Temperature Sensor Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, Infrared Sensors, Bimetallic Sensors, Others); By End-User (Healthcare, Automotive, Consumer Electronics, Oil & Gas, Energy & Power, Food & Beverage, Aerospace & Defense, Manufacturing); By Connectivity (Wired, Wireless) and Geography

2025-11-04

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Temperature Sensor Market Overview

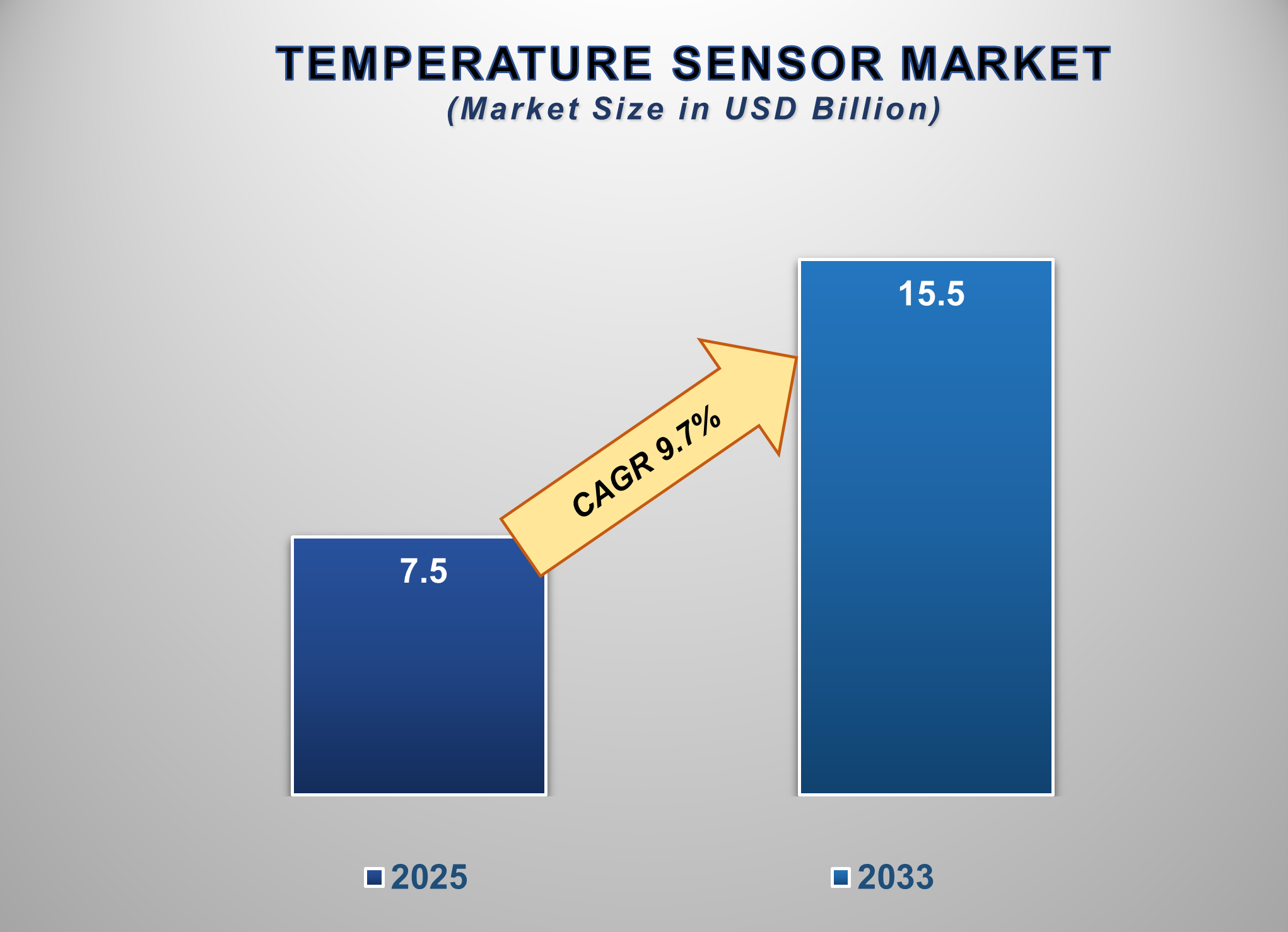

The global Temperature Sensors Market is experiencing robust growth, propelled by the accelerating pace of industrial automation, the proliferation of smart devices, and stringent regulatory requirements for temperature monitoring across critical industries. Valued at approximately USD 7.5 billion in 2025, the market is projected to reach USD 15.5 billion by 2033, growing at a CAGR of 9.7% during the forecast period.

Temperature sensors are critical

components that measure thermal energy to monitor, control, and maintain

specific temperatures in systems and environments. Their applications range

from simple household appliances to complex industrial processes and advanced

medical equipment. The market is characterized by a relentless drive towards

higher accuracy, miniaturization, and digital integration. Key innovations

include the development of smart, wireless sensors with IoT connectivity for

real-time data analytics, the emergence of flexible and printed sensors for

novel applications, and a strong focus on energy-efficient designs. As

industries worldwide embrace Industry 4.0 and smart infrastructure, the demand

for reliable, precise, and interconnected temperature sensing solutions is set

for sustained expansion.

Temperature Sensor Market

Drivers and Opportunities

Proliferation of Industrial Automation and Industry 4.0

A primary driver is the widespread adoption of

industrial automation and the principles of Industry 4.0. Modern manufacturing,

process industries, and smart factories rely on continuous temperature

monitoring to ensure product quality, optimize processes, and enable predictive

maintenance. Temperature sensors are integral to Industrial IoT (IIoT)

ecosystems, providing the critical data needed to prevent equipment failure and

reduce downtime. The opportunity lies in developing advanced sensors with embedded

intelligence, self-diagnostic capabilities, and seamless integration with cloud

platforms for data-driven decision-making.

Stringent Regulatory Standards in Healthcare and Food &

Beverage Industries

Regulatory compliance is a significant market

driver, particularly in sectors like healthcare (for equipment sterilization

and pharmaceutical storage) and food & beverage (for safety and cold chain

logistics). Standards such as HACCP and FDA regulations mandate precise

temperature monitoring and logging. This creates a consistent, recurring demand

for high-accuracy sensors and data-logging solutions. The opportunity for

manufacturers is to offer certified, tamper-proof sensing systems with robust

data management features to help end-users meet compliance effortlessly.

Rapid Growth in Consumer Electronics and Automotive Sectors

The expanding consumer electronics market, with

devices like smartphones, laptops, and wearables, requires compact, low-power

temperature sensors for thermal management and battery monitoring. In the

automotive sector, the rise of electric vehicles (EVs) and advanced

driver-assistance systems (ADAS) has created a surge in demand for sensors to

monitor battery packs, power electronics, and cabin climate. This trend

presents an opportunity for innovation in MEMS-based sensors, which offer the

small size, low cost, and high volume required by these industries.

Temperature Sensor Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 7.5 Billion |

|

Market Forecast in 2033 |

USD 15.5 Billion |

|

CAGR % 2025-2033 |

9.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Service Type, Growth Factors, and more |

|

Segments Covered |

●

By Product Type ●

By Connectivity ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Temperature Sensor Market

Report Segmentation Analysis

The global Temperature Sensors

Market industry analysis is segmented by product type, by end-user, by

connectivity, and by region.

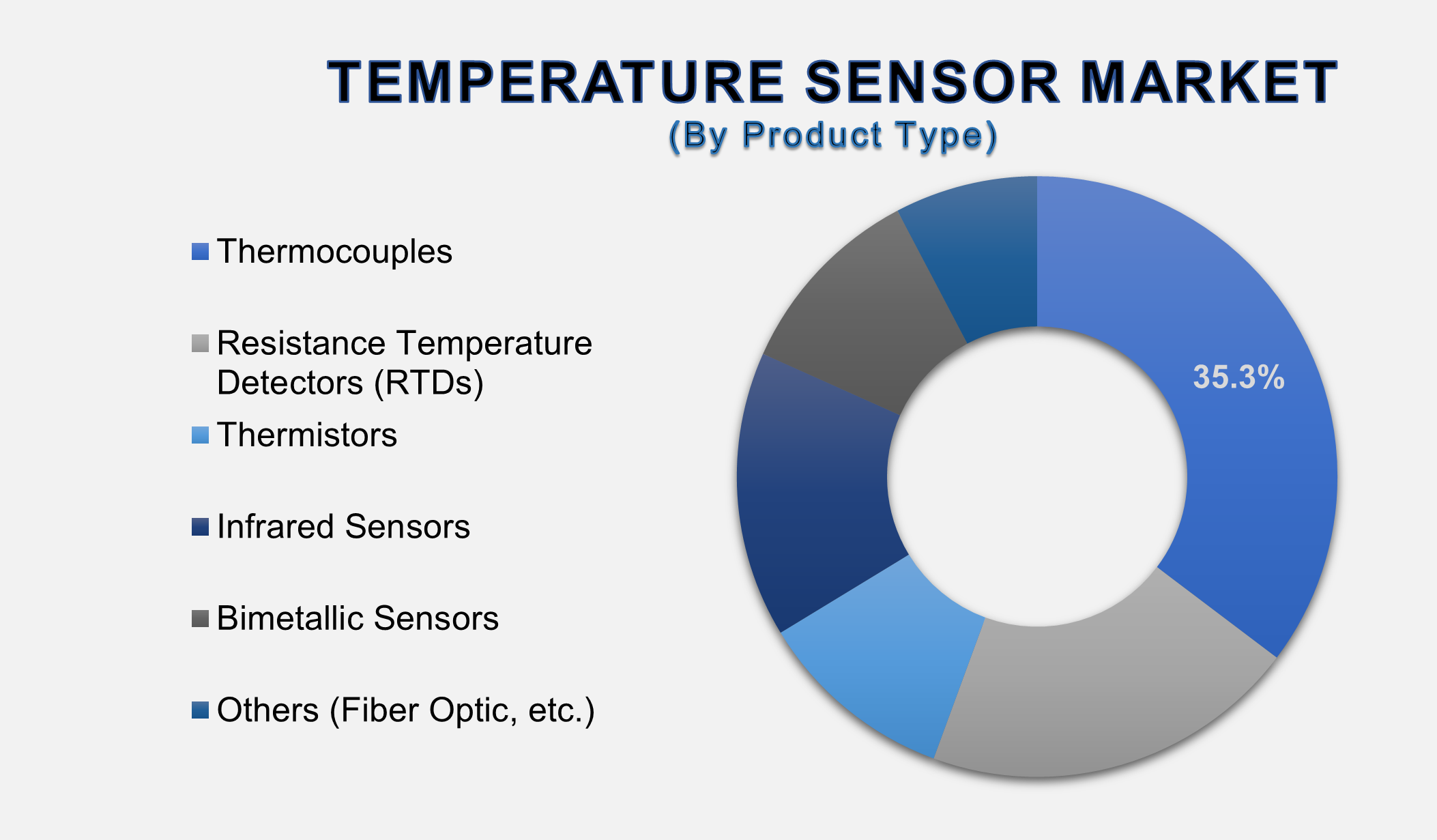

Thermocouples and RTDs Lead by Product Type

Thermocouples and Resistance Temperature

Detectors (RTDs) collectively represent the largest share of the industrial

temperature sensors market. Thermocouples are favored for their wide

temperature range, durability, and low cost, making them suitable for harsh

environments like metal processing and power generation. RTDs are preferred in

applications demanding high accuracy and stability, such as in pharmaceutical

and food processing, due to their precise and repeatable measurements. The

ongoing innovation in these segments focuses on enhancing their robustness and

extending their operational lifespan in extreme conditions.

Infrared and Wireless Sensors are the Fastest-Growing

Segments

The Infrared (IR) temperature sensor segment is

experiencing the highest growth rate, driven by the need for non-contact

temperature measurement. This is critical in applications involving moving

parts, sterile environments, or social distancing, such as in medical scanning,

public spaces, and high-speed manufacturing. Similarly, the wireless

connectivity segment is expanding rapidly, enabled by the growth of IoT.

Wireless sensors reduce installation complexity and cost, allowing for dense

sensor networks in large-scale agricultural, environmental, and industrial

monitoring applications.

Manufacturing and Healthcare are Key End-User Industries

The manufacturing sector is the largest end-user,

consuming a vast number of sensors for process control, machine health

monitoring, and quality assurance. The healthcare sector is another major and

high-growth segment, utilizing sensors in medical devices (e.g., patient

monitors, ventilators), laboratory equipment, and cold chain logistics of

vaccines and biologics. The energy & power and automotive industries also

represent significant and growing markets, driven by smart grid technologies

and the electric vehicle revolution, respectively.

The following segments are part of an in-depth analysis of the global

Temperature Sensor Market:

|

Market Segments |

|

|

By Product Type |

●

Thermocouples ●

Resistance

Temperature Detectors (RTDs) ●

Thermistors ●

Infrared Sensors ●

Bimetallic Sensors ●

Others (Fiber Optic,

etc.) |

|

By Connectivity

|

●

Wired ●

Wireless |

|

By End-user |

●

Healthcare ●

Automotive ●

Consumer Electronics ●

Oil & Gas ●

Energy & Power ●

Food & Beverage ●

Aerospace &

Defense ●

Manufacturing ●

Others |

Temperature Sensor Market

Share Analysis by Region

The Asia-Pacific Region is Dominating the Market

The Asia-Pacific (APAC) region holds a dominant

and rapidly growing position in the temperature sensors market. This is

primarily driven by the massive manufacturing base in countries like China,

Japan, and South Korea, which are global hubs for consumer electronics,

automotive, and industrial equipment production. Government initiatives

promoting industrial automation, such as "Made in China 2025,"

coupled with heavy investments in infrastructure and the rapid adoption of IoT

technologies, are key growth catalysts. The presence of major sensor

manufacturers and a thriving electronics component ecosystem further solidifies

APAC's leadership in both production and consumption.

North America and Europe remain significant

markets, characterized by early adoption of advanced technologies, stringent

regulatory environments, and a strong focus on upgrading existing industrial

infrastructure with smart sensors. These regions are at the forefront of

developing and deploying sensors for high-value applications in aerospace,

defense, and advanced medical devices.

Global Temperature Sensor

Market Recent Developments News:

- In May 2025, TE Connectivity launched a new series

of miniature, high-accuracy RTD sensors designed for precise thermal

management in electric vehicle battery packs.

- In April 2025, Texas Instruments introduced an

ultra-low-power, wireless IoT temperature sensor with an integrated

energy-harvesting interface, targeting building automation and asset

tracking.

- In March 2025, Siemens AG expanded its Siemens

Xcelerator portfolio with a new line of AI-enabled smart temperature

sensors for predictive maintenance in industrial settings.

The Global Temperature Sensor Market is dominated

by a few large companies, such as

●

TE Connectivity Ltd.

●

Texas Instruments

Incorporated

●

Siemens AG

●

Honeywell

International Inc.

●

ABB Ltd.

●

STMicroelectronics

N.V.

●

Amphenol Corporation

●

NXP Semiconductors

N.V.

●

Omega Engineering Inc.

●

Robert Bosch GmbH

●

Microchip Technology

Inc.

●

Analog Devices, Inc.

●

Emerson Electric Co.

●

Danfoss A/S

●

Endress+Hauser Group

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Temperature Sensor Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Temperature Sensor Market Scope and Market Estimation

1.2.1.Global Temperature

Sensor Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Temperature

Sensor Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Product Type of

Global Temperature Sensor Market

1.3.2.Connectivity

of Global Temperature Sensor Market

1.3.3.End-user of

Global Temperature Sensor Market

1.3.4.Region of

Global Temperature Sensor Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Demand Supply Scenario

2.6.

Market Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact

Analysis of Drivers and Restraints

2.7.

Emerging Trends for Temperature Sensor Market

2.8.

Pricing Analysis

2.9.

Key regulations

2.10. Key

Product/Brand Analysis

2.11. Porter’s

Five Forces Analysis

2.12. PEST

Analysis

2.13. Key

Regulation

3.

Global

Temperature Sensor Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Temperature Sensor Market Estimates & Forecast Trend Analysis, by Product Type

4.1.

Global Temperature Sensor Market Revenue (US$ Bn) Estimates and

Forecasts, by Product Type, 2020 - 2033

4.1.1.Thermocouples

4.1.2.Resistance

Temperature Detectors (RTDs)

4.1.3.Thermistors

4.1.4.Infrared

Sensors

4.1.5.Bimetallic

Sensors

4.1.6.Others (Fiber

Optic, etc.)

5. Global Temperature Sensor Market Estimates & Forecast Trend Analysis, by Connectivity

5.1.

Global Temperature Sensor Market Revenue (US$ Bn) Estimates and

Forecasts, by Connectivity, 2020 - 2033

5.1.1.Wired

5.1.2.Wireless

6. Global Temperature Sensor Market Estimates & Forecast Trend Analysis, by End-user

6.1.

Global Temperature Sensor Market Revenue (US$ Bn) Estimates and

Forecasts, by End-user, 2020 - 2033

6.1.1.Healthcare

6.1.2.Automotive

6.1.3.Consumer

Electronics

6.1.4.Oil & Gas

6.1.5.Energy &

Power

6.1.6.Food &

Beverage

6.1.7.Aerospace

& Defense

6.1.8.Manufacturing

6.1.9.Others

7.

Global

Temperature Sensor Market Estimates & Forecast Trend Analysis, by region

7.1.

Global Temperature Sensor Market Revenue (US$ Bn) Estimates and

Forecasts, by region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East

& Africa

7.1.5.Latin America

8.

North America Temperature

Sensor Market: Estimates & Forecast

Trend Analysis

8.1.

North America Temperature Sensor Market Assessments & Key

Findings

8.1.1.North America

Temperature Sensor Market Introduction

8.1.2.North America

Temperature Sensor Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product Type

8.1.2.2.

By Connectivity

8.1.2.3.

By End-user

8.1.2.4.

By Country

8.1.2.4.1.

The U.S.

8.1.2.4.2.

Canada

9.

Europe Temperature

Sensor Market: Estimates & Forecast

Trend Analysis

9.1.

Europe Temperature Sensor Market Assessments & Key Findings

9.1.1.Europe Temperature

Sensor Market Introduction

9.1.2.Europe Temperature

Sensor Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Connectivity

9.1.2.3.

By End-user

9.1.2.4.

By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Netherland

9.1.2.4.7.

Rest

of Europe

10.

Asia Pacific Temperature

Sensor Market: Estimates & Forecast

Trend Analysis

10.1. Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia Pacific Temperature Sensor Market Introduction

10.1.2.

Asia Pacific Temperature Sensor Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Connectivity

10.1.2.3.

By End-user

10.1.2.4.

By Country

10.1.2.4.1.

China

10.1.2.4.2.

Japan

10.1.2.4.3.

India

10.1.2.4.4.

Australia

10.1.2.4.5.

South Korea

10.1.2.4.6. Rest

of Asia Pacific

11.

Middle East & Africa Temperature Sensor Market:

Estimates & Forecast Trend Analysis

11.1. Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Temperature

Sensor Market Introduction

11.1.2.

Middle East & Africa Temperature

Sensor Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Connectivity

11.1.2.3.

By End-user

11.1.2.4.

By Country

11.1.2.4.1.

UAE

11.1.2.4.2.

Saudi Arabia

11.1.2.4.3.

South Africa

11.1.2.4.4. Rest of MEA

12.

Latin America Temperature

Sensor Market: Estimates & Forecast

Trend Analysis

12.1. Latin

America Market Assessments & Key Findings

12.1.1.

Latin America Temperature Sensor Market Introduction

12.1.2.

Latin America Temperature Sensor Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Connectivity

12.1.2.3.

By End-user

12.1.2.4.

By Country

12.1.2.4.1.

Brazil

12.1.2.4.2.

Mexico

12.1.2.4.3.

Argentina

12.1.2.4.4. Rest of LATAM

13.

Country Wise Market: Introduction

14. Competition

Landscape

14.1. Global

Temperature Sensor Market Product Mapping

14.2. Global

Temperature Sensor Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3. Global

Temperature Sensor Market Tier Structure Analysis

14.4. Global

Temperature Sensor Market Concentration & Company Market Shares (%)

Analysis, 2024

15. Company

Profiles

15.1.

TE Connectivity Ltd.

15.1.1.

Company Overview & Key Stats

15.1.2.

Financial Performance & KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2.

Texas Instruments Incorporated

15.3.

Siemens AG

15.4.

Honeywell International Inc.

15.5.

ABB Ltd.

15.6.

STMicroelectronics N.V.

15.7.

Amphenol Corporation

15.8.

NXP Semiconductors N.V.

15.9.

Omega Engineering Inc.

15.10.

Robert Bosch GmbH

15.11.

Microchip Technology Inc.

15.12.

Analog Devices, Inc.

15.13.

Emerson Electric Co.

15.14.

Danfoss A/S

15.15.

Endress+Hauser Group

15.16.

Other Prominent Players

16.

Research

Methodology

16.1. External

Transportations / Databases

16.2. Internal

Proprietary Database

16.3. Primary

Research

16.4. Secondary

Research

16.5. Assumptions

16.6. Limitations

16.7. Report

FAQs

17.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables