Textile Colorant Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Source (Natural, Synthetic), By Type (Azoic Dyes, Direct Dyes, Basic Dyes, Disperse Dyes, Reactive Dyes, Sulfur Dyes, VAT Dyes, Others), By Application (Clothing, Technical Textiles, Home Textiles & Carpets, Automotive Textiles), and Geography

2026-02-02

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Textile Colorant Market Overview

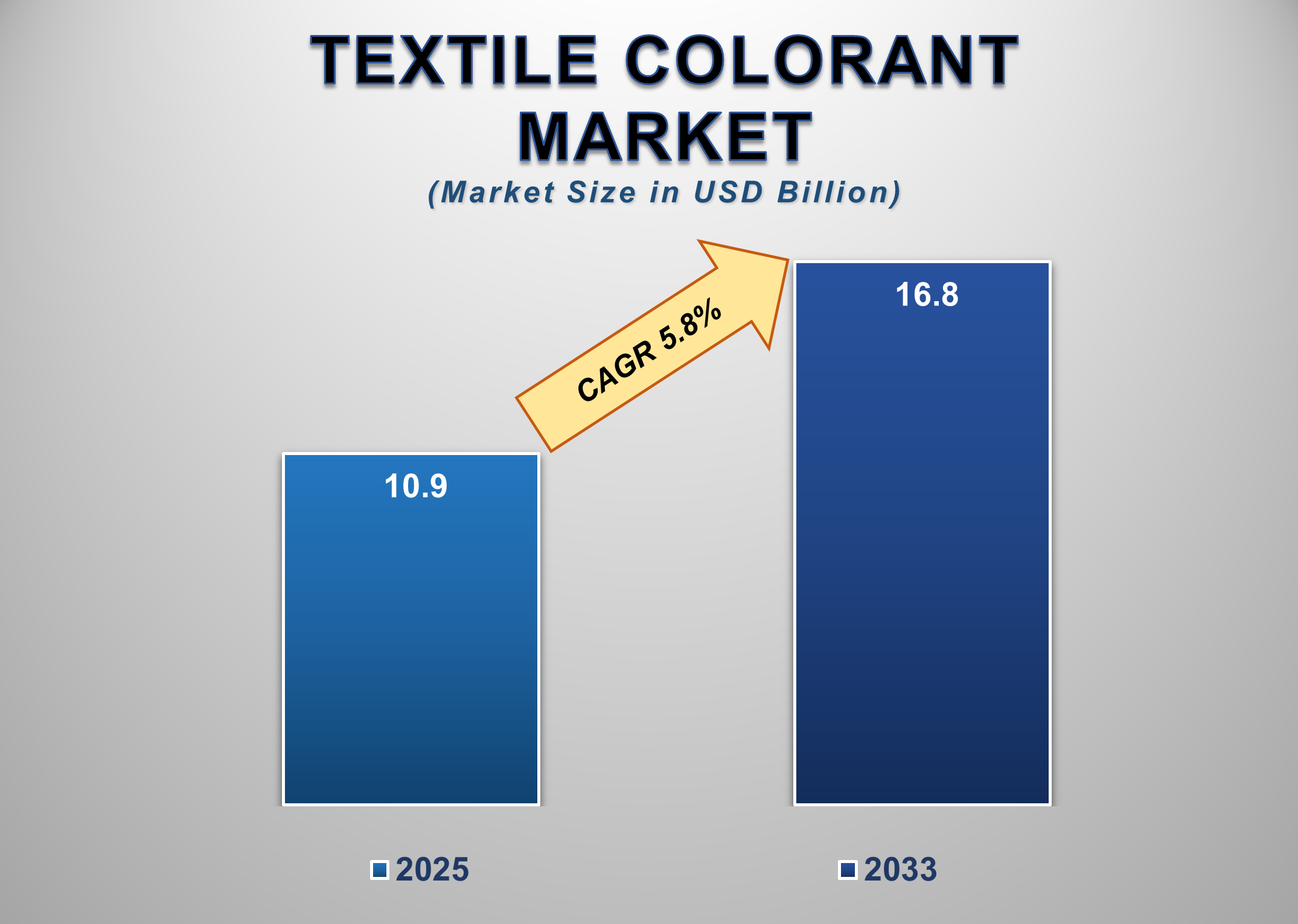

The global Textile Colorant Market was valued at USD 10.9 billion in 2025 and is projected to reach USD 16.8 billion by 2033, expanding at a CAGR of 5.8% during the forecast period. Textile colorants, including dyes and pigments, play a foundational role in defining the visual appeal, branding, and functional performance of textile products across apparel, home furnishings, industrial fabrics, and automotive interiors. As global textile and apparel production continues to expand, particularly in Asia-Pacific manufacturing hubs, demand for reliable, high-performance, and sustainable colorants is increasing steadily.

The market is undergoing a

structural transition driven by environmental regulations, consumer preference

for eco-friendly fabrics, and the fashion industry’s push toward sustainable

sourcing. Natural colorants are gaining significant traction, accounting for

34.8% of total market share, as brands shift away from petroleum-based dyes

toward biodegradable, non-toxic alternatives. Meanwhile, technological

advancements in synthetic dyes, such as reactive and disperse dyes, are

improving colorfastness, wash resistance, and compatibility with modern fibers

like polyester and blended textiles.

Textile Colorant Market

Drivers and Opportunities

Rising

Global Textile and Apparel Production Is Driving Textile Colorant Demand

Expanding global demand for apparel, home furnishings, and

technical textiles is a key driver of the textile colorant market. Rapid

urbanization, rising disposable income, and fast-fashion business models are

driving higher volumes of textile production, particularly in emerging

economies. Every garment, upholstery fabric, or industrial textile requires

multiple stages of dyeing and finishing, making colorants an indispensable

component of the textile value chain. Asia-Pacific continues to lead global textile

manufacturing, with countries such as China, India, Bangladesh, and Vietnam

serving as major suppliers to international fashion brands. As production

volumes increase, so does the consumption of dyes and pigments across spinning,

weaving, knitting, and finishing processes. Additionally, the growth of

technical textiles used in automotive, construction, medical, and industrial

applications is expanding the market for high-performance colorants that

deliver durability, chemical resistance, and UV stability.

Moreover, fashion cycles are becoming shorter, driving higher

color variety and faster dyeing throughput. This is boosting demand for

versatile dye systems such as reactive, disperse, and direct dyes that can

deliver consistent shades across large production runs. As global textile

exports continue to grow, the need for advanced, cost-effective, and scalable

colorant solutions is accelerating market expansion.

Shift Toward Sustainable and Eco-Friendly Dyeing Is Reshaping

the Market

Environmental concerns and regulatory pressure are transforming

the textile colorant industry. Conventional synthetic dyes often generate

wastewater containing toxic chemicals, heavy metals, and non-biodegradable

compounds, creating major environmental and compliance challenges for textile

producers. Governments across Europe, North America, and increasingly Asia are

enforcing stricter effluent treatment and chemical usage standards, pushing

manufacturers to adopt greener dyeing solutions.

This regulatory shift is driving strong growth in natural

colorants derived from plants, minerals, and bio-based sources. With natural

colorants accounting for 34.8% of the market, fashion brands are increasingly

marketing naturally dyed garments as premium, sustainable, and skin-friendly

products. At the same time, chemical companies are investing in low-impact

synthetic dyes, including high-exhaust reactive dyes and water-saving dyeing

technologies that reduce chemical and water consumption. Large apparel brands

are also setting sustainability targets that require suppliers to use

certified, low-toxicity colorants. This is reshaping procurement strategies and

accelerating the adoption of eco-compliant dye portfolios. As environmental

compliance becomes a competitive requirement rather than an option, sustainable

colorant solutions are becoming a powerful growth driver for the industry.

Digital Textile Printing and Fiber Innovation Are Creating

High-Value Opportunities

The expansion of digital textile printing and advanced fiber

technologies presents a major growth opportunity for the textile colorant

market. Digital printing allows manufacturers to apply precise, high-resolution

colors directly onto fabrics, enabling customization, shorter production runs,

and reduced waste. This shift is creating strong demand for specialized inks

and dye formulations optimized for digital printing platforms. At the same

time, the textile industry is rapidly adopting new fibers such as recycled

polyester, bio-based fabrics, and high-performance technical textiles. These

materials require advanced colorants that offer strong bonding, color vibrancy,

and durability. Traditional dye systems are often incompatible with modern

fibers, creating opportunities for innovative dye chemistry and application

methods. As fashion brands move toward on-demand manufacturing and mass

customization, colorant suppliers that can deliver digitally compatible,

sustainable, and high-performance solutions will gain a competitive edge. This

evolution is expected to significantly increase the value per unit of textile

colorants, driving premiumization and profitability across the market.

Textile Colorant Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 10.9 Billion |

|

Market Forecast in 2033 |

USD 16.8 Billion |

|

CAGR % 2025-2033 |

5.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth factors,

and more |

|

Segments Covered |

●

Source, Type,

Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Textile Colorant Market

Report Segmentation Analysis

The Global Textile Colorant

Market Industry Analysis is segmented by Source, Type, Application, and Region.

Natural Segment Accounted for Largest Market Share in the

Global Textile Colorant Market

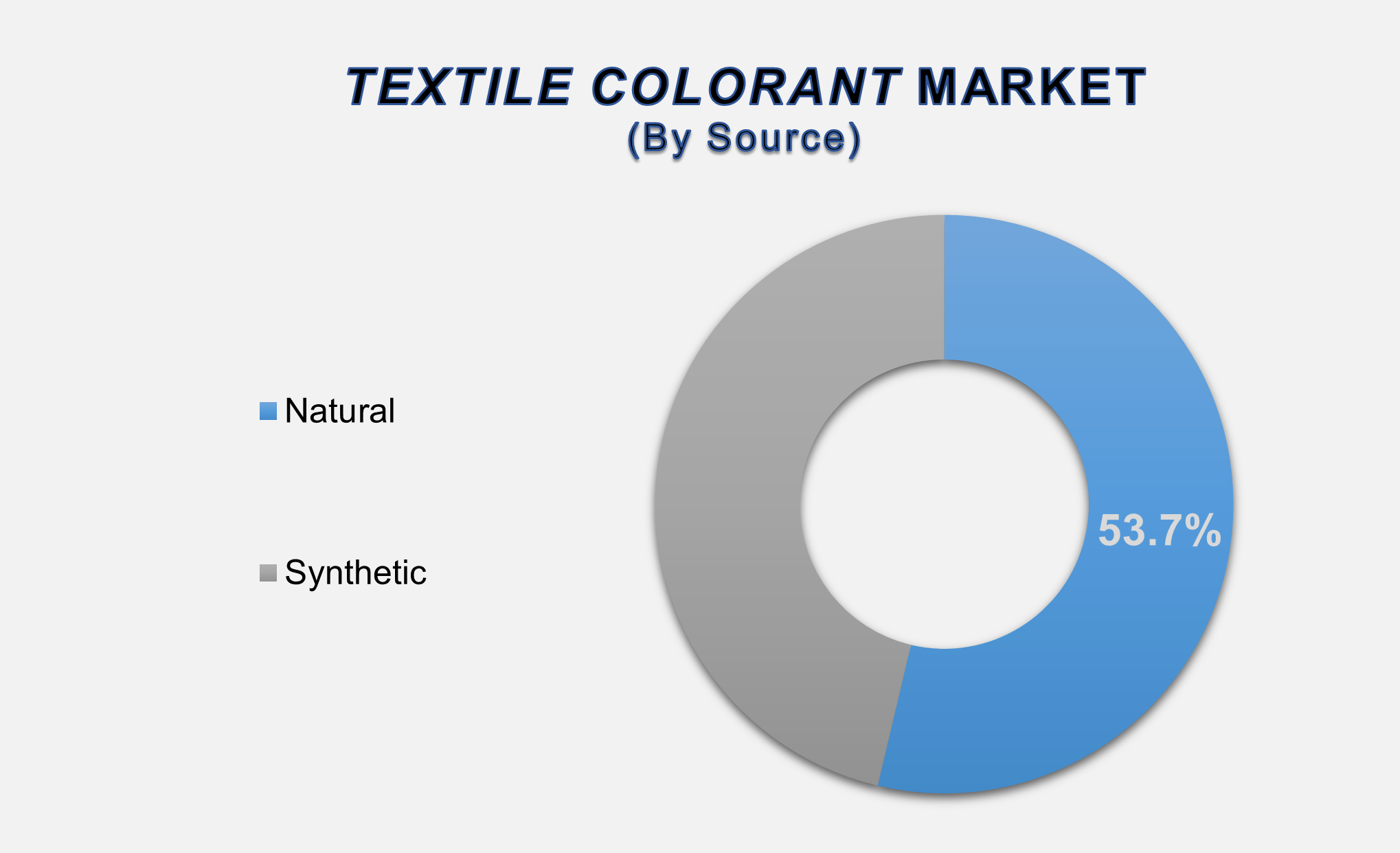

The natural segment accounted for the largest market share in the global textile colorant market, driven by rising sustainability awareness and increasing restrictions on synthetic dye chemicals. Natural dyes derived from plants, minerals, and organic sources are gaining popularity among apparel brands seeking eco-friendly and skin-safe products. These dyes are especially popular in premium clothing, organic apparel, and traditional textiles, where environmental credentials are becoming a key differentiator. Consumer demand for chemical-free and biodegradable fabrics is pushing brands to incorporate natural dyes into their collections. Additionally, natural colorants often offer softer shades and unique tonal variations that appeal to fashion designers and niche markets. While cost and scalability remain challenges, ongoing research into improved extraction and stabilization techniques is making natural dyes more commercially viable. As sustainability continues to shape textile procurement, the natural colorant segment is expected to maintain its leadership position.

Azoic

Dyes Segment Holds a Strong Position Across High-Volume Textile Applications

The

azoic dyes segment holds a strong share in the global textile colorant market

due to its cost-effectiveness and ability to deliver bright, vibrant shades,

particularly in cotton and cellulosic fibers. Azoic dyes are widely used in

mass-market clothing and home textiles because they offer good colorfastness and can be applied using relatively simple dyeing

processes. These dyes are especially popular in high-volume textile

manufacturing hubs in the Asia-Pacific region,

where efficiency, affordability, and consistent color output are critical.

Although environmental concerns are prompting gradual substitution in some

markets, azoic dyes remain essential for large-scale production of garments,

upholstery, and printed fabrics. Ongoing improvements in low-toxicity azo

formulations are helping this segment retain relevance in a more regulated

environment.

Clothing

Segment Represents the Largest Application Area for Textile Colorants

The

clothing segment accounted for the largest share of the textile colorant

market, reflecting the enormous global demand for dyed garments across fast

fashion, sportswear, luxury apparel, and traditional clothing. Every apparel

category, from T-shirts and denim to formal

wear and activewear, relies heavily on dyes

and pigments to create brand identity, visual appeal, and consumer

differentiation. Rapid fashion cycles and growing e-commerce penetration are

driving higher garment production volumes, which directly increase colorant

consumption. Additionally, trends such as custom designs, limited-edition

releases, and regional fashion preferences are increasing the number of colors

and shades used per production run. As the apparel industry continues to expand,

particularly in emerging markets, the clothing segment will remain the primary

revenue generator for textile colorant suppliers.

The following segments are

part of an in-depth analysis of the global Textile Colorant market:

|

Market Segments |

|

|

By Source |

●

Natural ●

Synthetic |

|

By Type |

●

Azoic Dyes ●

Direct Dyes ●

Basic Dyes ●

Disperse Dyes ●

Reactive Dyes ●

Sulfur Dyes ●

VAT Dyes ●

Others |

|

By Application |

●

Clothing ●

Technical Textiles ●

Home Textiles &

Carpets ●

Automotive Textiles |

Textile Colorant Market

Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Textile Colorant Market globally

throughout the forecast period.

Asia-Pacific dominates the

textile colorant market with a 41.9% share, driven by the region’s position as

the global hub for textile and garment manufacturing. China, India, Bangladesh,

Vietnam, and Indonesia host thousands of dyeing and finishing facilities

supplying international fashion and home textile brands. Strong export demand,

low-cost labor, and expanding production capacity continue to reinforce

Asia-Pacific’s leadership.

North America is expected to grow

at the fastest CAGR, supported by increasing adoption of sustainable textiles,

reshoring of manufacturing, and growth in technical textiles for automotive,

medical, and industrial applications. Rising regulatory enforcement and

consumer demand for eco-friendly products are also boosting demand for advanced

and compliant colorant solutions in the region.

Textile Colorant Market

Competition Landscape Analysis

The textile colorant market is

highly competitive, with players focusing on sustainable dye portfolios,

digital printing inks, and compliance-ready formulations. Companies are

investing in R&D to meet environmental regulations while improving color performance

and application efficiency.

Global Textile Colorant

Market Recent Developments News:

- In June 2023,

Archroma entered a partnership with COLOURizd to focus on

eco-friendlier production of high-performance sustainable textiles, aiming

for maximum consumer appeal with minimal environmental impact.

- In February 2023,

Archroma completed the acquisition of the Textile Effects business

from Huntsman Corporation, integrating it with its

own Brand & Performance Textile Specialties business to form a new

division named Archroma Textile Effects.

The Global Textile Colorant Market

Is Dominated by a Few Large Companies, such as

●

Kapsch TrafficCom AG

●

Huntsman Corporation

●

Archroma

●

DyStar

●

Kiri Industries

●

BASF

●

Zhejiang Longsheng

Group

●

Jihua Group

●

Atul Ltd

●

Allied Industrial Corp

●

Yorkshire Group

●

Synthesia

●

Lanxess

●

Organic Dyes and

Pigments

●

Everlight Chemical

●

Kyung-In Synthetic

●

BEZEMA

●

Colourtex

●

Jay Chemicals

●

Apexical

●

Pidilite Industries

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Textile Colorant

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Textile Colorant Market Scope and Market Estimation

1.2.1.Global Textile Colorant Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Textile Colorant

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Textile

Colorant Market

1.3.2.Source of Global Textile

Colorant Market

1.3.3.Application of Global Textile

Colorant Market

1.3.4.Region of Global Textile

Colorant Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Textile Colorant Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Textile Colorant Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Textile Colorant Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020

- 2033

4.1.1.Azoic Dyes

4.1.2.Direct Dyes

4.1.3.Basic Dyes

4.1.4.Disperse Dyes

4.1.5.Reactive Dyes

4.1.6.Sulfur Dyes

4.1.7.VAT Dyes

4.1.8.Others

5. Global

Textile Colorant Market Estimates

& Forecast Trend Analysis, by Source

5.1.

Global

Textile Colorant Market Revenue (US$ Bn) Estimates and Forecasts, by Source,

2020 - 2033

5.1.1.Natural

5.1.2.Synthetic

6. Global

Textile Colorant Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Textile Colorant Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Clothing

6.1.2.Technical Textiles

6.1.3.Home Textiles &

Carpets

6.1.4.Automotive Textiles

7. Global

Textile Colorant Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Textile Colorant Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Textile

Colorant Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Textile Colorant Market Assessments & Key Findings

8.1.1.North America Textile

Colorant Market Introduction

8.1.2.North America Textile

Colorant Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Source

8.1.2.3. By Application

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Textile

Colorant Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Textile Colorant Market Assessments & Key Findings

9.1.1.Europe Textile Colorant

Market Introduction

9.1.2.Europe Textile Colorant

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Source

9.1.2.3. By Application

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Textile

Colorant Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Textile Colorant Market Introduction

10.1.2.

Asia

Pacific Textile Colorant Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Type

10.1.2.2. By Source

10.1.2.3. By Application

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Textile

Colorant Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Textile Colorant Market Introduction

11.1.2.

Middle East & Africa Textile Colorant Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Source

11.1.2.3. By Application

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Textile Colorant Market: Estimates

& Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Textile Colorant Market Introduction

12.1.2.

Latin

America Textile Colorant Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Type

12.1.2.2. By Source

12.1.2.3. By Application

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Textile Colorant Market Product Mapping

14.2.

Global

Textile Colorant Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

14.3.

Global

Textile Colorant Market Tier Structure Analysis

14.4.

Global

Textile Colorant Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Huntsman Corporation

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Archroma

15.3. DyStar

15.4. Kiri

Industries

15.5. BASF

15.6. Zhejiang

Longsheng Group

15.7. Jihua

Group

15.8. Atul Ltd

15.9. Allied

Industrial Corp

15.10. Yorkshire

Group

15.11. Synthesia

15.12. Lanxess

15.13. Organic

Dyes and Pigments

15.14. Everlight

Chemical

15.15. Kyung-In

Synthetic

15.16. BEZEMA

15.17. Colourtex

15.18. Jay

Chemicals

15.19. Apexical

15.20. Pidilite

Industries

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables