Form, 2020 - 2033

6.1.1.Below 32 inches

6.1.2.32 to 45 inches

6.1.3.46 to 55 inches

6.1.4.56 to 65 inches

6.1.5.Above 65 inches

7.

Global Smart TV Market Estimates & Forecast Trend Analysis, by

Technology

7.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Technology, 2020 -

2033

7.1.1.OLED

7.1.2.QLED

7.1.3.LED

7.1.4.Others

8. Global

Smart TV Market Estimates

& Forecast Trend Analysis, by Distribution Channel

8.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

8.1.1.Online

8.1.2.Offline

9. Global

Smart TV Market Estimates

& Forecast Trend Analysis, by Region

9.1.

Global

Smart TV Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

9.1.1.North America

9.1.2.Europe

9.1.3.Asia Pacific

9.1.4.Middle East & Africa

9.1.5.Latin America

10. North America Smart

TV Market: Estimates & Forecast

Trend Analysis

10.1. North America Smart TV

Market Assessments & Key Findings

10.1.1.

North

America Smart TV Market Introduction

10.1.2.

North

America Smart TV Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Operating System

10.1.2.2.

By Resolution

10.1.2.3.

By Screen Size

10.1.2.4.

By Technology

10.1.2.5.

By Distribution Channel

10.1.2.6. By Country

10.1.2.6.1. The U.S.

10.1.2.6.2. Canada

11. Europe Smart

TV Market: Estimates & Forecast

Trend Analysis

11.1. Europe Smart TV Market

Assessments & Key Findings

11.1.1. Europe Smart TV Market

Introduction

11.1.2. Europe Smart TV Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Operating System

11.1.2.2.

By Resolution

11.1.2.3.

By Screen Size

11.1.2.4.

By Technology

11.1.2.5.

By Distribution Channel

11.1.2.6. By Country

11.1.2.6.1.

Germany

11.1.2.6.2.

Italy

11.1.2.6.3.

U.K.

11.1.2.6.4.

France

11.1.2.6.5.

Spain

11.1.2.6.6.

Switzerland

11.1.2.6.7. Rest

of Europe

12. Asia Pacific Smart

TV Market: Estimates & Forecast

Trend Analysis

12.1. Asia Pacific Market

Assessments & Key Findings

12.1.1.

Asia

Pacific Smart TV Market Introduction

12.1.2.

Asia

Pacific Smart TV Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Operating System

12.1.2.2.

By Resolution

12.1.2.3.

By Screen Size

12.1.2.4.

By Technology

12.1.2.5.

By Distribution Channel

12.1.2.6. By Country

12.1.2.6.1. China

12.1.2.6.2. Japan

12.1.2.6.3. India

12.1.2.6.4. Australia

12.1.2.6.5. South Korea

12.1.2.6.6. Rest of Asia Pacific

13. Middle East & Africa Smart

TV Market: Estimates & Forecast

Trend Analysis

13.1. Middle East & Africa

Market Assessments & Key Findings

13.1.1. Middle

East & Africa

Smart TV Market Introduction

13.1.2. Middle

East & Africa

Smart TV Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Operating System

13.1.2.2.

By Resolution

13.1.2.3.

By Screen Size

13.1.2.4.

By Technology

13.1.2.5.

By Distribution Channel

13.1.2.6. By Country

13.1.2.6.1. UAE

13.1.2.6.2. Saudi

Arabia

13.1.2.6.3. South

Africa

13.1.2.6.4. Rest

of MEA

14. Latin America

Smart TV Market: Estimates &

Forecast Trend Analysis

14.1. Latin America Market

Assessments & Key Findings

14.1.1. Latin America Smart TV

Market Introduction

14.1.2. Latin America Smart TV

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

14.1.2.1.

By Operating System

14.1.2.2.

By Resolution

14.1.2.3.

By Screen Size

14.1.2.4.

By Technology

14.1.2.5. By Distribution

Channel

14.1.2.6. By Country

14.1.2.6.1. Brazil

14.1.2.6.2. Argentina

14.1.2.6.3. Mexico

14.1.2.6.4. Rest

of LATAM

15.

Country

Wise Market: Introduction

16.

Competition

Landscape

16.1. Global Smart TV Market Product

Mapping

16.2. Global Smart TV Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

16.3. Global Smart TV Market Tier

Structure Analysis

16.4. Global Smart TV Market

Concentration & Company Market Shares (%) Analysis, 2023

17.

Company

Profiles

17.1.

Haier Inc.

17.1.1.

Company

Overview & Key Stats

17.1.2.

Financial

Performance & KPIs

17.1.3.

Product

Portfolio

17.1.4.

SWOT

Analysis

17.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

17.2.

Hisense International

17.3.

Intex Technologies

17.4.

Koninklijke Philips N.V

17.5.

LG Electronics Inc

17.6.

Panasonic Corporation

17.7.

Samsung Electronics Co. Ltd

17.8.

Sansui Electric Co. Ltd

17.9.

Sony Corporation

17.10.

TCL Electronics Holdings Limited

17.11.

Toshiba Visual Solutions (TVS Regza Corporation)

17.12.

Others

18. Research

Methodology

18.1. External Transportations /

Databases

18.2. Internal Proprietary

Database

18.3. Primary Research

18.4. Secondary Research

18.5. Assumptions

18.6. Limitations

18.7. Report FAQs

19. Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables