Thin Film Solar Cells Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Cadmium Telluride (CdTe), Copper Indium Gallium Selenide (CIGS), Amorphous Silicon (a-Si), Perovskite), By Application (Utility-Scale, Commercial, Residential, Off-Grid), By End-User (Energy, Industrial, Automotive, Construction) And Geography

2025-12-17

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Thin Film

Solar Cells Market Overview

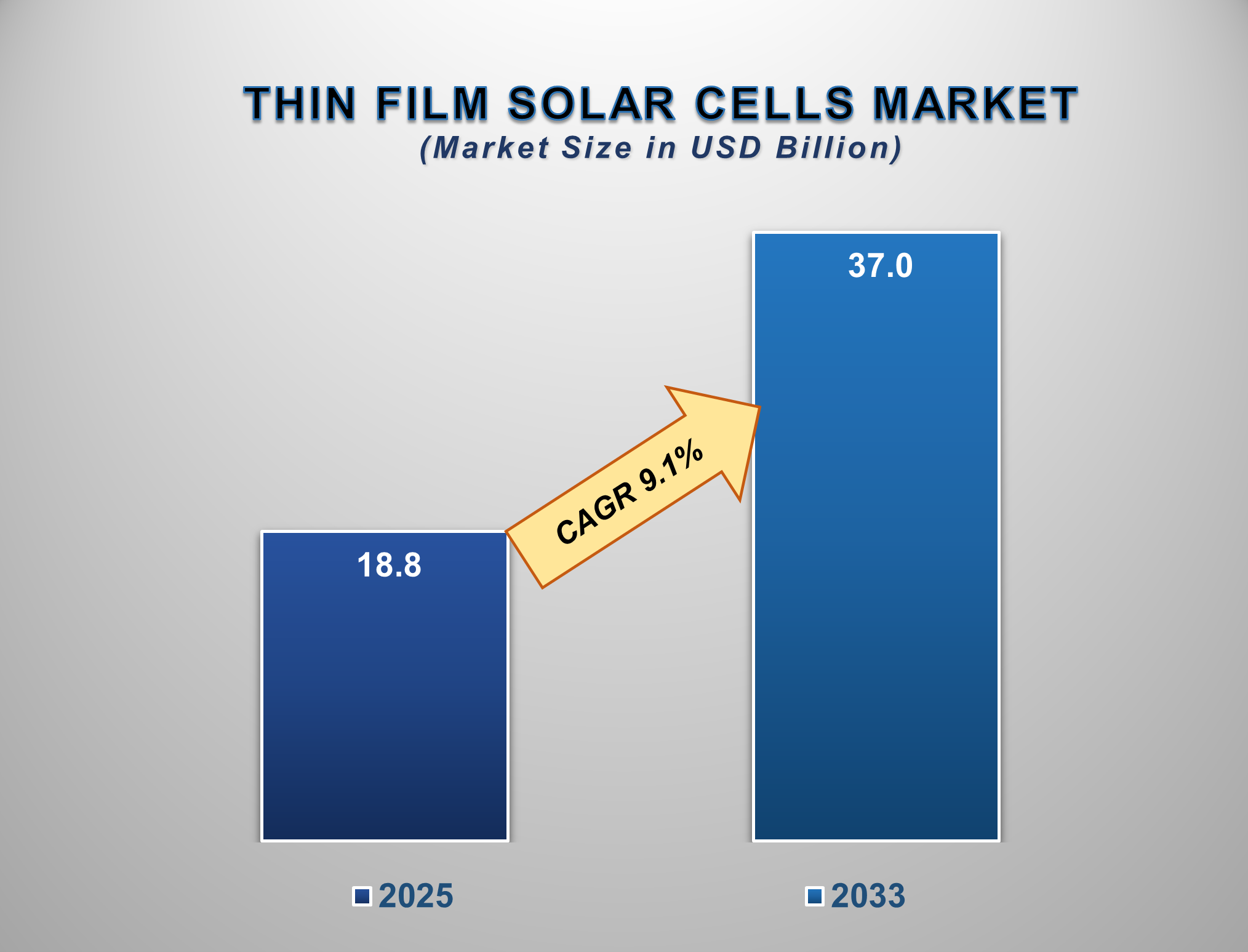

The Thin Film Solar Cells Market is poised for robust growth from 2025 to 2033, driven by the global push for renewable energy, rising demand for cost-effective and versatile solar solutions, and continuous technological advancements. The market is projected to be valued at approximately USD 18.8 billion in 2025 and is forecasted to reach nearly USD 37.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 9.1% during this period.

Thin-film solar cells are lightweight, flexible,

and semi-transparent photovoltaic devices that convert sunlight into

electricity. Unlike traditional silicon-wafer-based panels, they are created by

depositing one or more thin layers of photovoltaic material onto a substrate

like glass, plastic, or metal. The market's expansion is primarily fuelled by

their lower manufacturing costs, superior performance in low-light conditions,

and minimal material usage.

The versatility of thin film technology enables

its integration into building-integrated photovoltaics (BIPV),

vehicle-integrated photovoltaics (VIPV), and portable electronics, opening up

new application avenues. Government incentives, favorable policies promoting solar energy, and the declining cost of

raw materials are also significant contributors. Asia Pacific holds the largest

market share, driven by massive solar installations and a strong manufacturing

base, while North America and Europe are key regions for technological

innovation and BIPV adoption.

Thin Film Solar Cells Market Drivers and

Opportunities

Global Renewable Energy Transition and Cost Competitiveness

is the Primary Market Driver

The global imperative to transition from fossil

fuels to renewable energy sources is the most powerful driver for the thin-film solar cells market. Governments worldwide are setting

ambitious carbon neutrality targets, implementing supportive policies, and

offering subsidies for solar power generation. Thin film technology has become

increasingly cost-competitive with conventional crystalline silicon (c-Si)

panels, particularly for large-scale utility projects. The Levelized Cost of

Energy (LCOE) for thin-film solar, especially Cadmium Telluride (CdTe), is

among the lowest in the solar industry. This cost advantage, combined with

simpler and less energy-intensive manufacturing processes, makes thin film an

attractive option for developers aiming to maximize return on investment for

massive solar farms. The scalability of production and the ability to be

manufactured on flexible substrates further enhance its appeal for a diverse

range of applications beyond traditional solar farms, solidifying its role as a

cornerstone technology in the global energy transition.

Versatility and Emerging Application in Building-Integrated

Photovoltaics (BIPV) Are Driving Market Evolution

The unique physical properties of thin film

solar cells, such as flexibility, lightweight, and semi-transparency, are

unlocking new markets beyond conventional solar panels. The most significant

growth frontier is Building-Integrated Photovoltaics (BIPV), where solar cells

are seamlessly incorporated into building materials like windows, facades, and

roofs. This transforms buildings from energy consumers to energy producers

without compromising aesthetics. Similarly, the automotive industry is

exploring vehicle-integrated photovoltaics (VIPV) to power auxiliary systems

and extend the range of electric vehicles. The ability to deploy thin film on

curved surfaces and for portable charging applications further diversifies its

potential. This trend towards integrated and aesthetically pleasing solar

solutions is a major catalyst for market expansion beyond the utility sector.

Technological Breakthroughs in Perovskite and Tandem Cells

Present Significant Opportunities

Continuous innovation in materials and cell

architecture presents substantial growth frontiers. The most promising

opportunity lies in the development of perovskite solar cells, which have

demonstrated remarkable efficiency gains in laboratory settings and offer the

potential for ultra-low-cost, printable solar panels. The emergence of tandem

cells, which combine a thin film layer (like perovskite) with a traditional

silicon cell to capture a broader spectrum of sunlight, represents a

significant leap forward. These multi-junction cells have the potential to

shatter efficiency records, making solar power even more productive and

cost-effective. For manufacturers, investing in R&D to scale up perovskite

production, improve the long-term stability of new materials, and develop

commercial-grade tandem modules are key strategies for capturing future market share and driving the next

wave of solar adoption.

Thin Film Solar Cells Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 18.8 Billion |

|

Market Forecast in 2033 |

USD 37.0 Billion |

|

CAGR % 2025-2033 |

9.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Type ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Thin Film Solar Cells Market Report Segmentation

Analysis

The global Thin Film Solar Cells

Market industry analysis is segmented by Type, by Application, by End-User, and

by Region.

The Dominance of Cadmium

Telluride (CdTe)

The Cadmium Telluride (CdTe) segment is anticipated to command a dominant market share in 2025 due to its established position as the most commercially mature and cost-effective thin-film technology. Unlike its competitors, CdTe boasts a simplified and rapid manufacturing process, leading to the lowest production cost per watt, which is a critical factor for large-scale adoption. Its modules have demonstrated high and reliable efficiency in real-world, mass-produced settings, particularly excelling in hot and humid climates and under diffuse light conditions. This proven performance and durability in massive utility-scale projects have built strong trust among developers and investors. Furthermore, the supply chain for CdTe materials is well-developed and robust, minimizing production bottlenecks. As a result, CdTe's combination of economic advantage, proven field performance, and manufacturing scalability solidifies its leadership over newer and more niche thin-film alternatives like CIGS and the still-developing perovskite cells.

The Leadership of the

Utility-Scale Application

The

Utility-Scale segment is projected to be the largest application area for

thin-film solar cells because it directly leverages the technology's core

economic strengths. The primary driver for utility-scale solar farm developers

is minimizing the Levelized Cost of Energy (LCOE), and thin-film panels,

especially those based on Cadmium Telluride (CdTe), consistently offer one of

the lowest LCOEs in the entire solar industry. Their cost-effectiveness,

derived from cheaper manufacturing processes, makes them the preferred choice

for projects covering hundreds of acres and requiring hundreds of megawatts of

capacity. Additionally, thin films' superior

performance in high temperatures and low-light conditions ensures consistent

energy yield, which is crucial for the financial models of these large

installations. While commercial and residential segments are growing, the sheer

volume and scale of utility projects, driven by global renewable energy

targets, ensure this segment remains the dominant force in the thin-film

market.

The Energy Sector as the

Primary End-User

The

Energy sector is projected to exhibit the highest usage as an end-user because

it encompasses the primary function of thin-film solar cells: centralized and

distributed electricity generation. This segment directly includes

utility-scale solar farms, commercial power plants, and independent power

producers who are the largest volume purchasers of photovoltaic modules. The

energy sector's massive investments are driven by global decarbonization goals,

government incentives, and the declining cost of solar power, with thin-film

technology being a key beneficiary due to its cost-competitiveness. While the

Industrial, Automotive, and Construction sectors represent innovative and

high-growth application areas, their current volume of solar cell consumption does

not yet rival the gigawatt-scale deployments led by the energy sector. The

energy industry's fundamental role in procuring and operating power generation

assets cements its position as the dominant end-user, consuming the vast

majority of thin-film panels produced.

The following segments are

part of an in-depth analysis of the global Thin Film Solar Cells Market:

|

Market

Segments |

|

|

By Type |

●

Cadmium Telluride

(CdTe) ●

Copper Indium

Gallium Selenide (CIGS) ●

Amorphous Silicon

(a-Si) ●

Perovskite |

|

By

Application |

●

Utility-Scale ●

Commercial ●

Residential ●

Off-Grid |

|

By End-user |

●

Energy ●

Industrial ●

Automotive ●

Construction |

Thin Film Solar Cells Market Share Analysis by

Region

The Asia Pacific region

is anticipated to hold the largest portion of the Thin Film Solar Cells Market

globally throughout the forecast period.

Asia

Pacific's dominance is attributed to its massive investments in solar energy

infrastructure, strong government support for renewables, and the presence of

leading manufacturing hubs, particularly in China. The region has a high demand

for low-cost energy, driving the installation of large-scale solar farms where

thin film technology is highly competitive. Supportive policies, growing

industrial and residential electricity demand, and a robust supply chain

solidify Asia Pacific's position as the largest regional market. China is the

single largest market within Asia Pacific, driven by its national renewable

energy targets and its dominance in solar panel manufacturing. The country is a

global leader in both the production and deployment of thin film solar cells.

Its massive domestic market, coupled with strong government backing and a

complete industrial ecosystem for photovoltaic manufacturing, ensures its

continued leadership in the thin film segment.

Thin Film Solar Cells Market Competition

Landscape Analysis

The global thin film solar

cells market is moderately consolidated and features a mix of large,

specialized thin-film manufacturers and emerging players focusing on

next-generation technologies. Competition is based on conversion efficiency,

cost per watt, product durability, and technological innovation. Key strategies

include significant investment in R&D to improve cell efficiencies, scaling

up production to reduce costs, and forming strategic partnerships for

technology development and market entry.

Global Thin Film Solar

Cells Market Recent Developments News:

- In March 2025, First Solar, Inc. announced a breakthrough in its

Series 7 CdTe module, achieving a record conversion efficiency for

commercial production.

- In January 2025, a European consortium launched a pilot production

line for perovskite-on-silicon tandem cells, aiming for commercialization

by 2027.

- In October 2024, Hanergy Thin Film Power Group unveiled a new line of

flexible CIGS solar panels specifically designed for vehicle-integrated

photovoltaics (VIPV).

- In June 2024, Swift Solar secured significant funding to advance the

development and manufacturing of lightweight, high-performance perovskite

solar cells for aerospace and mobility applications.

The Global Thin Film

Solar Cells Market Is Dominated by a Few Large Companies, such as

●

First Solar, Inc.

●

Hanergy Thin Film

Power Group

●

Solar Frontier K.K.

(subsidiary of Idemitsu Kosan Co., Ltd.)

●

Ascent Solar

Technologies, Inc.

●

Kaneka Corporation

●

Oxford PV

●

Swift Solar

●

Flisom AG

●

Mitsubishi Electric

Corporation

●

Trony Solar Holdings

Co., Ltd.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Thin Film Solar

Cells Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Thin Film Solar Cells Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Mn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Thin Film Solar

Cells Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Thin Film

Solar Cells Market

1.3.2.Application of Global Thin

Film Solar Cells Market

1.3.3.End-user of Global Thin

Film Solar Cells Market

1.3.4.Region of Global Thin Film

Solar Cells Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Mn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Regulatory

Scenario by Region

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Thin Film Solar Cells Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Thin Film Solar Cells Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Thin Film Solar Cells Market Revenue (US$ Mn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.Cadmium Telluride (CdTe)

4.1.2.Copper Indium Gallium

Selenide (CIGS)

4.1.3.Amorphous Silicon (a-Si)

4.1.4.Perovskite

5. Global

Thin Film Solar Cells Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Thin Film Solar Cells Market Revenue (US$ Mn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Utility-Scale

5.1.2.Commercial

5.1.3.Residential

5.1.4.Off-Grid

6. Global

Thin Film Solar Cells Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Thin Film Solar Cells Market Revenue (US$ Mn) Estimates and Forecasts, by End-user

2020 - 2033

6.1.1.Energy

6.1.2.Industrial

6.1.3.Automotive

6.1.4.Construction

7. Global

Thin Film Solar Cells Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Thin Film Solar Cells Market Revenue (US$ Mn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Thin

Film Solar Cells Market: Estimates

& Forecast Trend Analysis

8.1.

North

America Thin Film Solar Cells Market Assessments & Key Findings

8.1.1.North America Thin Film

Solar Cells Market Introduction

8.1.2.North America Thin Film

Solar Cells Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By Application

8.1.2.3. By End-user

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Thin

Film Solar Cells Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Thin Film Solar Cells Market Assessments & Key Findings

9.1.1.Europe Thin Film Solar

Cells Market Introduction

9.1.2.Europe Thin Film Solar

Cells Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By Application

9.1.2.3. By End-user

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Thin

Film Solar Cells Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Thin Film Solar Cells Market Introduction

10.1.2.

Asia

Pacific Thin Film Solar Cells Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Type

10.1.2.2. By Application

10.1.2.3. By End-user

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Thin

Film Solar Cells Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Thin Film Solar Cells Market

Introduction

11.1.2.

Middle East & Africa Thin Film Solar Cells Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Application

11.1.2.3. By End-user

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Thin Film Solar Cells Market: Estimates

& Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Thin Film Solar Cells Market Introduction

12.1.2.

Latin

America Thin Film Solar Cells Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Type

12.1.2.2. By Application

12.1.2.3. By End-user

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Thin Film Solar Cells Market Product Mapping

14.2.

Global

Thin Film Solar Cells Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Thin Film Solar Cells Market Tier Structure Analysis

14.4.

Global

Thin Film Solar Cells Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

First Solar, Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Hanergy Thin

Film Power Group

15.3. Solar

Frontier K.K. (subsidiary of Idemitsu Kosan Co., Ltd.)

15.4. Ascent Solar

Technologies, Inc.

15.5. Kaneka

Corporation

15.6. Oxford PV

15.7. Swift Solar

15.8. Flisom AG

15.9. Mitsubishi

Electric Corporation

15.10. Trony Solar

Holdings Co., Ltd.

15.11. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables