Structural Insulated Panels Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (Expanded Polystyrene Panels, Polyurethane Panels, Polyisocyanurate Panels, Glass Wool Panels, Others); By Application (Residential Construction, Commercial Construction, Industrial Buildings, Cold Storage Facilities, Agricultural Buildings, Others); By Skin Material (Oriented Strand Board, Metal, Cement Board, Plywood, Others); By End User (Construction Companies, Real Estate Developers, Infrastructure Contractors, Industrial Facilities, Others), and Geography

2026-06-01

Real Estate & Infrastructure

Ekta Chaurasia (Team Lead)

Description

Structural

Insulated Panels Market Overview

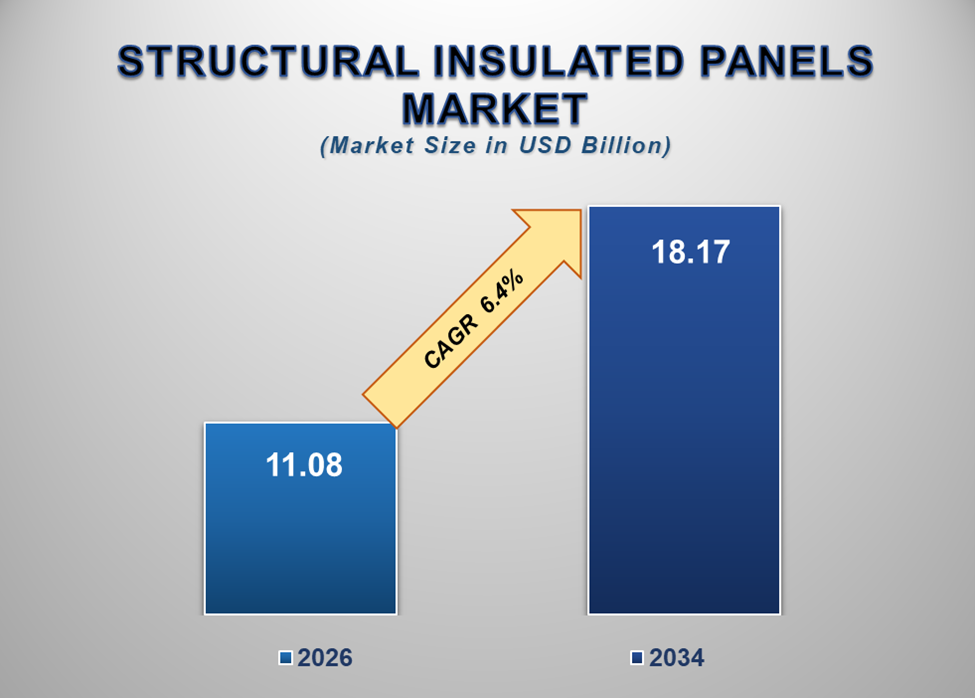

The global Structural Insulated Panels

market was valued at USD 11.08 billion in 2026 and is projected to

reach USD 18.17 billion by 2034, expanding at a CAGR of 6.4% during

the forecast period. The market is witnessing significant growth due to

increasing demand for energy-efficient buildings, rising adoption of

sustainable construction materials, growing focus on reducing construction

timelines, and expanding investments in prefabricated building technologies

worldwide.

Structural insulated panels (SIPs) are

high-performance building materials consisting of an insulating foam core

sandwiched between two structural facings such as oriented strand board (OSB),

metal sheets, or cement boards. These panels are widely utilized in walls,

roofs, and floors across residential, commercial, industrial, and institutional

construction projects.

The increasing global emphasis on

sustainable construction and energy conservation is significantly accelerating

the adoption of structural insulated panels. SIPs provide superior thermal

insulation, airtightness, and structural strength compared to traditional

construction materials, helping reduce building energy consumption and

operational costs.

Governments and regulatory agencies

worldwide are implementing stringent building energy efficiency standards and

green building regulations, encouraging developers and contractors to adopt

advanced insulation systems and environmentally sustainable construction

materials.

The rapid expansion of prefabricated and

modular construction is another major factor driving market growth. Structural

insulated panels support faster construction timelines, reduced labor

requirements, improved material efficiency, and minimized on-site waste

generation.

Additionally, increasing urbanization and

infrastructure development activities are generating strong demand for modern

building technologies capable of improving structural durability, occupant

comfort, and energy performance.

Technological advancements in insulation

materials, panel manufacturing processes, fire-resistant coatings, and

moisture-resistant structural systems are further improving SIP performance and

application versatility.

As the global construction industry continues prioritizing sustainability, energy efficiency, and rapid project execution, the structural insulated panels market is expected to witness steady expansion through 2034.

Structural Insulated Panels Market Drivers and OpportunitiesRising Demand for Energy-efficient and Sustainable Buildings Is Driving Market Growth

The growing demand for energy-efficient

buildings is one of the primary drivers of the structural insulated panels

market. Building owners, developers, and governments increasingly prioritize

reducing energy consumption and greenhouse gas emissions associated with

heating and cooling systems.

Structural insulated panels provide high

thermal resistance and minimize thermal bridging, helping maintain stable

indoor temperatures and reduce energy loss. These performance benefits make

SIPs highly suitable for green buildings and low-energy construction projects.

The increasing adoption of sustainable

building certifications such as LEED and net-zero energy building initiatives

is further encouraging the utilization of advanced insulation systems across

residential and commercial construction sectors.

Additionally, rising electricity costs and

growing awareness regarding long-term operational savings are motivating

property developers and homeowners to invest in highly insulated building

materials.

The superior structural integrity and durability of SIPs also contribute to improved building lifespan and lower maintenance requirements, further supporting market growth.

Expansion of Prefabricated and Modular

Construction Is Fueling Market Expansion

The rapid growth of prefabricated and

modular construction methods is significantly contributing to market expansion.

Construction companies increasingly seek building systems capable of reducing

labor dependency, minimizing project delays, and improving overall construction

efficiency.

Structural insulated panels are extensively

utilized in off-site prefabrication processes because they can be manufactured

to precise dimensions and quickly assembled at construction sites.

The use of SIPs reduces construction waste,

improves quality control, and accelerates project completion timelines compared

to conventional building methods.

Additionally, growing labor shortages

within the construction industry are encouraging developers to adopt

prefabricated construction technologies that simplify installation and reduce

workforce requirements.

The increasing demand for affordable housing, temporary structures, educational facilities, healthcare infrastructure, and cold storage facilities is also supporting the adoption of SIP-based construction systems globally.

Advancements in Smart Building

Technologies and Green Infrastructure Present Significant Opportunities

The integration of smart building

technologies and green infrastructure initiatives presents substantial

opportunities for the structural insulated panels market.

Smart buildings increasingly require

advanced insulation materials capable of improving energy efficiency and

supporting intelligent climate control systems. SIPs help optimize HVAC system

performance and reduce building energy loads.

Advancements in fire-resistant insulation

materials, moisture-resistant coatings, recyclable panel materials, and

environmentally sustainable foam cores are expanding application opportunities

across diverse climatic conditions and construction environments.

Additionally, increasing government

investments in sustainable urban infrastructure and climate-resilient building

development are creating opportunities for high-performance insulation systems

globally.

Cold storage infrastructure expansion

within food logistics and pharmaceutical supply chains is also generating

increasing demand for structural insulated panels with superior thermal

insulation capabilities.

Emerging economies are witnessing rapid

urbanization and infrastructure modernization, creating additional growth

opportunities for SIP manufacturers and prefabricated construction solution

providers.

As sustainable construction practices and smart infrastructure development continue accelerating worldwide, demand for structural insulated panels is expected to rise significantly.

Structural Insulated Panels Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD

11.08 Billion |

|

Market Forecast in 2034 |

USD 18.17 Billion |

|

CAGR % 2026-2034 |

6.4% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption, Company

Share, Company Heatmap, Company Production, Service Type, Growth Factors and

more |

|

Segments Covered |

∙ By Product Type |

|

Regional Scope |

● North

America ● Europe ● APAC ● Latin

America ● Middle

East and Africa |

|

Country Scope |

U.S. Canada U.K. Germany France Italy Spain Switzerland China India Japan South Korea Australia Mexico Brazil Argentina Saudi Arabia UAE South Africa |

Structural Insulated Panels Market Report

Segmentation Analysis

The global structural insulated panels market industry analysis is segmented by product type, by application, by skin material, by end user, and by region.

Expanded Polystyrene Panels Segment Is

Expected to Dominate the Market During the Forecast Period

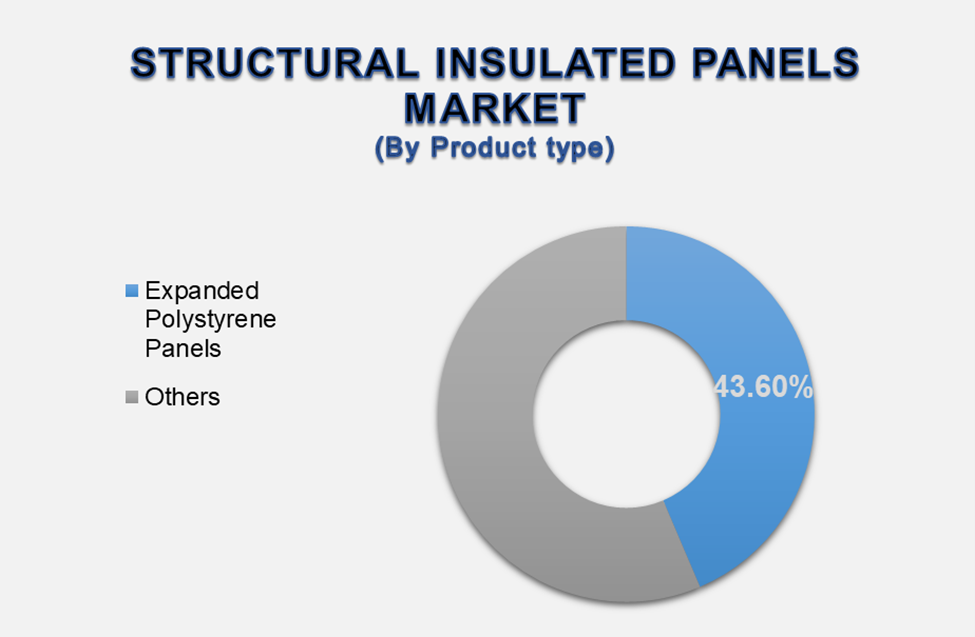

The expanded polystyrene (EPS) panels

segment accounted for approximately 43.6% of the global market, making

it the dominant product category.

EPS-based structural insulated panels are

widely utilized due to their lightweight structure, cost-effectiveness, high

thermal insulation performance, and moisture resistance.

These panels are extensively used in

residential housing, commercial buildings, cold storage facilities, and modular

construction projects.

The increasing demand for affordable and energy-efficient construction materials is significantly supporting the growth of the EPS panel segment globally.

Residential Construction Segment Is

Expected to Lead the Market by Application

Residential construction dominates the

application segment due to increasing demand for sustainable housing and

energy-efficient residential infrastructure.

Homebuilders increasingly utilize SIPs to

improve insulation performance, reduce utility costs, and accelerate project

completion timelines.

The growing adoption of prefabricated

housing systems and modular residential construction is significantly

contributing to segment expansion.

Additionally, rising consumer awareness regarding environmentally sustainable homes and long-term energy savings is accelerating the utilization of insulated building panels within residential construction projects.

Oriented Strand Board Segment Is Expected

to Dominate the Market by Skin Material

Oriented strand board (OSB) represents the

leading skin material segment within the structural insulated panels market due

to its structural strength, durability, affordability, and compatibility with

insulation cores.

OSB-faced SIPs are extensively utilized

across residential and commercial applications because they provide excellent

load-bearing performance and ease of installation.

Advancements in moisture-resistant and fire-retardant OSB technologies are further improving segment adoption across modern construction projects.

The Construction Companies Segment Is

Expected to Lead the End-User Market

Construction companies account for the

largest market share due to the increasing adoption of prefabricated

construction technologies and high-performance building materials.

Contractors increasingly utilize structural

insulated panels to improve project efficiency, reduce labor costs, and comply

with energy efficiency regulations.

The growing emphasis on rapid

infrastructure development and sustainable building practices is significantly

supporting demand for SIP systems among construction firms globally.

The following segments are part of an

in-depth analysis of the global Structural Insulated Panels market:

|

Market Segments |

|

|

By Skin Material |

∙ Oriented Strand Board |

|

By

Product Type |

∙ Expanded Polystyrene Panels |

|

By Application |

∙ Residential

Construction |

|

By End User |

∙ Construction Companies |

Structural Insulated Panels Market Share

Analysis By Region

North America is projected to hold the

largest share of the global structural insulated panels market over the

forecast period.

North America accounted for approximately 36.9%

of the global market in 2026, driven by strong adoption of energy-efficient

construction technologies, advanced prefabricated building industries, and

stringent building energy regulations.

The United States remains the dominant

contributor due to increasing demand for sustainable housing, modular

construction systems, and green building certifications.

Canada is also witnessing the rising

adoption of insulated building materials due to cold climate conditions and a

strong emphasis on energy-efficient residential infrastructure.

Europe represents another significant

market due to strict environmental regulations, carbon reduction targets, and

increasing investments in sustainable building development.

Asia Pacific is expected to register the

highest CAGR during the forecast period due to rapid urbanization,

infrastructure expansion, and increasing government support for affordable and

energy-efficient housing projects.

China, India, Japan, and South Korea are witnessing growing adoption of prefabricated construction technologies and modern insulation systems, further supporting regional market growth.

Structural Insulated Panels Market

Competition Landscape Analysis

The structural insulated panels market is

highly competitive and innovation-driven, with leading companies focusing on

advanced insulation technologies, sustainable materials, prefabricated

construction systems, and energy-efficient building solutions.

Manufacturers are increasingly investing in

recyclable insulation cores, fire-resistant panel technologies,

moisture-resistant coatings, and automated manufacturing systems to improve

product performance and environmental sustainability.

Strategic partnerships between construction firms, panel manufacturers, modular housing companies, and green infrastructure developers are becoming increasingly common as organizations seek to expand technological capabilities and market presence.

Global Structural Insulated Panels Market

Recent Developments News:

∙ In March 2026 – Construction companies

accelerated the adoption of structural insulated panels for modular housing and

sustainable infrastructure projects.

∙ In January 2026 – Advanced fire-resistant and moisture-resistant SIP

technologies gained increased commercialization globally.

∙ In October 2025 – Green building initiatives and net-zero energy construction

projects significantly boosted demand for high-performance insulation systems.

∙ In August 2025 – Prefabricated construction manufacturers expanded production

capacity for energy-efficient structural panel systems.

∙ In June 2025 – Cold storage and temperature-controlled infrastructure

projects increasingly adopted SIP-based insulation technologies.

The Global Structural Insulated Panels

Market is dominated by a few large companies, such as

∙ Kingspan Group plc

∙ Owens Corning

∙ PFB Corporation

∙ Metl-Span LLC

∙ Nucor Corporation

∙ Premier Building Systems

∙ Structural Panels Inc.

∙ Insulspan Inc.

∙ R-Control SIPs

∙ SIPCO

∙ Foard Panel Inc.

∙ Extreme Panel Technologies Inc.

∙ Alubel S.p.A.

∙ Eagle Panel Systems, Inc.

∙ Isopan S.p.A.

∙ Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Structural

Insulated Panels Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Structural Insulated Panels Market Scope and Market

Estimation

1.2.1.

Global Structural Insulated

Panels Overall Market Size (US$ Million), Market CAGR (%), Market Forecast

(2026 - 2034)

1.2.2.

Global Structural Insulated

Panels Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1.

Product Type of Global

Structural Insulated Panels Market

1.3.2.

Application of Global

Structural Insulated Panels Market

1.3.3.

Skin Material of Global

Structural Insulated Panels Market

1.3.4.

End User of Global Structural

Insulated Panels Market

1.3.5.

Region of Global Structural

Insulated Panels Market

1.4. Competition Coverage List of Market Participants

1.5. Market Definition: Structural Insulated Panels Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Million) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Tariff, Regulatory Landscape and Standards

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global Structural

Insulated Panels Market Estimates & Historical Trend Analysis (2021 - 2025)

4.

Global Structural

Insulated Panels Market Estimates & Forecast Trend Analysis, by Product

Type

4.1. Global Structural Insulated Panels Market Revenue (US$ Million)

Estimates and Forecasts, by Product Type, 2021 - 2034

4.1.1.

Expanded Polystyrene Panels

4.1.2.

Polyurethane Panels

4.1.3.

Polyisocyanurate Panels

4.1.4.

Glass Wool Panels

4.1.5.

Others

5.

Global Structural

Insulated Panels Market Estimates & Forecast Trend Analysis, by Application

5.1. Global Structural Insulated Panels Market Revenue (US$ Million)

Estimates and Forecasts, by Application, 2021 - 2034

5.1.1.

Residential Construction

5.1.2.

Commercial Construction

5.1.3.

Industrial Buildings

5.1.4.

Cold Storage Facilities

5.1.5.

Agricultural Buildings

5.1.6.

Others

6.

Global Structural

Insulated Panels Market Estimates & Forecast Trend Analysis, by Skin

Material

6.1. Global Structural Insulated Panels Market Revenue (US$ Million)

Estimates and Forecasts, by Skin Material, 2021 - 2034

6.1.1.

Oriented Strand Board

6.1.2.

Metal

6.1.3.

Cement Board

6.1.4.

Plywood

6.1.5.

Others

7.

Global Structural

Insulated Panels Market Estimates & Forecast Trend Analysis, by End User

7.1. Global Structural Insulated Panels Market Revenue (US$ Million)

Estimates and Forecasts, by End User, 2021 - 2034

7.1.1.

Construction Companies

7.1.2.

Real Estate Developers

7.1.3.

Infrastructure Contractors

7.1.4.

Industrial Facilities

7.1.5.

Others

8.

Global Structural

Insulated Panels Market Estimates & Forecast Trend Analysis, by Region

8.1. Global Structural Insulated Panels Market Revenue (US$ Million)

Estimates and Forecasts, by Region, 2021 - 2034

8.1.1.

North America

8.1.2.

Europe

8.1.3.

Asia Pacific

8.1.4.

Middle East & Africa

8.1.5.

Lain America

9.

North America Structural

Insulated Panels Market: Estimates & Forecast Trend Analysis

9.1. North America Structural Insulated Panels Market Assessments &

Key Findings

9.1.1.

North America Structural

Insulated Panels Market Introduction

9.1.2.

North America Structural

Insulated Panels Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

9.1.2.1.

By Product Type

9.1.2.2.

By Application

9.1.2.3.

By Skin Material

9.1.2.4.

By End User

9.1.2.5.

By Country

9.1.2.5.1.

The U.S.

9.1.2.5.2.

Canada

10. Europe Structural Insulated Panels Market: Estimates & Forecast

Trend Analysis

10.1.

Europe Structural Insulated

Panels Market Assessments & Key Findings

10.1.1.

Europe Structural Insulated

Panels Market Introduction

10.1.2.

Europe Structural Insulated

Panels Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

10.1.2.1.

By Product Type

10.1.2.2.

By Application

10.1.2.3.

By Skin Material

10.1.2.4.

By End User

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest of Europe

11. Asia Pacific Structural Insulated Panels Market: Estimates &

Forecast Trend Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific Structural

Insulated Panels Market Introduction

11.1.2.

Asia Pacific Structural

Insulated Panels Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

11.1.2.1.

By Product Type

11.1.2.2.

By Application

11.1.2.3.

By Skin Material

11.1.2.4.

By End User

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6.

Rest of Asia Pacific

12. Middle East & Africa Structural Insulated Panels Market:

stimates & Forecast Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa

Structural Insulated Panels Market Introduction

12.1.2.

Middle East & Africa

Structural Insulated Panels Market Size Estimates and Forecast (US$ Million)

(2021 - 2034)

12.1.2.1.

By Product Type

12.1.2.2.

By Application

12.1.2.3.

By Skin Material

12.1.2.4.

By End User

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4.

Rest of MEA

13. Latin America Structural Insulated Panels Market: Estimates &

Forecast Trend Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America Structural

Insulated Panels Market Introduction

13.1.2.

Latin America Structural

Insulated Panels Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

13.1.2.1.

By Product Type

13.1.2.2.

By Application

13.1.2.3.

By Skin Material

13.1.2.4.

By End User

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global Structural Insulated

Panels Market Product Mapping

14.2.

Global Structural Insulated

Panels Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global Structural Insulated

Panels Market Tier Structure Analysis

14.4.

Global Structural Insulated

Panels Market Concentration & Company Market Shares (%) Analysis, 2025

15. Company Profiles

15.1.

Kingspan Group plc

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

*Similar etails would be provided for all

the players mentioned below*

15.2.

Owens Corning

15.3.

PFB Corporation

15.4.

Metl-Span LLC

15.5.

Nucor Corporation

15.6.

Premier Building Systems

15.7.

Structural Panels Inc.

15.8.

Insulspan Inc.

15.9.

R-Control SIPs

15.10.

SIPCO

15.11.

Foard Panel Inc.

15.12.

Extreme Panel Technologies Inc.

15.13.

Alubel S.p.A.

15.14.

Eagle Panel Systems, Inc.

15.15.

Isopan S.p.A.

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables