Tethered Caps Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Material (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Others), By Application (Beverages, Pharmaceuticals, Others), and Geography

2026-02-25

Chemicals & Materials

Description

Tethered

Caps Market Overview

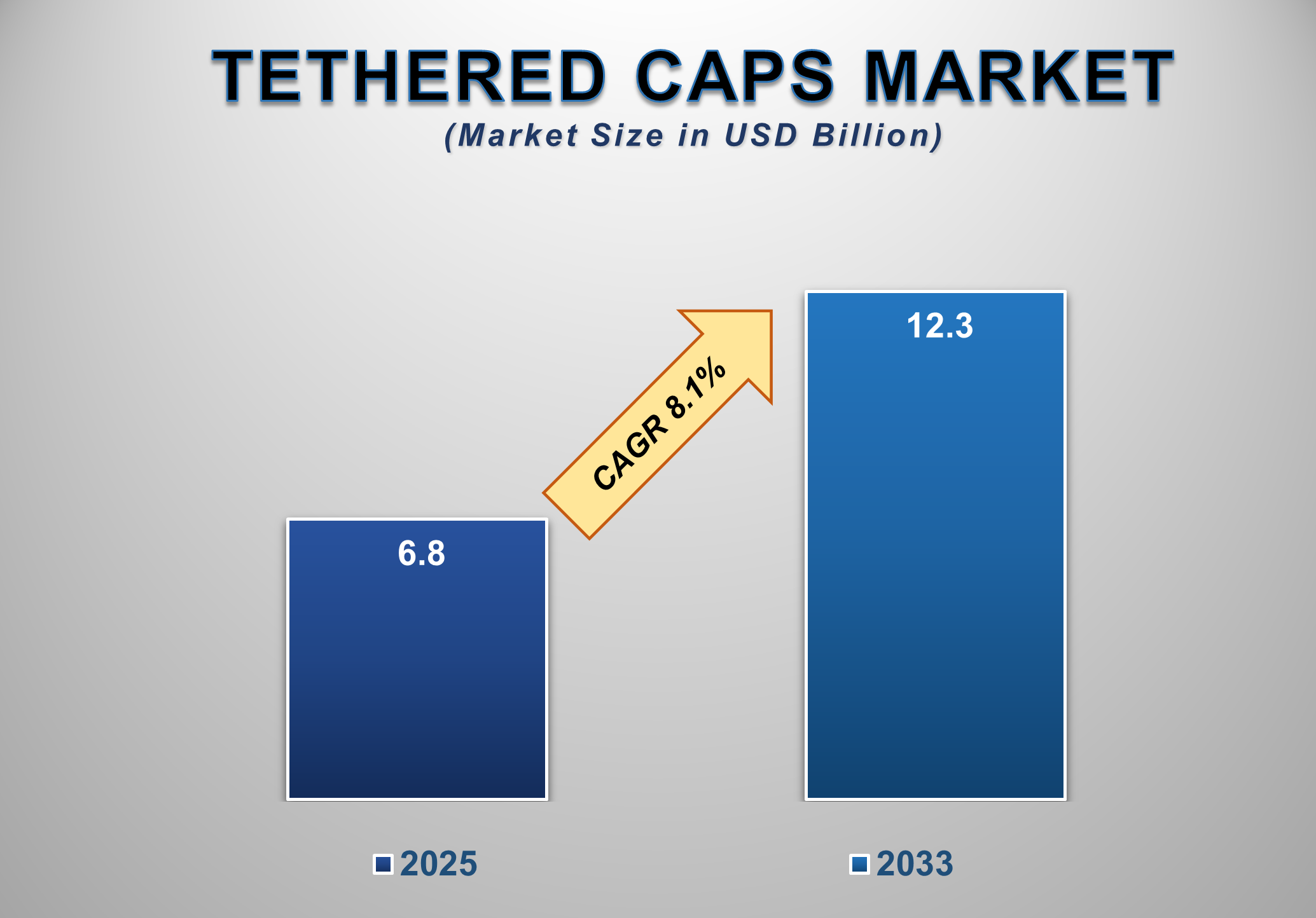

The global tethered caps market was valued at USD 6.8 billion in 2025 and is projected to reach USD 12.3 billion by 2033, registering a CAGR of 8.1% during the forecast period. Market growth is primarily driven by rising regulatory pressure to reduce plastic waste, increasing adoption of sustainable packaging solutions, and strong demand from the beverages industry. Tethered caps, which remain attached to containers after opening, are increasingly being adopted as an effective solution to prevent cap littering and improve recyclability.

Governments and regulatory

authorities across multiple regions have introduced stringent packaging waste

directives, particularly targeting single-use plastics. In response, beverage

manufacturers and packaging companies are rapidly transitioning toward tethered

closures to comply with environmental regulations and enhance sustainability

credentials. The implementation of the European Union’s Single-Use Plastics

Directive has had a ripple effect globally, encouraging brand owners to

proactively adopt tethered cap designs even in regions where regulations are

still evolving. Additionally, growing consumer awareness regarding plastic

pollution and recycling practices is accelerating the shift toward

environmentally responsible packaging formats. Major beverage brands are

increasingly positioning tethered caps as part of broader sustainability

initiatives, reinforcing their market acceptance. Technological advancements in

cap design, material optimization, and manufacturing efficiency have further

improved product performance, ease of use, and cost competitiveness. As

sustainability becomes a core pillar of packaging innovation, the tethered caps

market is expected to witness sustained growth through 2033.

Tethered Caps Market

Drivers and Opportunities

Stringent Environmental

Regulations Are Driving Market Growth

The increasing implementation of

environmental regulations aimed at reducing plastic waste is a key driver of

the tethered caps market. Regulatory bodies across Europe, North America, and

parts of the Asia Pacific are enforcing measures to minimize plastic leakage

into the environment, particularly from beverage packaging. Tethered caps

directly address this challenge by ensuring that caps remain attached to

containers throughout the product lifecycle, significantly reducing the risk of

littering. The European Union’s mandate requiring tethered caps on beverage

containers has played a pivotal role in accelerating global adoption.

Multinational beverage companies operating across regions are standardizing

packaging formats to maintain regulatory compliance and operational efficiency.

This has led to widespread investments in tethered cap technologies across

global production facilities. Furthermore, extended producer responsibility

(EPR) frameworks are pushing manufacturers to take greater accountability for packaging

waste. Tethered caps support EPR goals by improving collection rates and

recycling outcomes. As additional countries introduce similar waste reduction

policies, regulatory compliance will remain a strong catalyst for market

expansion.

Rising Beverage

Consumption and Sustainable Packaging Demand Are Fueling Adoption

The growing consumption of

bottled beverages, including water, carbonated drinks, juices, and functional

beverages, is another major driver supporting tethered caps demand. As beverage

volumes rise globally, particularly in urbanizing and developing regions, the

environmental footprint of packaging has become a critical concern for both

regulators and brand owners. Beverage manufacturers are increasingly

integrating sustainability into their brand strategies, viewing packaging

innovation as a differentiating factor. Tethered caps not only reduce

environmental impact but also enhance consumer convenience by preventing cap

loss and improving on-the-go usability. These functional benefits have

contributed to positive consumer perception and broader acceptance. In

addition, leading packaging suppliers have optimized tethered cap designs to

ensure compatibility with high-speed filling lines, minimizing disruption to

existing manufacturing processes. This has lowered adoption barriers and

encouraged faster transition across beverage packaging formats. As sustainable

packaging becomes a non-negotiable requirement for beverage brands, tethered

caps are expected to see continued demand growth.

Expansion into

Pharmaceuticals and Emerging Markets Presents Key Opportunities

Beyond beverages, the expansion of tethered caps into pharmaceutical and healthcare packaging presents a significant growth opportunity. Pharmaceutical packaging increasingly prioritizes safety, tamper evidence, and controlled disposal, making tethered caps an attractive solution for liquid medicines, syrups, and diagnostic products. Emerging markets in the Asia Pacific, Latin America, and the Middle East & Africa also represent untapped growth potential. While regulatory enforcement in these regions is still developing, growing awareness of plastic pollution and increasing alignment with global sustainability standards are driving gradual adoption. Multinational packaging suppliers are actively introducing tethered cap solutions tailored to local market needs and cost structures. Moreover, ongoing innovation in bio-based and recyclable materials is expected to enhance the sustainability profile of tethered caps further. As material science advances and production costs decline, tethered caps are likely to penetrate a wider range of applications, creating long-term growth opportunities.

Tethered Caps Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 6.8 Billion |

|

Market Forecast in 2033 |

USD 12.3 Billion |

|

CAGR % 2025-2033 |

8.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company

Share, Company Heatmap, Company Production Capacity, Growth Factors, and more |

|

Segments Covered |

●

By Material ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Saudi Arabia 17)

UAE 18)

South Africa

|

Tethered Caps Market

Report Segmentation Analysis

The Global Tethered Caps Market

Industry Analysis Is Segmented Into By Material, By Application, And By Region.

Polyethylene (PE) Segment

Is Expected to Dominate the Tethered Caps Market During the Forecast Period

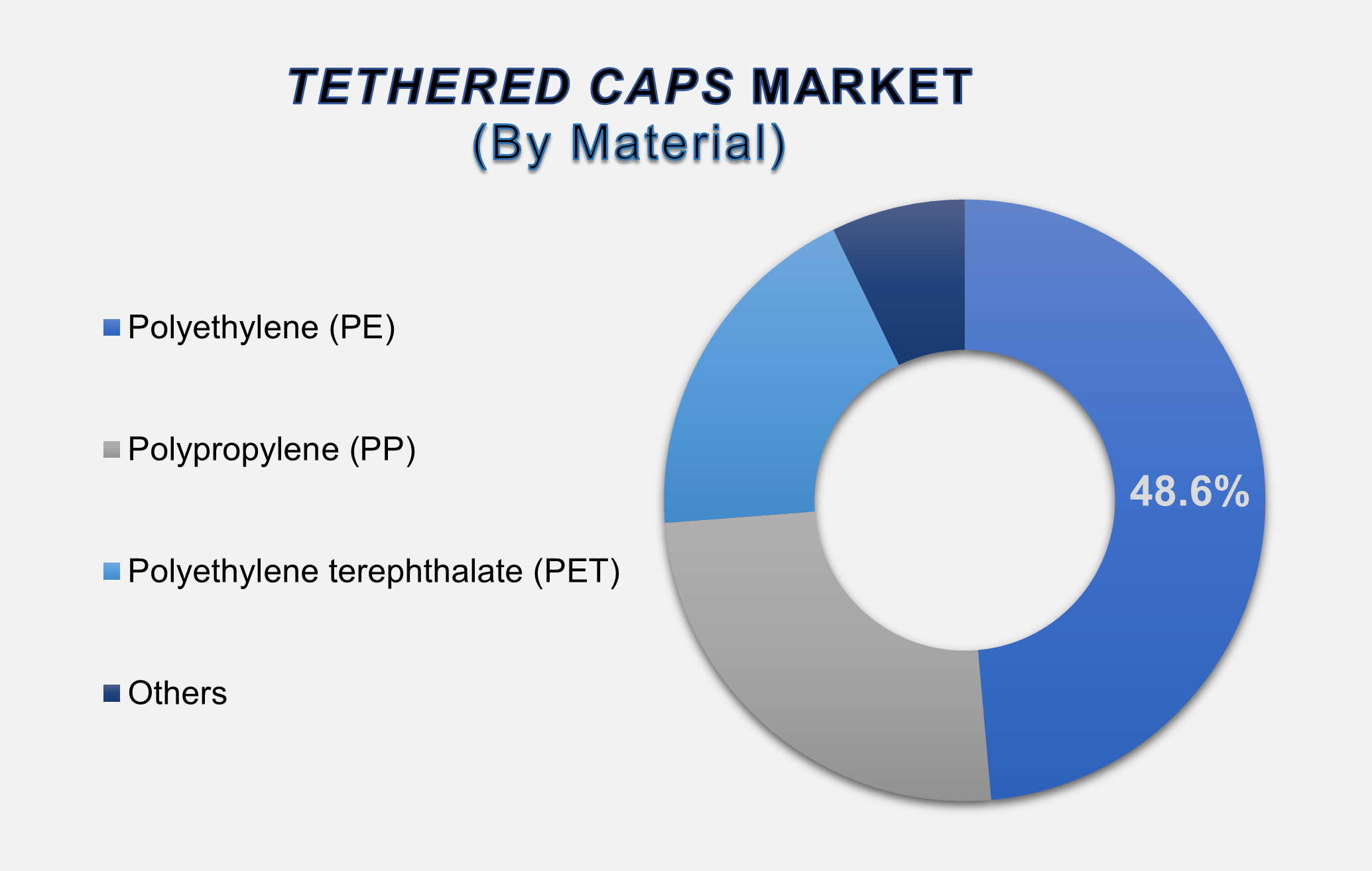

The polyethylene (PE) segment accounted for approximately 48.6% of the global tethered caps market, making it the leading material segment. PE is widely preferred due to its flexibility, durability, chemical resistance, and cost-effectiveness. Its compatibility with existing recycling infrastructure further enhances its attractiveness for sustainable packaging applications. PE tethered caps are extensively used in beverage packaging, where lightweight design and ease of molding are critical. The material allows for complex hinge and tether designs without compromising opening performance or user comfort. Additionally, PE’s widespread availability and processing efficiency make it the material of choice for high-volume production. As packaging manufacturers continue to prioritize recyclability and regulatory compliance, PE is expected to maintain its dominant position throughout the forecast period.

Beverages Application Is

Expected to Lead Market Demand Through 2033

The beverages segment represents

the largest application area for tethered caps, driven by regulatory mandates

and the high volume of bottled beverage consumption globally. Water bottles,

carbonated soft drinks, and ready-to-drink beverages are primary adopters of

tethered cap solutions. Beverage brands are increasingly redesigning packaging

portfolios to align with sustainability commitments, and tethered caps have

become a standard requirement in many markets. Their ability to reduce cap

loss, improve recycling efficiency, and enhance consumer convenience has

strengthened their adoption. With beverage packaging accounting for the

majority of tethered cap installations, this segment is expected to continue

leading market demand during the forecast period.

The following segments are

part of an in-depth analysis of the global Tethered Caps market:

|

Market

Segments |

|

|

By Material |

●

Polyethylene (PE) ●

Polypropylene (PP) ●

Polyethylene

terephthalate (PET) ●

Others |

|

By Application |

●

Beverages ●

Pharmaceuticals ●

Others |

Tethered Caps Market

Share Analysis By Region

North America is

projected to hold the largest share of the global tethered caps market over the

forecast period.

North America accounted for

approximately 47.4% of the global tethered caps market in 2025, making it the

largest regional market. The region benefits from early adoption of sustainable

packaging practices, a strong presence of leading beverage brands, and

proactive regulatory initiatives aimed at reducing plastic waste. Packaging

manufacturers in North America have invested heavily in tethered cap

technologies to align with both current and anticipated regulations. High

consumer awareness regarding environmental sustainability further supports

market growth, reinforcing North America’s leadership position.

Asia Pacific is expected to

register the highest CAGR during the forecast period, driven by rapid growth in

beverage consumption, expanding urban populations, and increasing regulatory

alignment with global sustainability standards. Countries such as China, India,

and Southeast Asian nations are witnessing rising bottled beverage demand,

prompting packaging innovation. While tethered cap adoption is still in the

early stages, growing environmental awareness and multinational brand influence

are accelerating market penetration. As infrastructure and regulatory

frameworks mature, the Asia Pacific is poised to become the fastest-growing

regional market.

Tethered Caps Market Competition Landscape

Analysis

The tethered caps market is

moderately competitive, with global packaging manufacturers and closure

specialists focusing on innovation, regulatory compliance, and large-scale

production capabilities. Companies compete on material expertise, design flexibility,

sustainability credentials, and long-term supply agreements with beverage and

pharmaceutical brands.

Global Tethered Caps Market Recent Developments

News:

●

In January 2024 –

Tetra Pak and Valio introduced the first tethered cap made with certified

recycled polymers in Northern Europe. The C38 Pro tethered cap is designed to

remain attached to the packaging, supporting waste reduction and sustainable

packaging goals.

●

In December 2023 –

TriMas Packaging expanded its tethered closure portfolio with a new 38mm sports

drink tethered cap developed for Coca-Cola. Scheduled for launch and production

scale-up in mid-2024, the closure is designed for major beverage applications.

●

In January 2023 –

Berry Global and Coca-Cola partnered to introduce tethered closures in European

markets. Berry's design features a tamper-evident band that, when broken, keeps

the cap attached to the bottle for convenient drinking and re-closing, aligning

with evolving packaging regulations.

●

In November 2022 –

Landliebe launched the first combiSwift closure with a tethered cap for SIG's

carton packages. The launch came well ahead of the EU Single-Use Plastics

Directive deadline, requiring caps to remain

attached to beverage containers to facilitate recycling.

●

In September 2021 –

Elopak introduced the Pure-TwistFlip, a tethered cap option for its Pure-Pak

cartons. The closure remains attached throughout the package lifecycle, aiming

to reduce marine littering by ensuring proper cap disposal alongside the carton.

The Global Tethered Caps Market

is dominated by a few large companies, such as

●

Berry Global

●

AptarGroup Inc.

●

Closure Systems International

●

Silgan Closures

●

BERICAP

●

Tetra Pak

●

ALPLA Group

●

Huhtamaki

●

SACMI

●

Guala Closures

●

TriMas

●

Corvaglia

●

KHS GmbH

●

Resilux

●

Cap & Seal

●

Baralan

●

MJS Packaging

●

Aller Closures

●

Caplugs

●

HEUFT

● Others

Frequently Asked Questions

1. Global Tethered Caps

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Tethered Caps Market Scope and Market Estimation

1.2.1.Global Tethered Caps Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Tethered Caps

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Material of Global Tethered

Caps Market

1.3.2.Application of Global Tethered

Caps Market

1.3.3.Region of Global Tethered

Caps Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Tethered Caps Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Tethered Caps Market Estimates

& Forecast Trend Analysis, by Material

4.1.

Global

Tethered Caps Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020

- 2033

4.1.1.Polyethylene (PE)

4.1.2.Polypropylene (PP)

4.1.3.Polyethylene terephthalate

(PET)

4.1.4.Others

5. Global

Tethered Caps Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Tethered Caps Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Beverages

5.1.2.Pharmaceuticals

5.1.3.Others

6. Global

Tethered Caps Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Tethered Caps Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Tethered

Caps Market: Estimates & Forecast

Trend Analysis

7.1.

North

America Tethered Caps Market Assessments & Key Findings

7.1.1.North America Tethered

Caps Market Introduction

7.1.2.North America Tethered

Caps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Material

7.1.2.2. By Application

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Tethered

Caps Market: Estimates & Forecast

Trend Analysis

8.1.

Europe

Tethered Caps Market Assessments & Key Findings

8.1.1.Europe Tethered Caps

Market Introduction

8.1.2.Europe Tethered Caps

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Material

8.1.2.2. By Application

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Tethered

Caps Market: Estimates & Forecast

Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Tethered Caps

Market Introduction

9.1.2.Asia Pacific Tethered Caps

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Material

9.1.2.2. By Application

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Tethered

Caps Market: Estimates & Forecast

Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Tethered Caps Market Introduction

10.1.2.

Middle East & Africa Tethered Caps Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Material

10.1.2.2. By Application

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Tethered Caps Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Tethered Caps Market Introduction

11.1.2.

Latin

America Tethered Caps Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Material

11.1.2.2. By Application

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Tethered Caps Market Product Mapping

13.2.

Global

Tethered Caps Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

13.3.

Global

Tethered Caps Market Tier Structure Analysis

13.4.

Global

Tethered Caps Market Concentration & Company Market Shares (%) Analysis,

2024

14.

Company

Profiles

14.1.

Berry Global

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. AptarGroup

Inc.

14.3. Closure

Systems International

14.4. Silgan

Closures

14.5. BERICAP

14.6. Tetra

Pak

14.7. ALPLA

Group

14.8. Huhtamaki

14.9. SACMI

14.10. Guala

Closures

14.11. TriMas

14.12. Corvaglia

14.13. KHS GmbH

14.14. Resilux

14.15. Cap

& Seal

14.16. Baralan

14.17. MJS

Packaging

14.18. Aller

Closures

14.19. Caplugs

14.20. HEUFT

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables