Telecom Electronic Manufacturing Services Market Size and Forecast (2026 - 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Service Type (Electronics Manufacturing, Engineering & Design Services, Assembly & Integration, Testing & Quality Assurance and Aftermarket Services); By Equipment Type (Network Infrastructure Equipment, Consumer Telecom Devices, Wireless Communication Modules and Optical Communication Equipment); By Deployment Model (Outsourced Manufacturing and In-house Manufacturing); By End-use (Telecom Equipment OEMs, Telecom Operators, Data Center Providers, Consumer Electronics Brands and Others) and Geography

2026-03-12

ICT

Ekta Chaurasia (Team Lead)

Description

Telecom Electronic Manufacturing Services Market Overview

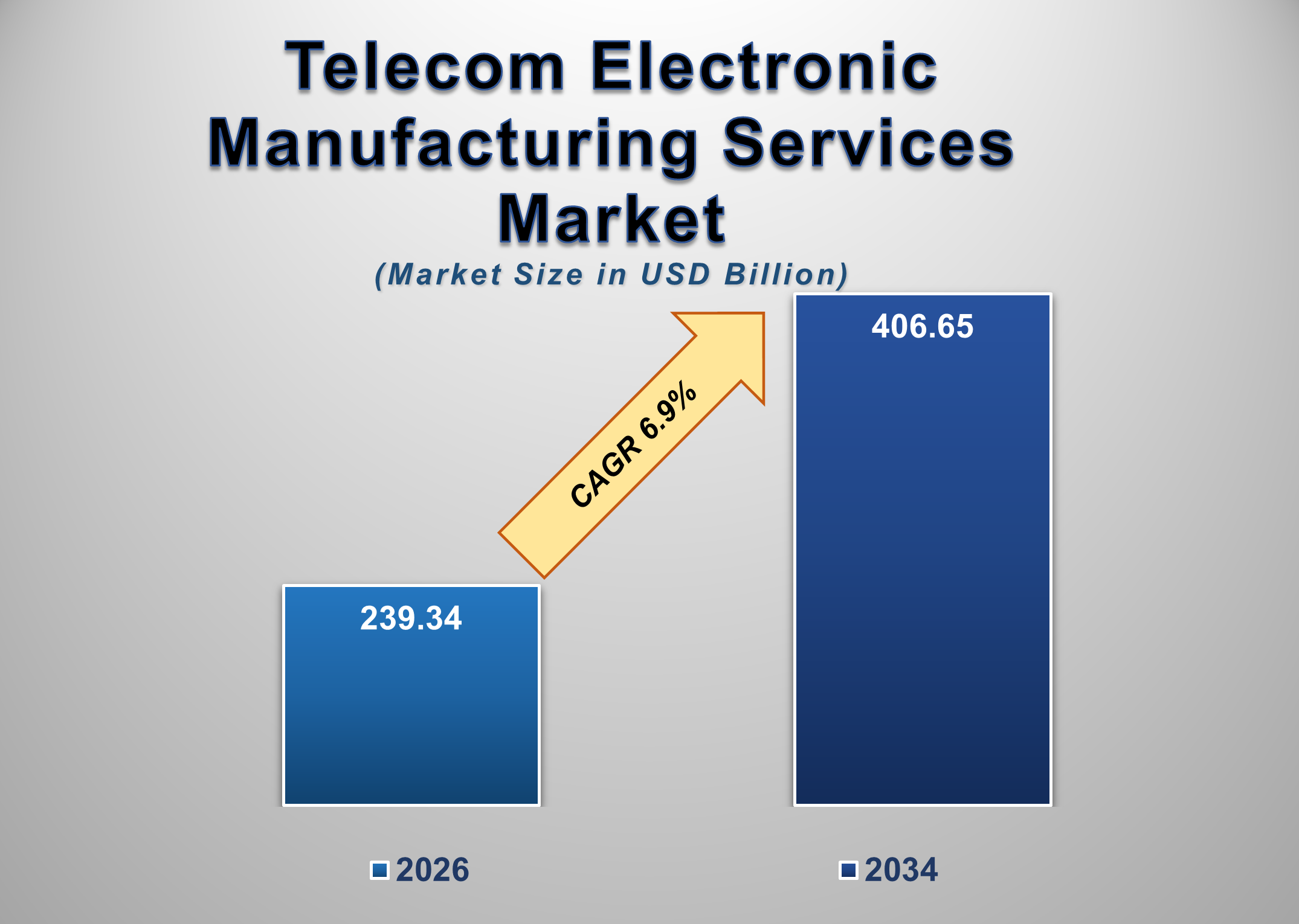

The global Telecom Electronic Manufacturing Services Market is witnessing steady expansion as telecommunications companies increasingly outsource complex electronics manufacturing processes to specialized service providers. The market is valued at USD 239.34 billion in 2026 and is projected to reach USD 406.65 billion by 2034, growing at a CAGR of 6.9%during the forecast period.

Telecom electronic manufacturing services (EMS) refer to outsourced manufacturing solutions provided to telecom equipment manufacturers and technology companies for the production of communication devices, network infrastructure hardware, and electronic modules. EMS providers handle various stages of the product lifecycle, including design support, component sourcing, printed circuit board assembly (PCBA), testing, logistics, and post-production services.

The growing complexity of telecommunications hardware is encouraging original equipment manufacturers (OEMs) to rely on specialized EMS companies with advanced manufacturing capabilities and global supply chain networks. Telecom infrastructure components such as routers, switches, base stations, optical transceivers, and communication modules require precise engineering, high-quality assembly, and rigorous testing procedures to ensure reliable network performance. By outsourcing these processes, telecom OEMs can focus more effectively on innovation, product design, and software development.

The ongoing deployment of next-generation communication technologies, including 5G networks, edge computing infrastructure, and fiber-optic connectivity, is also driving demand for telecom EMS solutions. Telecom equipment production requires highly scalable manufacturing facilities capable of producing large volumes of components while maintaining strict quality standards. EMS providers play a crucial role in meeting these requirements by offering flexible production capacity and global manufacturing expertise.

Additionally, increasing demand for connected devices, mobile communication hardware, and broadband infrastructure is expanding the telecom hardware ecosystem. As the telecommunications sector continues to evolve and global connectivity requirements increase, telecom electronic manufacturing services are expected to remain a critical part of the technology supply chain.

Telecom Electronic Manufacturing Services Market Drivers and Opportunities

Expanding 5G Infrastructure Deployment is anticipated to drive the Telecom Electronic Manufacturing Services market growth

The global rollout of 5G networks is one of the most significant drivers of demand for telecom electronic manufacturing services. Telecommunications operators across the world are investing heavily in upgrading their network infrastructure to support ultra-fast data speeds, low-latency communication, and massive device connectivity. This transition requires the production of advanced telecom hardware components such as base stations, antennas, small cells, routers, and high-capacity switching systems.

Manufacturing these sophisticated components requires specialized expertise in electronics design, precision assembly, and large-scale production. Telecom OEMs increasingly rely on EMS providers to manufacture these devices efficiently while maintaining strict quality and reliability standards. EMS companies possess advanced manufacturing facilities capable of handling high-volume production runs, automated assembly lines, and complex electronic systems integration.

Furthermore, 5G technology requires a denser network architecture compared to previous generations of mobile networks. The deployment of thousands of small cells, distributed antenna systems, and edge computing nodes significantly increases the volume of hardware required to support telecommunications infrastructure. As a result, telecom equipment manufacturers are increasingly outsourcing production to EMS providers to ensure faster manufacturing cycles and efficient supply chain management.

Rising Demand for Fiber Optic and Broadband Infrastructure is accelerating market expansion

The global demand for high-speed internet connectivity continues to grow as digital services, cloud computing, and data-intensive applications become central to modern economies. Governments and private companies are investing heavily in fiber-optic broadband infrastructure to improve network capacity and deliver faster internet services to households and businesses.

The expansion of fiber networks requires large quantities of electronic hardware, including optical transmission equipment, communication modules, signal processing units, and networking devices. Telecom electronic manufacturing service providers play a crucial role in producing these components and ensuring they meet the performance and durability requirements of modern communication systems.

Additionally, the growing number of connected devices, including smartphones, IoT sensors, smart home systems, and industrial automation equipment is increasing network traffic and driving further infrastructure investments. To meet these demands, telecom equipment manufacturers must rapidly scale production of networking hardware, making partnerships with EMS providers increasingly essential.

As the telecommunications sector continues to expand its infrastructure footprint, the demand for high-quality electronics manufacturing services is expected to rise significantly.

Supply Chain Optimization and Global Manufacturing Partnerships create major growth opportunities

One of the most important opportunities within the telecom electronic manufacturing services market lies in the optimization of global electronics supply chains. Telecom hardware production requires a complex network of component suppliers, manufacturing facilities, and distribution channels. EMS providers offer integrated supply chain management solutions that help telecom companies streamline procurement, production, and logistics operations.

Many telecom OEMs are adopting global manufacturing strategies to reduce production costs, improve operational efficiency, and ensure consistent product quality. EMS providers with international manufacturing networks are well positioned to support these strategies by offering geographically diversified production facilities and scalable manufacturing capabilities.

Additionally, increasing geopolitical shifts and supply chain disruptions in recent years have highlighted the importance of resilient and diversified manufacturing ecosystems. Telecom companies are increasingly collaborating with EMS partners to build flexible supply chains that can adapt to changing market conditions.

As telecom infrastructure investments continue to expand worldwide, EMS providers that offer advanced manufacturing technologies, efficient logistics systems, and strong supplier relationships are expected to capture significant growth opportunities in the coming years.

Telecom Electronic Manufacturing Services Market Scope

Telecom Electronic Manufacturing Services Market Report Segmentation Analysis

The global Telecom Electronic Manufacturing Services Market industry analysis is segmented by service type, equipment type, deployment model, end-use, and region.

Electronics Manufacturing dominates the Service Type Segment

By service type, the telecom EMS market is segmented into electronics manufacturing, engineering & design services, assembly & integration, testing & quality assurance, and aftermarket services. Electronics manufacturing accounts for the largest share because telecom hardware production requires extensive printed circuit board assembly, component integration, and system-level manufacturing. Telecom equipment manufacturers rely on EMS providers for large-scale manufacturing operations due to the high complexity and capital requirements involved in telecom electronics production.

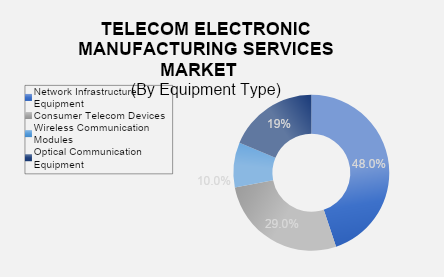

Network Infrastructure Equipment leads the Equipment Type Segment

In terms of equipment type, the market includes network infrastructure equipment, consumer telecom devices, wireless communication modules, and optical communication equipment. Network infrastructure equipment dominates the segment because the deployment of communication networks requires routers, switches, base stations, and signal transmission equipment. These devices form the core hardware of telecommunications systems and represent the largest share of telecom electronics manufacturing demand.

Outsourced Manufacturing holds the largest share of the Deployment Model Segment

Based on deployment model, the market is segmented into outsourced manufacturing and in-house manufacturing. Outsourced manufacturing currently dominates because telecom OEMs increasingly partner with EMS providers to reduce operational costs and improve production efficiency. Outsourcing enables telecom companies to focus on product development and innovation while leveraging the manufacturing expertise of EMS providers.

Telecom Equipment OEMs represent the largest End-use Segment

In terms of end-use, the market is segmented into telecom equipment OEMs, telecom operators, data center providers, consumer electronics brands, and others. Telecom equipment OEMs hold the largest share because they manufacture network devices and infrastructure hardware used by telecommunications operators and enterprises worldwide.

The following segments are part of an in-depth analysis of the global Telecom Electronic Manufacturing Services Market:

Telecom Electronic Manufacturing Services Market Share Analysis by Region

North America is expected to hold a significant share of the global telecom electronic manufacturing services market due to strong investments in advanced telecommunications infrastructure and the presence of major telecom technology companies. The United States leads the regional market because of extensive 5G deployment, large-scale data center expansion, and high demand for networking equipment.

Europe also represents an important market supported by ongoing modernization of telecommunications networks and expansion of fiber broadband infrastructure. Countries such as Germany, the United Kingdom, and France are investing heavily in next-generation telecom infrastructure and digital connectivity programs.

Asia-Pacific is projected to be the fastest-growing region during the forecast period. Rapid expansion of telecommunications networks in countries such as China, India, Japan, and South Korea is driving demand for telecom hardware manufacturing. The region also hosts many global electronics manufacturing hubs, making it a key production center for telecom equipment.

Global Telecom Electronic Manufacturing Services Market Recent Developments News:

o In July 2025, Foxconn expanded its electronics manufacturing facilities to support telecom networking equipment production for global technology companies.

o In May 2025, Flex Ltd. announced a new partnership with a telecom infrastructure manufacturer to produce advanced 5G network hardware modules.

o In March 2025, Jabil Inc. introduced a next-generation telecom electronics manufacturing platform designed to improve efficiency in high-volume network hardware production.

The Global Telecom Electronic Manufacturing Services Market is dominated by a few large companies, such as

● Foxconn Technology Group

● Flex Ltd.

● Jabil Inc.

● Sanmina Corporation

● Celestica Inc.

● Benchmark Electronics Inc.

● Plexus Corporation

● Venture Corporation Limited

● Wistron Corporation

● Pegatron Corporation

● Fabrinet

● New Kinpo Group

● Zollner Elektronik AG

● Compal Electronics

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Telecom Electronic Manufacturing Services Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables