Specimen Collection Cards Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type (Blood, Saliva, Urine, Buccal Cells, Others); By Material (Cotton & Cellulose-based, Fiber-based, Others); By Product (Whatman 903, Ahlstrom 226, FTA, Others); By Application (Newborn Screening (NBS), Infectious Diseases Testing, Therapeutic Drug Monitoring, Forensics, Research, Wellbeing/Health Monitoring, Other Applications); By Distribution Channel (Online, Offline); By End Use (Hospitals & Clinics, Diagnostic Centers, Others); and Geography

2025-11-27

Healthcare

Swetal (Research Analyst)

Description

Specimen Collection Cards Market Overview

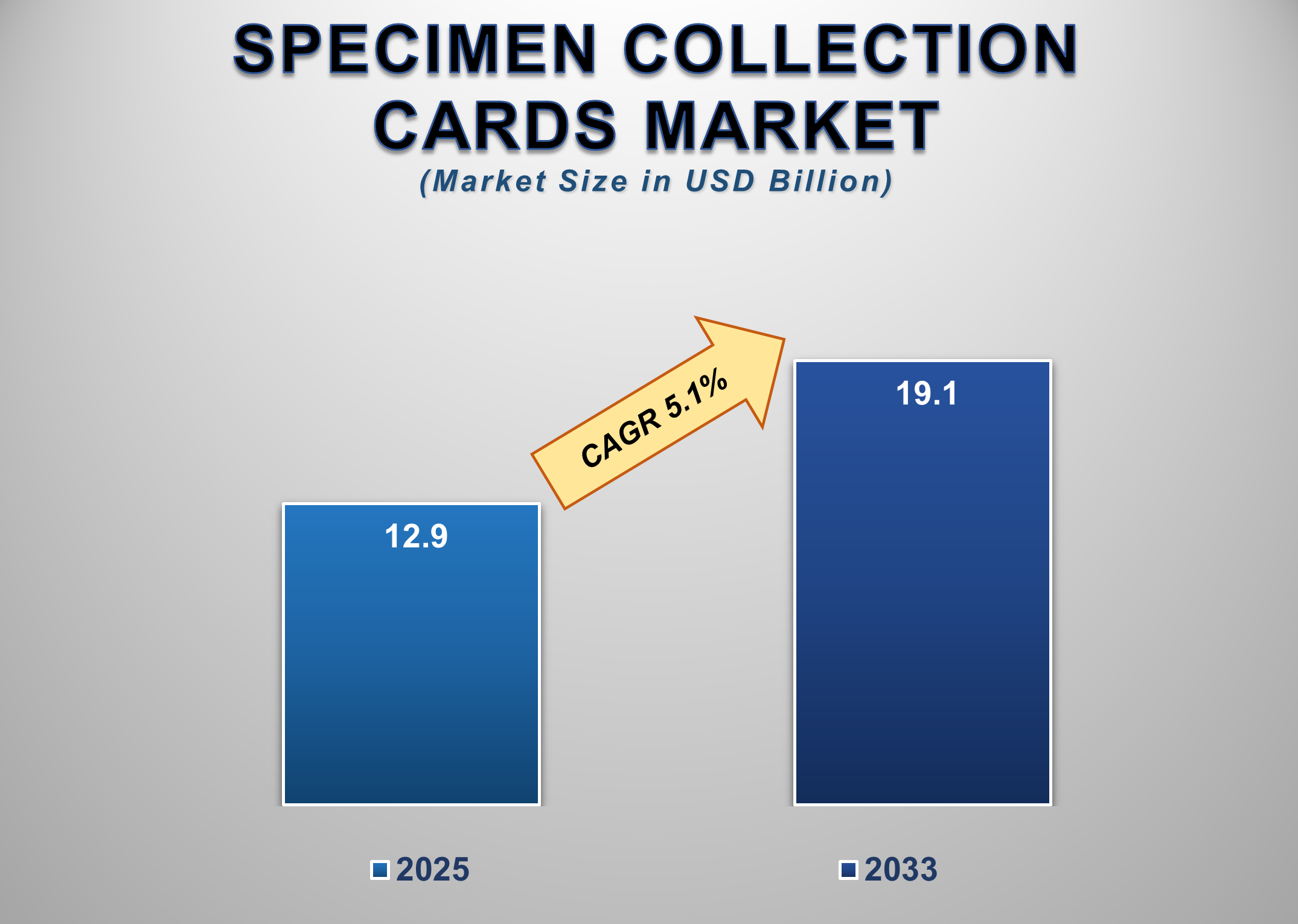

The Global Specimen Collection Cards Market is experiencing strong growth driven by the rising need for simplified, non-invasive, and cost-effective sample collection solutions across healthcare and research applications. Valued at USD 12.9 billion in 2025, the market is projected to reach USD 19.1 billion by 2033, expanding at a CAGR of 5.1% during the forecast period.

Specimen collection cards are

specialized tools used to collect, transport, and store biological samples such

as blood, saliva, urine, or buccal cells in a dry and stable format. They are

essential in newborn screening, infectious disease testing, forensic analysis,

therapeutic drug monitoring, and genomic research. Their ease of use, low

biohazard risk, and ability to maintain sample integrity without refrigeration

make them highly valuable, especially in resource-limited or remote areas. The

market’s expansion is supported by the increasing adoption of decentralized

testing and home-based sample collection, advancements in molecular

diagnostics, and government programs for disease surveillance and neonatal

screening. Moreover, specimen collection cards play a critical role in

epidemiological studies and biobanking, where long-term sample preservation is

essential.

Specimen Collection Cards

Market Drivers and Opportunities

Growing

adoption of remote diagnostics and decentralized testing drives market growth

One of the major drivers fueling the specimen collection cards

market is the global shift toward remote diagnostics, home-based testing, and

decentralized laboratory workflows. The demand for point-of-care testing has

surged as healthcare systems prioritize accessibility, convenience, and rapid

diagnosis. Specimen collection cards, particularly dried blood spot (DBS) and

FTA cards, offer a practical and affordable method for collecting,

transporting, and analyzing samples without requiring cold-chain logistics or

immediate laboratory processing. The growing prevalence of chronic diseases,

infectious outbreaks, and public health screening programs has increased the

need for efficient sample collection methods that can reach underserved

populations. Programs like newborn screening (NBS) and large-scale

epidemiological studies have widely adopted these cards due to their ease of

storage and minimal biohazard risk. Moreover, emerging markets in the Asia

Pacific, Latin America, and Africa are deploying DBS cards for HIV, hepatitis,

and metabolic disorder testing, enhancing early detection capabilities. The

combination of technology integration, such as barcoding and digital tracking,

with simplified sampling formats is making specimen collection more

standardized and reliable. With healthcare models increasingly emphasizing

accessibility and preventive care, specimen collection cards are becoming an

indispensable part of the diagnostic infrastructure globally.

Advancements in molecular diagnostics and biobanking bolster

global demand

Continuous innovations in molecular biology, genomics, and

proteomics are expanding the scope of specimen collection cards beyond

conventional screening. Modern cards are designed to preserve nucleic acids and

proteins effectively, enabling downstream applications such as PCR, NGS, and

biomarker analysis. These innovations ensure that small sample volumes

collected from DBS cards can deliver reliable results comparable to traditional

venipuncture samples. The rise of precision medicine and biobanking initiatives

is another strong growth driver. Biorepositories and research institutions are

increasingly using specimen cards for long-term storage of biological material

because of their stability and reduced storage costs. Their compatibility with

automation and data-driven laboratory management systems further enhances

efficiency and scalability. In addition, regulatory bodies and healthcare

organizations worldwide are supporting the standardization of specimen

collection processes. This encourages adoption across clinical trials, drug

monitoring, and disease surveillance programs. The convergence of molecular

diagnostics and simplified sampling technologies positions specimen collection

cards as a critical enabler of modern healthcare, particularly in personalized

diagnostics and population genomics.

Expanding applications in precision medicine and global health programs offer significant opportunities

The growing focus on precision medicine, telehealth, and global disease surveillance presents vast opportunities for the specimen collection cards market. As healthcare systems move toward personalized and data-driven care, there is a growing need for standardized, stable, and scalable sample collection tools that can support genetic, proteomic, and metabolomic analyses. Specimen collection cards are emerging as a preferred medium for collecting minimally invasive samples that can be used in large-scale cohort studies, longitudinal monitoring, and remote patient management. Furthermore, government-backed newborn screening programs and global health initiatives for HIV, hepatitis, and tuberculosis are expanding the use of DBS and FTA cards. These cards are being integrated into digital health ecosystems that allow real-time sample tracking, remote diagnostics, and electronic health record (EHR) integration. In parallel, advancements in card materials and surface chemistry are improving analyte recovery, sensitivity, and reproducibility.

Specimen Collection Cards

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 12.9 Billion |

|

Market Forecast in 2033 |

USD 19.1 Billion |

|

CAGR % 2025-2033 |

5.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type ●

By Material ●

By Product ●

By Application ●

By Distribution

Channel ●

By End Use |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Specimen Collection Cards

Market Report Segmentation Analysis

The global Specimen Collection

Cards Market is segmented by Type, Material, Product, Application, Distribution

Channel, End Use, and Region.

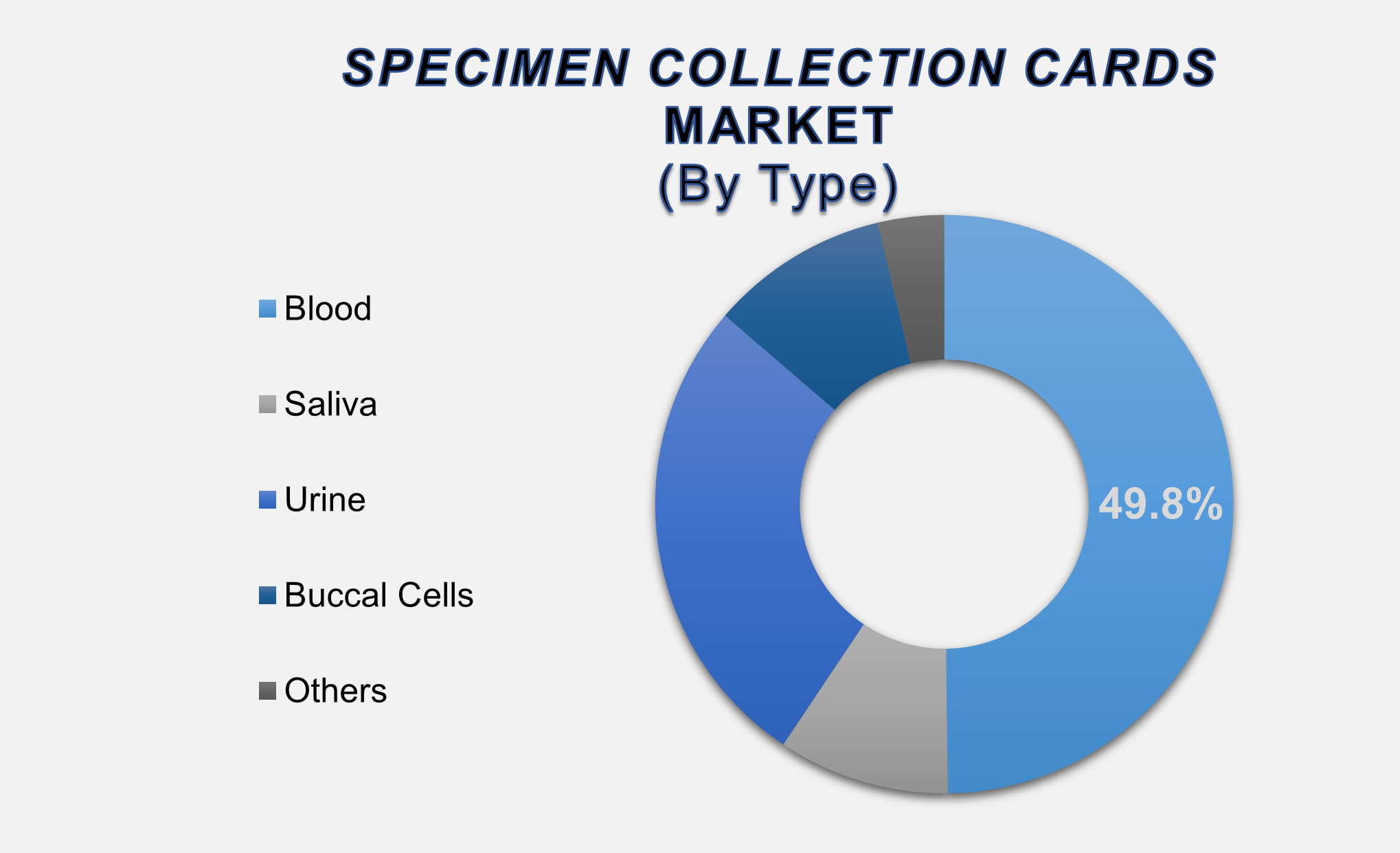

The

blood segment accounted for the largest market share in the global Specimen Collection

Cards market

By

Type, the market is segmented into Blood, Saliva, Urine, Buccal Cells, and

Others. The Blood segment dominates the global specimen collection cards

market, holding the largest share of around 49.8% in 2025. Dried blood spot

(DBS) collection is the most established method, extensively used in newborn

screening, infectious disease testing, and therapeutic drug monitoring. The

widespread clinical validation, ease of collection, and compatibility with

analytical methods like mass spectrometry and PCR drive this segment’s

dominance. Moreover, the increasing use of DBS cards in remote diagnostics and

pharmacokinetic studies further enhances their demand. The non-invasive nature,

reduced sample volume requirement, and simplified logistics have made

blood-based specimen cards the preferred choice in both clinical and research

settings. Continuous innovation in card substrates and spotting technologies

ensures accuracy, stability, and reproducibility across applications,

solidifying the blood segment’s leading position.

The cotton & Cellulose-based material segment dominates the

specimen collection cards market

By Material, the market divides into Cotton & Cellulose-based, Fiber-based, and Others. The Cotton & Cellulose-based segment holds the largest share in 2025 due to its widespread adoption, cost-effectiveness, and compatibility with a wide range of biological samples. These materials offer high absorbency, chemical stability, and uniform sample distribution—critical features for ensuring accurate diagnostic results. Products such as Whatman 903 and Ahlstrom 226 are manufactured using high-quality cellulose fibers and are widely used in clinical and research laboratories. Additionally, the natural porosity of cotton and cellulose materials facilitates efficient sample drying and long-term stability, minimizing degradation. Ongoing R&D is focused on enhancing the chemical treatment of these substrates to improve nucleic acid and protein recovery, further strengthening their dominance in the market.

The Whatman

903 product segment leads the global specimen collection cards market

By

Product, the market is segmented into Whatman 903, Ahlstrom 226, FTA, and

Others. The Whatman 903 card segment leads globally, recognized as the industry

standard for newborn screening and blood spot collection. Manufactured from

pure cellulose, Whatman 903 cards ensure consistent performance and

compatibility with diverse analytical workflows. Their use is endorsed by major

health organizations such as the CDC and WHO, reinforcing their clinical

credibility. The extensive use of Whatman 903

cards in metabolic screening, infectious disease detection, and genetic testing

programs continues to drive growth. Their proven quality, regulatory

acceptance, and widespread availability make them the most trusted choice among

healthcare providers and laboratories worldwide.

The following segments are

part of an in-depth analysis of the global Specimen Collection Cards market:

|

Market Segments |

||||||||

|

By Type |

●

Blood ●

Saliva ●

Urine ●

Buccal Cells ●

Others |

|||||||

|

By Material |

|

|||||||

|

By Product |

|

|||||||

|

By Application |

|

|||||||

|

By Distribution Channel |

|

|||||||

|

By End Use |

|

|||||||

Specimen Collection Cards

Market Share Analysis by Region

The

Asia Pacific region is projected to hold the largest

share of the global Specimen Collection Cards market over the forecast period

The

Asia Pacific (APAC) region accounted for 40.3% of the global market in 2025 and

is expected to maintain its dominance throughout the forecast period. The

region’s leadership is attributed to the rapid expansion of newborn screening

programs, increasing healthcare investments, and strong government support for

disease surveillance initiatives. Countries such as China, India, and Japan are

deploying large-scale screening and research programs that utilize dried blood

spot and saliva collection cards. The growing adoption of point-of-care

diagnostics, rising awareness about preventive health, and the proliferation of

research collaborations between academic and commercial institutions further

propel regional growth. Local manufacturing initiatives and affordable card

options also enhance accessibility in developing economies.

In

contrast, North America is expected to register the fastest CAGR during

2025–2033, driven by technological innovation, extensive research

infrastructure, and the presence of major manufacturers. The U.S. market

benefits from strong regulatory support, a focus on personalized medicine, and

expanding applications of specimen cards in forensic and clinical research.

Specimen Collection Cards

Market Competition Landscape Analysis

The global specimen collection

cards market is moderately consolidated, with a mix of established players and

emerging innovators competing based on product quality, certification, and

application diversity. Leading manufacturers focus on enhancing sample

preservation technologies, expanding digital integration, and forming

collaborations with healthcare agencies and research bodies.

Global Specimen

Collection Cards Market Recent Developments News:

- In November 2024,

Capitainer launched the Capitainer SEP10 collection card, a novel sampling

device that enables the separation of cells from plasma at the point of

collection without centrifugation. The product is set to be available in

both the U.S. and the European Union

markets.

- In September 2022,

Capitainer, a Swedish startup, announced highly positive performance

results for its qDBS card, a volumetric dried blood spot sampling device.

The technology demonstrated accurate testing for phenylketonuria,

overcoming limitations of conventional cards related to volume and

hematocrit variability.

- In January 2024,

Capitainer established miQro Lab Solutions, a new U.S. laboratory in

Warwick, Rhode Island. This facility is designed to accelerate the

integration of Capitainer’s self-sampling and diagnostic technologies into

the U.S. healthcare system, supporting faster adoption of its

user-friendly solutions.

The Global Specimen Collection Cards

Market Is Dominated by a Few Large Companies, such as

●

Thermo Fisher

Scientific

●

Whatman (GE

Healthcare)

●

PerkinElmer

●

Centers for Disease

Control and Prevention

●

Qiagen

●

Merck KGaA

●

Sarstedt

●

Ahlstrom-Munksjö

●

ARCHIMEDES

●

LIA Diagnostics

●

FortiusBio

●

Macherey-Nagel

●

Cepheid

●

Bio-Rad Laboratories

●

Shimadzu Corporation

●

MEDISO

●

Nupore Filtration

●

Cytiva

●

LOPROCO

●

Lab-AidsOthers

● Others

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Specimen Collection

Cards Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Specimen Collection Cards Market Scope and Market Estimation

1.2.1.Global Specimen Collection

Cards Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Specimen Collection

Cards Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Specimen

Collection Cards Market

1.3.2.Material of Global Specimen

Collection Cards Market

1.3.3.Product of Global Specimen

Collection Cards Market

1.3.4.Distribution Channel of

Global Specimen Collection Cards Market

1.3.5.Application of Global Specimen

Collection Cards Market

1.3.6.End-use of Global Specimen

Collection Cards Market

1.3.7.Region of Global Specimen

Collection Cards Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Specimen Collection Cards Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Specimen Collection

Cards Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.1.

Blood

4.1.1.2.

Saliva

4.1.1.3.

Urine

4.1.1.4.

Buccal

Cells

4.1.1.5.

Others

5.

Global Specimen Collection

Cards Market Estimates

& Forecast Trend Analysis, by Material

5.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Material,

2020 - 2033

5.1.1.Cotton &

Cellulose-based

5.1.2.Fiber-based

5.1.3.Others

6.

Global Specimen Collection

Cards Market Estimates

& Forecast Trend Analysis, by Product

6.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

6.1.1.Whatman 903

6.1.2.Ahlstrom 226

6.1.3.FTA

6.1.4.Others

7.

Global Specimen Collection

Cards Market Estimates

& Forecast Trend Analysis, by Distribution Channel

7.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

7.1.1.Online

7.1.2.Offline

8.

Global Specimen Collection

Cards Market Estimates

& Forecast Trend Analysis, by Application

8.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

8.1.1.New Born Screening (NBS)

8.1.2.Infectious Diseases

Testing

8.1.3.Therapeutic Drug

Monitoring

8.1.4.Forensics

8.1.5.Research

8.1.6.Wellbeing/Health

Monitoring

8.1.7.Other Applications

9. Global

Specimen Collection Cards Market Estimates

& Forecast Trend Analysis, by End-use

9.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by End-use,

2020 - 2033

9.1.1.Hospitals & Clinics

9.1.2.Diagnostics Centers

9.1.3.Others

10. Global

Specimen Collection Cards Market Estimates

& Forecast Trend Analysis, by Region

10.1.

Global

Specimen Collection Cards Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

10.1.1.

North

America

10.1.2.

Europe

10.1.3.

Asia

Pacific

10.1.4.

Middle

East & Africa

10.1.5.

Latin

America

11. North America Specimen

Collection Cards Market: Estimates

& Forecast Trend Analysis

11.1. North America Specimen

Collection Cards Market Assessments & Key Findings

11.1.1.

North

America Specimen Collection Cards Market Introduction

11.1.2.

North

America Specimen Collection Cards Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Material

11.1.2.3.

By Product

11.1.2.4.

By Distribution Channel

11.1.2.5.

By Application

11.1.2.6.

By End-use

11.1.2.7. By Country

11.1.2.7.1. The U.S.

11.1.2.7.2. Canada

12. Europe Specimen

Collection Cards Market: Estimates

& Forecast Trend Analysis

12.1. Europe Specimen Collection

Cards Market Assessments & Key Findings

12.1.1. Europe Specimen Collection

Cards Market Introduction

12.1.2. Europe Specimen Collection

Cards Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Material

12.1.2.3.

By Product

12.1.2.4.

By Distribution Channel

12.1.2.5.

By Application

12.1.2.6.

By End-use

12.1.2.7. By Country

12.1.2.7.1.

Germany

12.1.2.7.2.

Italy

12.1.2.7.3.

U.K.

12.1.2.7.4.

France

12.1.2.7.5.

Spain

12.1.2.7.6.

Switzerland

12.1.2.7.7. Rest

of Europe

13. Asia Pacific Specimen

Collection Cards Market: Estimates

& Forecast Trend Analysis

13.1. Asia Pacific Market

Assessments & Key Findings

13.1.1.

Asia

Pacific Specimen Collection Cards Market Introduction

13.1.2.

Asia

Pacific Specimen Collection Cards Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

13.1.2.1.

By Type

13.1.2.2.

By Material

13.1.2.3.

By Product

13.1.2.4.

By Distribution Channel

13.1.2.5.

By Application

13.1.2.6.

By End-use

13.1.2.7. By Country

13.1.2.7.1. China

13.1.2.7.2. Japan

13.1.2.7.3. India

13.1.2.7.4. Australia

13.1.2.7.5. South Korea

13.1.2.7.6. Rest of Asia Pacific

14. Middle East & Africa Specimen

Collection Cards Market: Estimates

& Forecast Trend Analysis

14.1. Middle East & Africa

Market Assessments & Key Findings

14.1.1. Middle

East & Africa

Specimen Collection Cards Market Introduction

14.1.2. Middle

East & Africa

Specimen Collection Cards Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

14.1.2.1.

By Type

14.1.2.2.

By Material

14.1.2.3.

By Product

14.1.2.4.

By Distribution Channel

14.1.2.5.

By Application

14.1.2.6.

By End-use

14.1.2.7. By Country

14.1.2.7.1. UAE

14.1.2.7.2. Saudi

Arabia

14.1.2.7.3. South

Africa

14.1.2.7.4. Rest

of MEA

15. Latin America

Specimen Collection Cards Market:

Estimates & Forecast Trend Analysis

15.1. Latin America Market

Assessments & Key Findings

15.1.1. Latin America Specimen

Collection Cards Market Introduction

15.1.2. Latin America Specimen

Collection Cards Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

15.1.2.1.

By Type

15.1.2.2.

By Material

15.1.2.3.

By Product

15.1.2.4.

By Distribution Channel

15.1.2.5.

By Application

15.1.2.6. By End-use

15.1.2.7. By Country

15.1.2.7.1. Brazil

15.1.2.7.2. Argentina

15.1.2.7.3. Mexico

15.1.2.7.4. Rest

of LATAM

16.

Country

Wise Market: Introduction

17.

Competition

Landscape

17.1. Global Specimen Collection

Cards Market Product Mapping

17.2. Global Specimen Collection

Cards Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

17.3. Global Specimen Collection

Cards Market Tier Structure Analysis

17.4. Global Specimen Collection

Cards Market Concentration & Company Market Shares (%) Analysis, 2023

18.

Company

Profiles

18.1.

Thermo Fisher Scientific

18.1.1.

Company

Overview & Key Stats

18.1.2.

Financial

Performance & KPIs

18.1.3.

Product

Portfolio

18.1.4.

SWOT

Analysis

18.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

18.2.

Whatman (GE Healthcare)

18.3.

PerkinElmer

18.4.

Centers for Disease Control and Prevention

18.5.

Qiagen

18.6.

Merck KGaA

18.7.

Sarstedt

18.8.

Ahlstrom-Munksjö

18.9.

ARCHIMEDES

18.10.

LIA Diagnostics

18.11.

FortiusBio

18.12.

Macherey-Nagel

18.13.

Cepheid

18.14.

Bio-Rad Laboratories

18.15.

Shimadzu Corporation

18.16.

MEDISO

18.17.

Nupore Filtration

18.18.

Cytiva

18.19.

LOPROCO

18.20.

Lab-Aids

18.21.

Others

19. Research

Methodology

19.1. External Transportations /

Databases

19.2. Internal Proprietary

Database

19.3. Primary Research

19.4. Secondary Research

19.5. Assumptions

19.6. Limitations

19.7. Report FAQs

20. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables