Tracheostomy Products Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Tracheostomy Tubes, Ventilation Accessories, Cleaning Kits, Others), By Material (Polyvinyl Chloride, Silicone, Polyurethane, Others), By End User (Hospitals, Home Care Settings, Long-term Care Facilities, Ambulatory Surgical Centers) And Geography

2025-11-20

Healthcare

Swetal (Research Analyst)

Description

Tracheostomy Products Market Overview

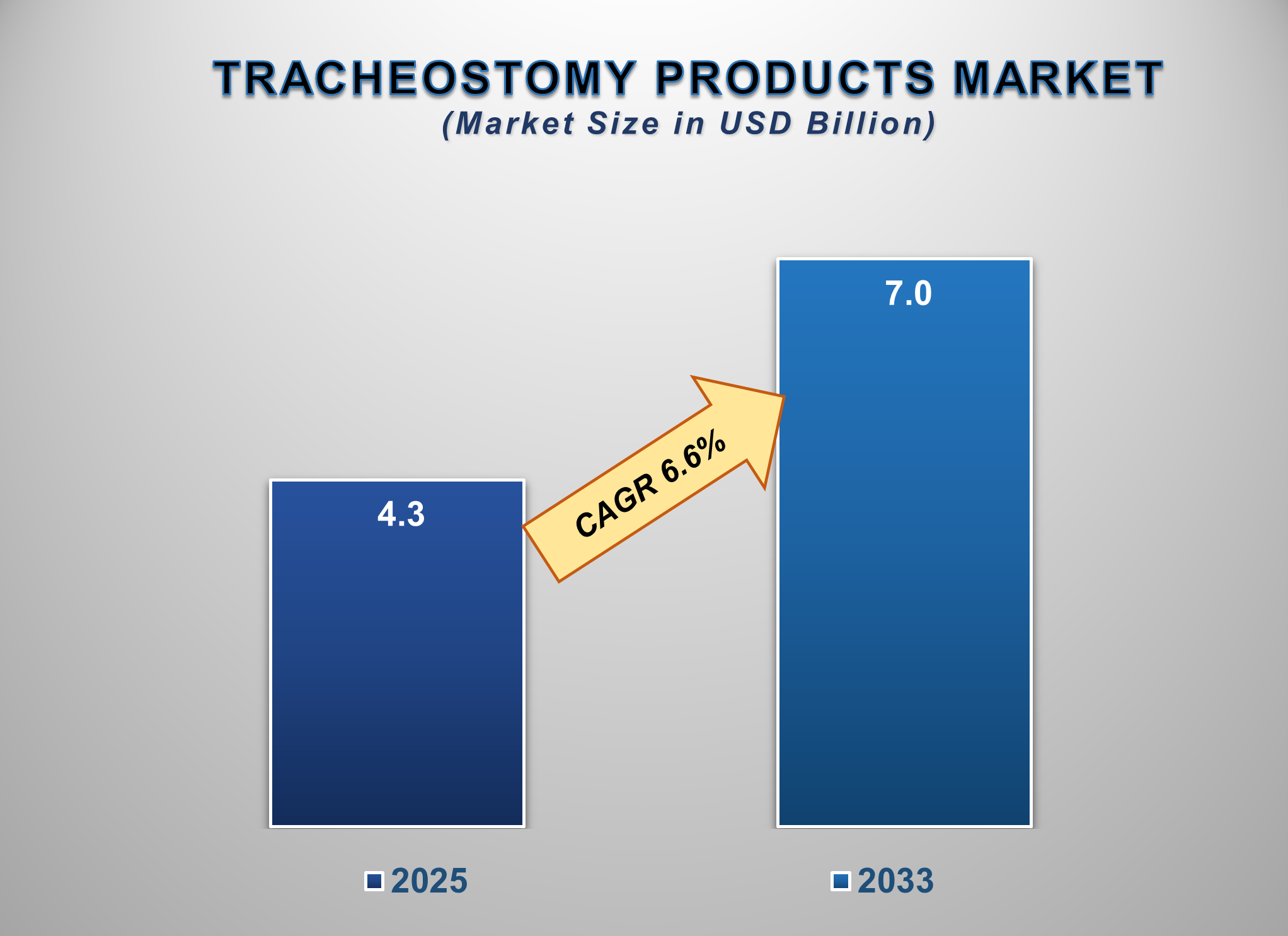

The Tracheostomy Products Market is poised for steady and sustained growth from 2025 to 2033, driven by the rising prevalence of chronic respiratory diseases, an aging global population, and advancements in minimally invasive surgical techniques. The market is projected to be valued at approximately USD 4.3 billion in 2025 and is forecasted to reach nearly USD 7.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.6% during this period.

Tracheostomy products are medical devices used

to create an artificial airway in the trachea through a surgical opening in the

neck. This procedure is critical for patients requiring long-term mechanical

ventilation, airway obstruction management, or pulmonary toileting. Market

growth is primarily fueled by the increasing incidence of conditions such as

chronic obstructive pulmonary disease (COPD), sleep apnea, and neurological

disorders, alongside the growing number of critical care patients surviving due

to improved medical interventions.

Technological innovations, including the

development of antimicrobial-coated tubes, low-pressure cuffs, and disposable

inner cannulas, are enhancing patient safety and comfort, thereby propelling

market adoption. The shift towards home-based care for long-term tracheostomy

patients is also creating a significant demand for user-friendly and safe

products for non-clinical settings. North America currently dominates the

market due to its advanced healthcare infrastructure and high healthcare

expenditure, while the Asia-Pacific region is expected to witness the fastest

growth, fueled by improving healthcare access and a large, underserved patient

population.

Tracheostomy

Products Market Drivers and Opportunities

The Rising Global Burden of Chronic

Respiratory Diseases is the Primary Market Driver

The escalating global prevalence of chronic

respiratory diseases, such as Chronic Obstructive Pulmonary Disease (COPD),

asthma, and lung cancer, directly fuels the demand for tracheostomy products.

As these conditions progress to severe stages, they often lead to acute

respiratory failure or chronic airway obstruction, making tracheostomy a

critical and often life-sustaining intervention. This procedure establishes a

secure airway for long-term mechanical ventilation or to bypass an obstruction,

creating a consistent and expanding patient population requiring specialized

medical devices. The World Health Organization,

identifying COPD as the third leading cause of death globally, underscores the scale of this driver. This high disease

burden translates directly into a growing and predictable pipeline of patients

in hospital ICUs and long-term care settings who need tracheostomy tubes and

associated accessories, ensuring a solid foundation for continuous market

growth. The procedure is no longer just for emergency trauma but a standard of

care for managing advanced chronic illness.

Technological Advancements and Product

Innovation are Enhancing Safety and Driving Adoption

Innovation in materials and design is a powerful

catalyst, transforming tracheostomy from a high-risk procedure to a safer,

long-term patient management solution. The shift from traditional Polyvinyl

Chloride (PVC) to advanced materials like silicone and polyurethane has been

pivotal, offering superior biocompatibility that minimizes tissue irritation,

inflammation, and the formation of granulation tissue. Furthermore,

technological integrations such as subglottic suction ports actively remove

secretions that pool above the tube cuff, drastically reducing the incidence of

fatal Ventilator-Associated Pneumonia (VAP). Antimicrobial coatings inhibit

biofilm formation, while integrated speech valves restore the ability to talk,

profoundly improving patients' quality of

life. These advancements address core clinical challenges—infection control,

patient safety, and dignity—making physicians more confident in recommending

tracheostomy and driving the adoption of premium, value-added products that

command higher prices and improve outcomes.

The Expanding Home Care Sector and Focus on

Cost-Effectiveness Present Significant Opportunities

The strategic shift in healthcare delivery from

expensive institutional settings to home-based care is creating a significant

growth frontier for the tracheostomy product market. Driven by the dual

pressures of reducing soaring hospital costs and enhancing patient quality of

life, there is a growing trend to discharge stable tracheostomy patients into

home care. This migration necessitates a new class of medical devices: products

designed specifically for ease of use by non-professional caregivers and patients

themselves. This includes foolproof cleaning kits, secure disposable inner

cannulas to minimize infection risk, and comprehensive educational resources.

For manufacturers, this opens entirely new distribution channels and spurs

innovation towards user-centric, safe, and simple-to-maintain products.

Catering to the home care segment is no longer a niche but a major strategic

opportunity, allowing companies to tap into a rapidly expanding and less

saturated market driven by healthcare's overarching goal of cost-effective,

patient-friendly care.

Tracheostomy Products

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.3 Billion |

|

Market Forecast in 2033 |

USD 7.0 Billion |

|

CAGR % 2025-2033 |

6.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Material ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Tracheostomy Products

Market Report Segmentation Analysis

The global Tracheostomy Products

Market industry analysis is segmented by Product Type, by Material, by

End-user, and by region.

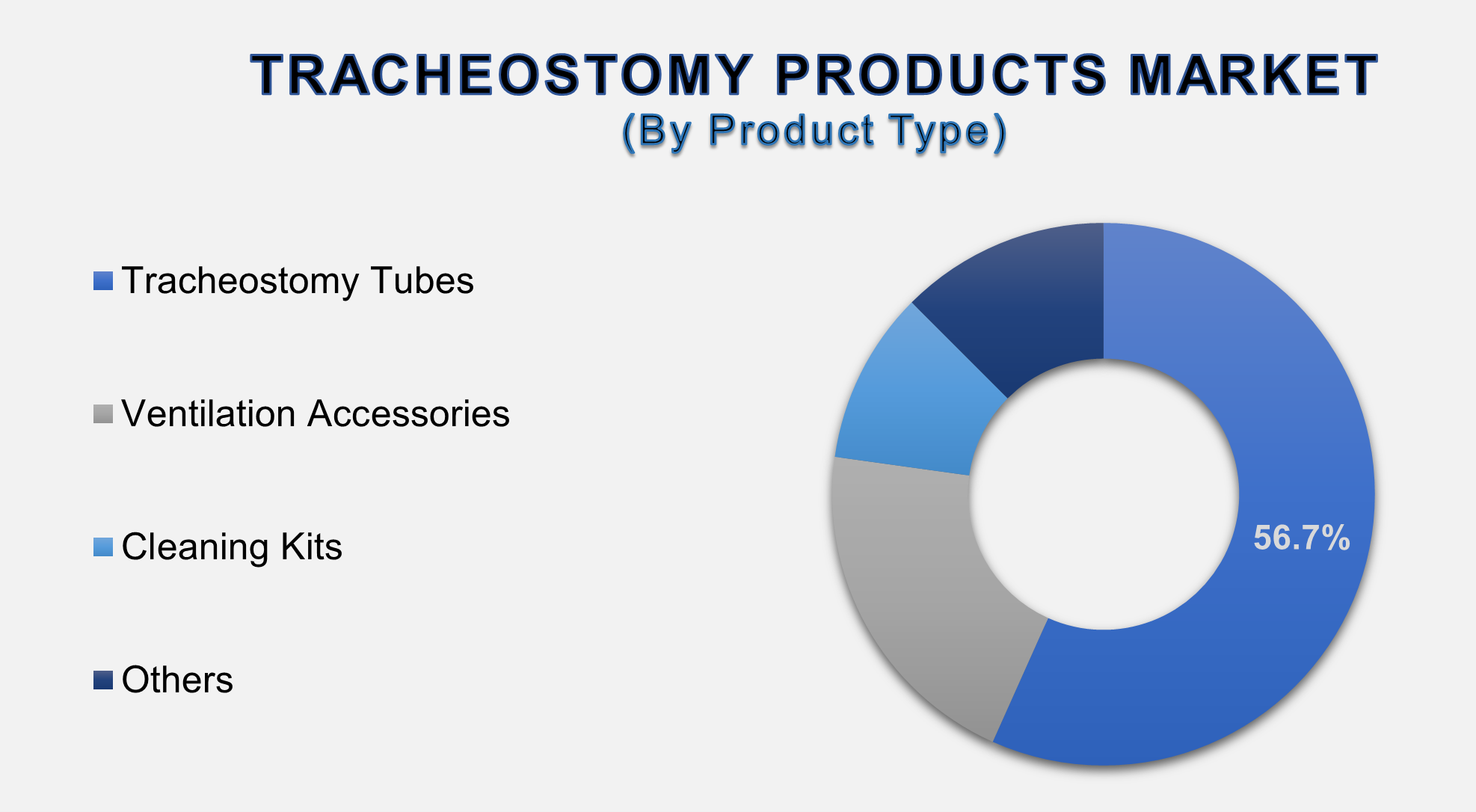

The Tracheostomy Tubes

product type segment is anticipated to command the largest market share in 2025

The dominance of the tracheostomy tube

segment is intrinsic to its role as the fundamental, indispensable device in

the entire market. It is the primary implantable component without which the

procedure cannot be performed, forming the baseline for all related product

sales. This segment's leadership is further reinforced by the critical need for

product specialization; a one-size-fits-all approach is clinically unviable.

The market offers a diverse array of tubes cuffed

for mechanical ventilation, uncuffed for stable airways, and fenestrated to

facilitate speech, each tailored to specific patient conditions and stages of

recovery. Moreover, unlike capital equipment, tracheostomy tubes are not a

one-time purchase. They require scheduled replacements due to material

degradation and biofilm formation and may need

to be changed for clinical reasons, such as downsizing as the patient's

condition improves. This creates a consistent, recurring revenue stream that

solidifies the segment's largest market share, driven by both initial procedure

volume and essential ongoing replacement cycles.

The Silicone material segment is projected to

grow at a significant CAGR.

The silicone segment's projected significant

growth is a direct result of the healthcare industry's escalating focus on

improving patient outcomes and reducing long-term complications. While PVC

remains a cost-effective option for short-term use, silicone's superior

material properties make it the preferred choice for the growing population of

patients requiring long-term or permanent tracheostomy. Its excellent

biocompatibility significantly reduces the risk of tissue irritation,

inflammation, and the development of traumatic granulation tissue, which are

common challenges with stiffer materials. Furthermore, silicone's inherent

flexibility enhances patient comfort, while its durability allows it to

withstand repeated sterilization, making it suitable for reusable tubes or

longer indwelling times. As clinical practice increasingly prioritizes the

prevention of hospital-acquired infections like ventilator-associated pneumonia

(VAP) and seeks to improve the quality of life for chronic patients, the

adoption of advanced, safer materials like silicone is accelerating, fueling

this segment's rapid expansion.

The hospitals' end-user segment

dominated the global tracheostomy products market in 2025.

Hospitals' position as the dominant end-user

segment is firmly rooted in their central role as the primary hub for acute and

critical care, where tracheostomies are most frequently initiated. They

are the undisputed site for performing the procedure itself, whether as a

planned surgery in the operating room or an urgent intervention at the bedside

in the Intensive Care Unit (ICU) for critically ill patients requiring

prolonged mechanical ventilation.

The immediate postoperative phase, which is

fraught with potential complications like bleeding or tube displacement,

necessitates close monitoring by specialized medical staff, cementing the

hospital's role in the initial care pathway. Furthermore, hospitals manage the

most complex patient populations—those with multi-organ failure, severe trauma,

or advanced respiratory diseases—for whom a tracheostomy is a critical

component of their life-saving treatment. This concentration of procedure

volume, high-acuity patients, and specialized care capabilities ensures that

hospitals remain the largest consumers of tracheostomy products.

The following segments are part of an in-depth analysis of

the global Tracheostomy Products Market:

|

Market

Segments |

|

|

By Product

Type |

●

Tracheostomy Tubes ●

Ventilation

Accessories ●

Cleaning Kits ●

Others |

|

By Material |

●

Polyvinyl Chloride

(PVC) ●

Silicone ●

Polyurethane ●

Others |

|

By End-user |

●

Hospitals ●

Home Care Settings ●

Long-term Care

Facilities ●

Ambulatory Surgical

Centers |

Tracheostomy Products

Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Tracheostomy Products Market

globally throughout the forecast period.

North America's dominance is attributed to its

well-established healthcare infrastructure, high healthcare expenditure, and

early adoption of advanced medical technologies. The region has a high

prevalence of respiratory diseases and a significant number of critical care

beds, leading to a large volume of tracheostomy procedures. Stringent

regulatory standards from the U.S. Food and Drug Administration (FDA) ensure a

market for high-quality, innovative products. Furthermore, the presence of

major global market players and robust reimbursement policies for both hospital

and home care settings solidifies North America's leading position.

Based on the most recent comprehensive data from

sources like the Healthcare Cost and Utilization Project (HCUP), which reported

approximately 108,000 procedures, and adjusting for consistent annual growth,

it is estimated that between 110,000 and 120,000 tracheostomy

procedures were performed in the United States in 2024. This projection

accounts for a steady historical growth rate of 2-3% per year, driven by key

demographic and clinical trends. An aging population with a higher prevalence

of chronic conditions such as severe COPD, neurological diseases, and head/neck

cancers contributes to a growing patient pool requiring this intervention.

Furthermore, advancements in critical care and

trauma medicine mean more patients survive acute emergencies but often require

prolonged mechanical ventilation. In these cases, a tracheostomy is the

standard of care to facilitate weaning from sedation, improve patient comfort,

reduce laryngeal injury, and allow for easier long-term airway management. The

vast majority of these procedures are conducted in hospital settings,

particularly within Intensive Care Units (ICUs) and operating rooms.

Tracheostomy Products

Market Competition Landscape Analysis

The global tracheostomy products

market is moderately consolidated and competitive, featuring a mix of large,

diversified medical device corporations and specialized players. Competition is

centered on product innovation, material science, clinical evidence, and

distribution network strength. Key strategies include launching products with

enhanced safety features (e.g., biofilm resistance, improved cuff designs),

strategic mergers and acquisitions to expand product portfolios, and forging

strong relationships with hospitals and home care service providers. The market

also sees competition from regional manufacturers offering cost-effective

alternatives.

Global Tracheostomy

Products Market Recent Developments News:

- In March 2025, Medtronic plc received FDA clearance

for its next-generation percutaneous tracheostomy kit, designed for faster

and more precise placement in critical care settings.

- In January 2025, Smiths Medical (a division of ICU

Medical) launched a new line of silicone tracheostomy tubes with a

proprietary TaperGuard cuff, aimed at reducing the risk of

micro-aspiration and ventilator-associated pneumonia (VAP).

- In November 2024, TRACOE Medical GmbH announced a

partnership with a major European home healthcare provider to distribute

its compact and user-friendly tracheostomy care kits directly to patients.

- In September 2024, Fisher & Paykel Healthcare introduced a new

integrated humidification system specifically designed for tracheostomy

patients in the home environment, focusing on comfort and airway

management.

The Global Tracheostomy

Products Market Is Dominated by a Few Large Companies, such as

●

Medtronic plc

●

Smiths Medical (ICU

Medical, Inc.)

●

Teleflex Incorporated

●

Fisher & Paykel

Healthcare Limited

●

TRACOE Medical GmbH

●

ConvaTec Group PLC

●

Boston Medical

Products Inc.

●

Cook Medical

●

Fuji Systems Corp.

●

Medis Medical GmbH

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Tracheostomy

Products Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Tracheostomy Products Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Tracheostomy

Products Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Tracheostomy

Products Market

1.3.2.Material of Global Tracheostomy

Products Market

1.3.3.End-user of Global Tracheostomy

Products Market

1.3.4.Region of Global Tracheostomy

Products Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Technological

Advancements

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Tracheostomy Products Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Tracheostomy Products Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Tracheostomy Products Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Tracheostomy Tubes

4.1.2.Ventilation Accessories

4.1.3.Cleaning Kits

4.1.4.Others

5. Global

Tracheostomy Products Market Estimates

& Forecast Trend Analysis, by Material

5.1.

Global

Tracheostomy Products Market Revenue (US$ Bn) Estimates and Forecasts, by Material,

2020 - 2033

5.1.1.Polyvinyl Chloride (PVC)

5.1.2.Silicone

5.1.3.Polyurethane

5.1.4.Others

6. Global

Tracheostomy Products Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Tracheostomy Products Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

6.1.1.Hospitals

6.1.2.Home Care Settings

6.1.3.Long-term Care Facilities

6.1.4.Ambulatory Surgical

Centers

7. Global

Tracheostomy Products Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Tracheostomy Products Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Tracheostomy

Products Market: Estimates &

Forecast Trend Analysis

8.1. North America Tracheostomy

Products Market Assessments & Key Findings

8.1.1.North America Tracheostomy

Products Market Introduction

8.1.2.North America Tracheostomy

Products Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product Type

8.1.2.2.

By Material

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Tracheostomy

Products Market: Estimates &

Forecast Trend Analysis

9.1. Europe Tracheostomy

Products Market Assessments & Key Findings

9.1.1.Europe Tracheostomy

Products Market Introduction

9.1.2.Europe Tracheostomy

Products Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product Type

9.1.2.2.

By Material

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Tracheostomy

Products Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Tracheostomy Products Market Introduction

10.1.2.

Asia

Pacific Tracheostomy Products Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Product Type

10.1.2.2.

By Material

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Tracheostomy

Products Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Tracheostomy Products Market Introduction

11.1.2. Middle

East & Africa

Tracheostomy Products Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product Type

11.1.2.2.

By Material

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Tracheostomy Products Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Tracheostomy

Products Market Introduction

12.1.2. Latin America Tracheostomy

Products Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product Type

12.1.2.2.

By Material

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Tracheostomy

Products Market Product Mapping

14.2. Global Tracheostomy

Products Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Tracheostomy

Products Market Tier Structure Analysis

14.4. Global Tracheostomy

Products Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Medtronic plc

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Smiths Medical (ICU Medical, Inc.)

15.3.

Teleflex Incorporated

15.4.

Fisher & Paykel Healthcare Limited

15.5.

TRACOE Medical GmbH

15.6.

ConvaTec Group PLC

15.7.

Boston Medical Products Inc. (A Besse Medical Company)

15.8.

Cook Medical

15.9.

Fuji Systems Corp.

15.10.

Medis Medical GmbH

15.11.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables