Telecommunications Infrastructure Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (Hardware, Software and Services); By Deployment (Cloud and On-premise); By Infrastructure Type (Wireless Infrastructure, Wired Infrastructure and Data Center Infrastructure); By End-use (Telecom Operators /Network Providers, Internet Service Providers (ISPs), Enterprises & Corporates, Government & Defense, Data Centers & Cloud Service Providers and Others) and Geography

2025-11-03

ICT

Ekta Chaurasia (Team Lead)

Description

Telecommunications Infrastructure Market Overview

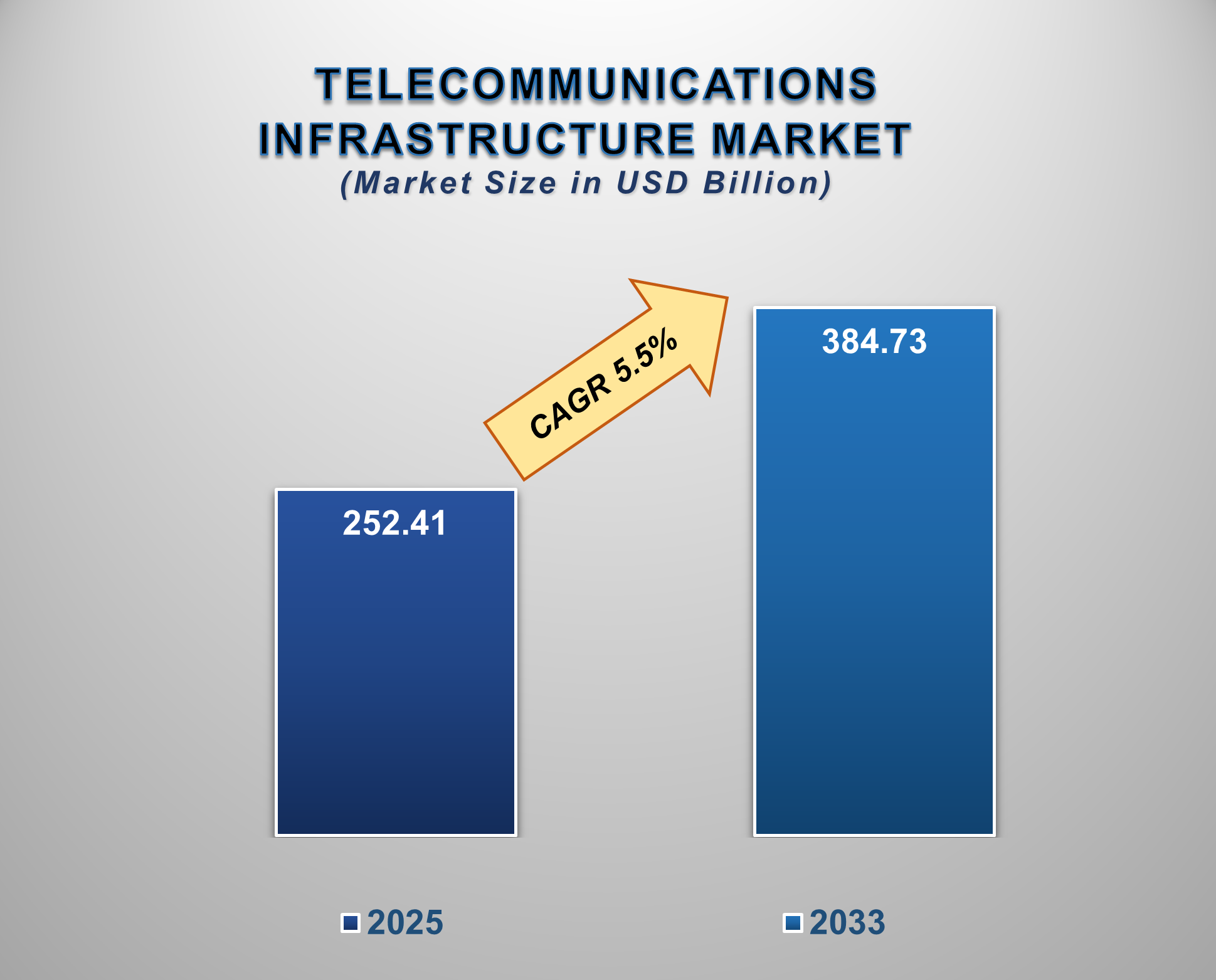

The global Telecommunications Infrastructure Market is experiencing robust growth, driven by a surge in demand for high-speed connectivity and a wave of major technological deployments. The global Telecommunications Infrastructure Market is valued at USD 252.41 billion in 2025 and is projected to reach USD 384.73 billion by 2033, growing at a CAGR of 5.5% during the forecast period. This growth will be supported by the rapid rollout of 5G networks, increasing internet penetration, rising demand for high-speed data services, and investments in fiber-optic and satellite communications.

The telecommunications

infrastructure market comprises all physical and digital systems that enable

the transmission of voice, data, video, and internet services. It includes

wired and wireless networks, core and access infrastructure, data centers, fiber

optic networks, towers, satellites, and support systems such as routers,

switches, and base stations. This infrastructure forms the backbone of global

connectivity, supporting 5G networks, cloud computing, IoT, and digital

transformation initiatives.

Telecommunications

Infrastructure Market Drivers and Opportunities

Rising Data Consumption & Internet Penetration are

anticipated to lift the Telecommunications Infrastructure market growth during

the forecast period

As digital lifestyles, connected

devices, and cloud-based applications become central to modern economies, the

demand for high-speed, reliable, and scalable network infrastructure has surged

dramatically. According to Cisco’s Annual Internet Report, global internet

traffic is projected to exceed 400 exabytes per month by 2030, up from around

350 exabytes per month in 2024, driven by the widespread adoption of video

streaming, gaming, remote work platforms, and IoT devices. Moreover, global

internet penetration has crossed 67% in 2025, with over 5.5 billion active

users, according to the International Telecommunication Union (ITU), compared

to just 4.9 billion in 2021. Emerging economies in Asia-Pacific, Africa, and

Latin America are witnessing particularly strong growth in broadband and mobile

connectivity due to government-led initiatives and private sector investments.

For instance, India’s Digital Bharat initiative aims to extend fiber

connectivity to over 250,000 gram panchayats, while African nations like Kenya

and Nigeria are expanding 4G and 5G coverage to rural areas. This surge in data

demand necessitates the expansion and modernization of fiber optic networks,

mobile towers, small cells, and data centers, as telecom operators and ISPs

race to upgrade capacity and reduce latency. Additionally, the proliferation of

data-intensive technologies such as 4K/8K streaming, virtual reality (VR), and

AI-driven cloud services further amplifies the need for high-performance

backhaul and edge infrastructure. Consequently, the exponential growth in data

consumption and internet access is not only increasing bandwidth requirements

but also catalyzing multi-billion-dollar investments in next-generation

telecommunications infrastructure globally, ensuring the market’s sustained

expansion throughout the forecast period.

Cloud Computing, Edge Computing, and Data Center Expansion a

vital drivers for influencing the growth of the global Telecommunications

Infrastructure market

The rapid growth of cloud

computing, edge computing, and data center expansion is significantly

propelling the Global Telecommunications Infrastructure Market during the

forecast period, as enterprises and consumers increasingly rely on digital

ecosystems that demand ultra-fast, low-latency connectivity. The migration of

enterprise workloads to the cloud, coupled with the proliferation of AI, IoT,

and big data analytics, has led to an unprecedented surge in data traffic

across telecom networks. Global spending on public cloud services is expected

to reach USD 675 billion by 2025, up from USD 563 billion in 2023, with

cloud-based applications accounting for over 60% of enterprise IT workloads.

This shift is driving telecom operators to invest heavily in high-capacity

fiber optic networks, 5G infrastructure, and software-defined networking (SDN)

to support seamless connectivity between cloud servers and end users. At the

same time, edge computing is transforming network architectures by moving data

processing closer to the user, thereby reducing latency and easing core network

congestion. The edge computing market is driven by applications such as

autonomous vehicles, smart factories, and real-time analytics, all of which

rely on distributed network nodes integrated with telecom infrastructure.

Telecom companies such as AT&T, Verizon, Deutsche Telekom, and NTT are

partnering with hyperscalers like AWS, Microsoft Azure, and Google Cloud to

deploy edge data centers and 5G-enabled edge nodes that bring computational

power closer to devices and consumers. Furthermore, the global data center

footprint continues to expand, with over 10,000 operational data centers

worldwide in 2025, fueled by rising demand for cloud storage and content

delivery. Hyperscale operators like Amazon, Meta, and Microsoft are investing

billions in new data center campuses connected by advanced telecom backbones

and submarine fiber cables. This convergence of telecom and data

infrastructure—where cloud providers depend on telecom networks for data

transport and telecom companies leverage cloud and edge technologies for

efficiency—creates a mutually reinforcing cycle of growth. Thus, the increasing

integration of cloud computing, edge processing, and data center expansion is

expected to accelerate capital investments in fiber networks, small cell

deployments, and core network modernization, thereby acting as a major growth

engine for the global telecommunications infrastructure market throughout the

forecast period.

Infrastructure Sharing and Tower Monetization are poised to

create significant opportunities in the global Telecommunications

Infrastructure market

Infrastructure sharing and tower

monetization are emerging as key strategies that are expected to create

lucrative opportunities in the Global Telecommunications Infrastructure Market

during the forecast period. As the rollout of 5G networks and fiber backhaul

accelerates, telecom operators face mounting capital expenditure (CAPEX) and

operational expenditure (OPEX) pressures to expand and maintain network

infrastructure. To optimize costs and maximize returns, operators are

increasingly adopting tower sharing agreements and network infrastructure

sharing models, allowing multiple service providers to utilize the same

physical assets, such as towers, rooftop antennas, and small cells.

Simultaneously, tower monetization, where telecom companies either sell or

lease their passive infrastructure to independent tower management firms, is

gaining momentum. For instance, in 2024, Bharti Infratel merged with Indus

Towers in India, creating one of the world’s largest tower companies, with over

200,000 towers, enabling telecom operators to free up capital for spectrum

acquisition and 5G deployment. In Latin America, companies like America Movil

and Telefónica have leased towers to third-party infrastructure providers,

generating steady revenue streams while reducing maintenance burdens. Such

initiatives not only optimize infrastructure utilization but also attract

private equity and institutional investment into the tower management sector,

making it a financially attractive segment. The trend is further reinforced by

regulatory frameworks in several countries that encourage multi-operator

infrastructure sharing to reduce environmental impact, accelerate broadband

expansion, and enhance rural connectivity. As telecom operators continue to

monetize existing assets and share infrastructure to meet escalating data

demands cost-effectively, this model is expected to significantly reduce

deployment costs, improve network scalability, and boost overall market growth,

creating substantial investment opportunities in the global telecommunications

infrastructure landscape during the forecast period.

Telecommunications Infrastructure Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 252.41 Billion |

|

Market Forecast in 2033 |

USD 384.73 Billion |

|

CAGR % 2025-2033 |

5.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Service Type, Growth Factors and more |

|

Segments Covered |

●

By Component ●

By Deployment ●

By Infrastructure Type ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Telecommunications Infrastructure Market Report Segmentation

Analysis

The global Telecommunications

Infrastructure Market industry analysis is segmented by component, deployment,

type, enterprise size, end-user, and region.

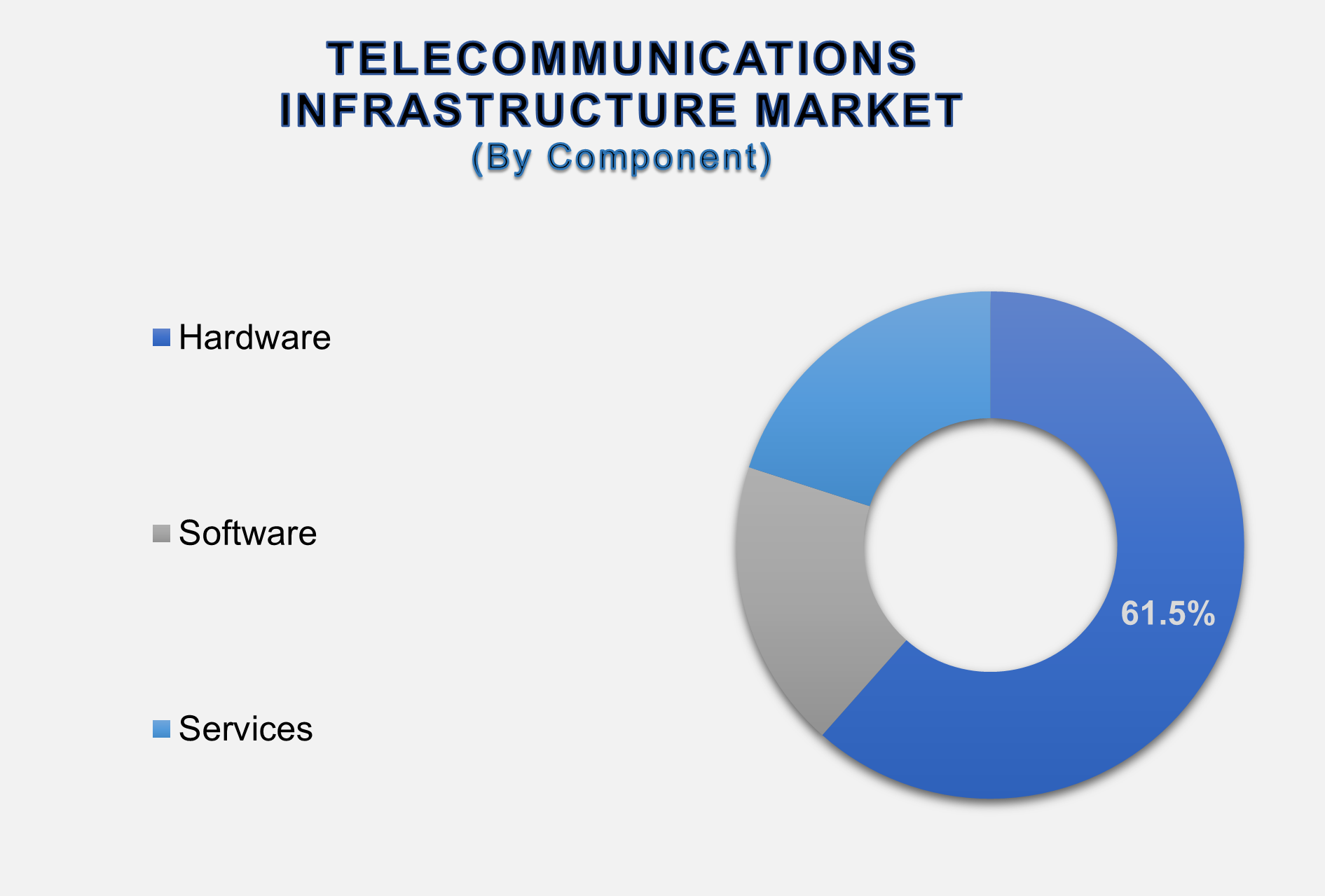

Hardware Dominates the Component Segment

By Component, the Telecommunications Infrastructure market is segmented into Hardware, Software, and Services. The hardware segment dominates due to the high upfront CAPEX required for deploying telecom networks, including 5G towers, fiber optic backhaul, and core network equipment. The rapid rollout of 5G, small cell networks, and fiber expansion in emerging markets necessitates substantial investment in physical infrastructure. Additionally, physical network infrastructure is non-negotiable for telecom operators to provide coverage and capacity. For instance, deploying a single 5G small cell costs between USD 15,000 and 20,000, and nationwide 5G deployments require thousands of such cells, driving hardware expenditure. Furthermore, software is projected to register the highest CAGR during the forecast period due to the rising adoption of cloud-managed networks.

On-premise holds the highest share of the Deployment Segment

Based on deployment, the market

is bifurcated into cloud and on-premise. On-premise infrastructure currently

dominates the market because most telecom operators still rely on physically

installed base stations, core networks, routers, switches, and data center

hardware. Operators prefer on-premise deployment for sensitive network

functions and critical services. Telecom companies have already invested

billions in on-premise hardware and network facilities, especially in North

America, Europe, and Asia-Pacific. Moreover, cloud deployment is projected to

grow at the highest CAGR during the forecast period, because virtualization of

network functions reduces dependency on physical hardware.

Wireless Infrastructure Segment Leads by Infrastructure Type

In terms of infrastructure type,

the Telecommunications Infrastructure market is segmented into Wireless

Infrastructure, Wired Infrastructure, and Data Center Infrastructure. Wireless

infrastructure currently dominates due to the global rollout of 4G/LTE and 5G

networks and the increasing reliance on mobile broadband services. Rapid

urbanization and mobile device proliferation are driving demand for cellular

connectivity, especially in the Asia-Pacific and North America. 5G deployment

requires dense small cell networks and macro towers, significantly increasing

infrastructure spending. Wireless networks are essential for supporting IoT,

connected vehicles, and smart city applications, making them the most critical

segment of telecom infrastructure.

Telecom Operators / Network Providers are a key end-use

In terms of End-use, the

Telecommunications Infrastructure market is segmented into Telecom Operators /

Network Providers, Internet Service Providers (ISPs), Enterprises &

Corporates, Government & Defense, Data Centers & Cloud Service Providers,

and others. Telecom Operators / Network Providers dominate the

Telecommunications Infrastructure market due to continuous investment in 4G/5G

towers, fiber networks, core network upgrades, and small cells. The need to

expand coverage, improve network capacity, and enhance quality of service

drives significant infrastructure spending. Global operators such as AT&T,

Verizon, China Mobile, Vodafone, and Deutsche Telekom collectively deploy and

maintain millions of network assets, accounting for the bulk of infrastructure

expenditure.

The following segments are part of an in-depth analysis of the global

Telecommunications Infrastructure Market:

|

Market Segments |

|

|

By Component

|

●

Hardware o

Transmission

Equipment o

Network Equipment o

Data Center

Equipment ●

Software o

Network Management

Software o

Virtualization

Software o

Software-Defined

Networking Solutions o

Others ●

Services o

Installation &

Consulting Services o

Maintenance &

Support Services o

Managed Network

Services |

|

By Deployment |

●

Cloud ●

On-premise |

|

By Infrastructure Type |

●

Wireless

Infrastructure ●

Wired Infrastructure ●

Data Center

Infrastructure |

|

By End-use |

●

Telecom Operators /

Network Providers ●

Internet Service

Providers (ISPs) ●

Enterprises &

Corporates ●

Government &

Defense ●

Data Centers &

Cloud Service Providers ●

Others |

Telecommunications

Infrastructure Market Share Analysis by Region

The North America region is projected to hold the largest

share of the global Telecommunications Infrastructure Market over the forecast

period.

North America currently holds the

largest share of the global telecommunications infrastructure market,

accounting for a significant portion of total revenue. This dominance is

primarily driven by the presence of major telecom operators such as Verizon, AT&T,

and T-Mobile, coupled with substantial investments in 5G network rollout, fiber

optic expansion, and edge data center deployment. The region benefits from

advanced technological adoption, high smartphone penetration, and strong

digital infrastructure, which collectively support continuous infrastructure

upgrades and expansion. Additionally, government initiatives like the U.S.

Broadband Equity, Access, and Deployment (BEAD) Program are accelerating

network expansion into underserved areas, further consolidating the region’s

market position. Europe holds a moderate market share, supported by mature

telecom networks, early 5G adoption in countries like Germany, the U.K., and

France, and ongoing fiber-to-the-home (FTTH) deployments. However, slower growth

compared to North America is due to market saturation in established urban

centers. Asia-Pacific is the fastest-growing region, expected to register the

highest CAGR during the forecast period. The growth is fueled by rapid

digitalization, rising smartphone penetration, large-scale 5G deployment in

China, India, South Korea, and Japan, and significant investments in rural

connectivity and fiber networks. Emerging markets such as India, Vietnam, and

Indonesia offer huge untapped potential for both wired and wireless telecom

infrastructure.

Global Telecommunications

Infrastructure Market Recent Developments News:

- In July 2025,

Telenor acquired the Norwegian consumer division of GlobalConnect for

approximately $592 million. This acquisition included fiber infrastructure

and around 140,000 fiber customers, strengthening Telenor's presence in

the Norwegian fiber market.

- In June 2025, Verizon, in partnership with Nokia,

secured a contract to construct private 5G networks at the UK's Thames

Freeport. This collaboration aims to support advanced industrial

applications like AI-driven analytics, predictive maintenance, and real-time

logistics coordination.

- In March 2025, Bharti Airtel signed an agreement

with Elon Musk's Starlink to explore bringing satellite internet services

to India, contingent upon government approval. The partnership aims to

bridge the digital divide in India's underserved remote and mountainous

regions.

The Global

Telecommunications Infrastructure Market is dominated by a few large companies,

such as

●

China Mobile

●

Verizon Communications

●

AT&T Inc.

●

Deutsche Telekom

●

Vodafone Group

●

Bharti Airtel

●

Reliance Jio

●

NTT Communications

●

Indus Towers

●

EDOTCO Group

●

ExteNet Systems

●

Pace Digitek

●

Huawei

●

Ericsson

●

Nokia

●

Cisco Systems

●

Qualcomm

●

Broadcom

●

Samsung Electronics

●

NEC Corporation

●

ZTE Corporation

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Telecommunications Infrastructure Market Introduction and

Market Overview

1.1.

Objectives of the Study

1.2.

Global Telecommunications Infrastructure Market Scope and Market

Estimation

1.2.1.Global Telecommunications

Infrastructure Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global Telecommunications

Infrastructure Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Component of

Global Telecommunications Infrastructure Market

1.3.2.Deployment of

Global Telecommunications Infrastructure Market

1.3.3.Infrastructure

Type of Global Telecommunications Infrastructure Market

1.3.4.End-use of Telecommunications

Infrastructure Market

1.3.5.Region of

Global Telecommunications Infrastructure Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Demand Supply Scenario

2.6.

Market Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact

Analysis of Drivers and Restraints

2.7.

Key Products/Brand Analysis

2.8.

Porter’s Five Forces Analysis

2.9.

PEST Analysis

2.10. Key

Regulation

3.

Global

Telecommunications Infrastructure Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Telecommunications Infrastructure Market Estimates & Forecast Trend Analysis, by Component

4.1.

Global Telecommunications Infrastructure Market Revenue (US$ Bn)

Estimates and Forecasts, by Component, 2020 - 2033

4.1.1.Hardware

4.1.1.1.

Transmission Equipment

4.1.1.2.

Network Equipment

4.1.1.3.

Data Center Equipment

4.1.2.Software

4.1.2.1.

Network Management Software

4.1.2.2.

Virtualization Software

4.1.2.3.

Software-Defined Networking Solutions

4.1.2.4.

Others

4.1.3.Services

4.1.3.1.

Installation & Consulting Services

4.1.3.2.

Maintenance & Support Services

4.1.3.3.

Managed Network Services

5. Global Telecommunications Infrastructure Market Estimates & Forecast Trend Analysis, by Deployment

5.1.

Global Telecommunications Infrastructure Market Revenue (US$ Bn)

Estimates and Forecasts, by Deployment, 2020 - 2033

5.1.1.On-Premise

5.1.2.Cloud

6. Global Telecommunications Infrastructure Market Estimates & Forecast Trend Analysis, by Infrastructure Type

6.1.

Global Telecommunications Infrastructure Market Revenue (US$ Bn)

Estimates and Forecasts, by Infrastructure Type, 2020 - 2033

6.1.1.Wireless

Infrastructure

6.1.2.Wired

Infrastructure

6.1.3.Data Center

Infrastructure

7. Global Telecommunications Infrastructure Market Estimates & Forecast Trend Analysis, by End-use

7.1.

Global Telecommunications Infrastructure Market Revenue (US$ Bn)

Estimates and Forecasts, by End-use, 2020 - 2033

7.1.1.Telecom

Operators / Network Providers

7.1.2.Internet

Service Providers (ISPs)

7.1.3.Enterprises

& Corporates

7.1.4.Government

& Defense

7.1.5.Data Centers

& Cloud Service Providers

7.1.6.Others

8.

Global

Telecommunications Infrastructure Market Estimates & Forecast Trend Analysis, by Region

1.1.

Global Telecommunications Infrastructure Market Revenue (US$ Bn)

Estimates and Forecasts, by Region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East

& Africa

1.1.5.Latin America

9.

North America Telecommunications

Infrastructure Market: Estimates &

Forecast Trend Analysis

9.1.

North America Telecommunications Infrastructure Market Assessments

& Key Findings

9.1.1.North America

Telecommunications Infrastructure Market Introduction

9.1.2.North America

Telecommunications Infrastructure Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

9.1.2.1.

By Component

9.1.2.2.

By Deployment

9.1.2.3.

By Infrastructure Type

9.1.2.4.

By End-use

9.1.2.5.

By Country

9.1.2.5.1.

The U.S.

9.1.2.5.2.

Canada

10.

Europe Telecommunications

Infrastructure Market: Estimates &

Forecast Trend Analysis

10.1. Europe

Telecommunications Infrastructure Market Assessments & Key Findings

10.1.1.

Europe Telecommunications Infrastructure Market Introduction

10.1.2.

Europe Telecommunications Infrastructure Market Size Estimates and

Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Component

10.1.2.2.

By Deployment

10.1.2.3.

By Infrastructure Type

10.1.2.4.

By End-use

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Netherland

10.1.2.5.7. Rest of Europe

11.

Asia Pacific Telecommunications

Infrastructure Market: Estimates &

Forecast Trend Analysis

11.1. Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia Pacific Telecommunications Infrastructure Market Introduction

11.1.2.

Asia Pacific Telecommunications Infrastructure Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Component

11.1.2.2.

By Deployment

11.1.2.3.

By Infrastructure Type

11.1.2.4.

By End-use

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6. Rest

of Asia Pacific

12.

Middle East & Africa Telecommunications Infrastructure Market: Estimates & Forecast Trend Analysis

12.1. Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Telecommunications

Infrastructure Market Introduction

12.1.2.

Middle East & Africa Telecommunications

Infrastructure Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Component

12.1.2.2.

By Deployment

12.1.2.3.

By Infrastructure Type

12.1.2.4.

By End-use

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4. Rest of MEA

13.

Latin America Telecommunications

Infrastructure Market: Estimates &

Forecast Trend Analysis

13.1. Latin

America Market Assessments & Key Findings

13.1.1.

Latin America Telecommunications Infrastructure Market

Introduction

13.1.2.

Latin America Telecommunications Infrastructure Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Component

13.1.2.2.

By Deployment

13.1.2.3.

By Infrastructure Type

13.1.2.4.

By End-use

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4. Rest of LATAM

14.

Country Wise Market: Introduction

15. Competition

Landscape

15.1. Global

Telecommunications Infrastructure Market Product Mapping

15.2. Global

Telecommunications Infrastructure Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

15.3. Global

Telecommunications Infrastructure Market Tier Structure Analysis

15.4. Global

Telecommunications Infrastructure Market Concentration & Company Market

Shares (%) Analysis, 2024

16. Company

Profiles

16.1. China Mobile

16.1.1.

Company Overview & Key Stats

16.1.2.

Financial Performance & KPIs

16.1.3.

Product Portfolio

16.1.4.

SWOT Analysis

16.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2.

Verizon Communications

16.3.

AT&T Inc.

16.4.

Deutsche Telekom

16.5.

Vodafone Group

16.6.

Bharti Airtel

16.7.

Reliance Jio

16.8.

NTT Communications

16.9.

Indus Towers

16.10.

EDOTCO Group

16.11.

ExteNet Systems

16.12.

Pace Digitek

16.13.

Huawei

16.14.

Ericsson

16.15.

Nokia

16.16.

Cisco Systems

16.17.

Qualcomm

16.18.

Broadcom

16.19.

Samsung Electronics

16.20.

NEC Corporation

16.21.

ZTE Corporation

16.22.

Other Prominent Players

17.

Research

Methodology

17.1. External

Transportations / Databases

17.2. Internal

Proprietary Database

17.3. Primary

Research

17.4. Secondary

Research

17.5. Assumptions

17.6. Limitations

17.7. Report

FAQs

18.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables