Traction Transformer Market Size and Forecast (2026 - 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Type (AC Traction Transformer and DC Traction Transformer); By Mounting Position (Underframe Mounted, Roof Mounted and Machine Room Mounted); By Rolling Stock (Electric Locomotives, High-Speed Trains, Metros, Light Rail Vehicles and Others); By Core Type (Shell Type and Core Type); By Cooling Type (Oil-cooled and Air-cooled) and Geography

2026-03-12

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Traction Transformer Market Overview

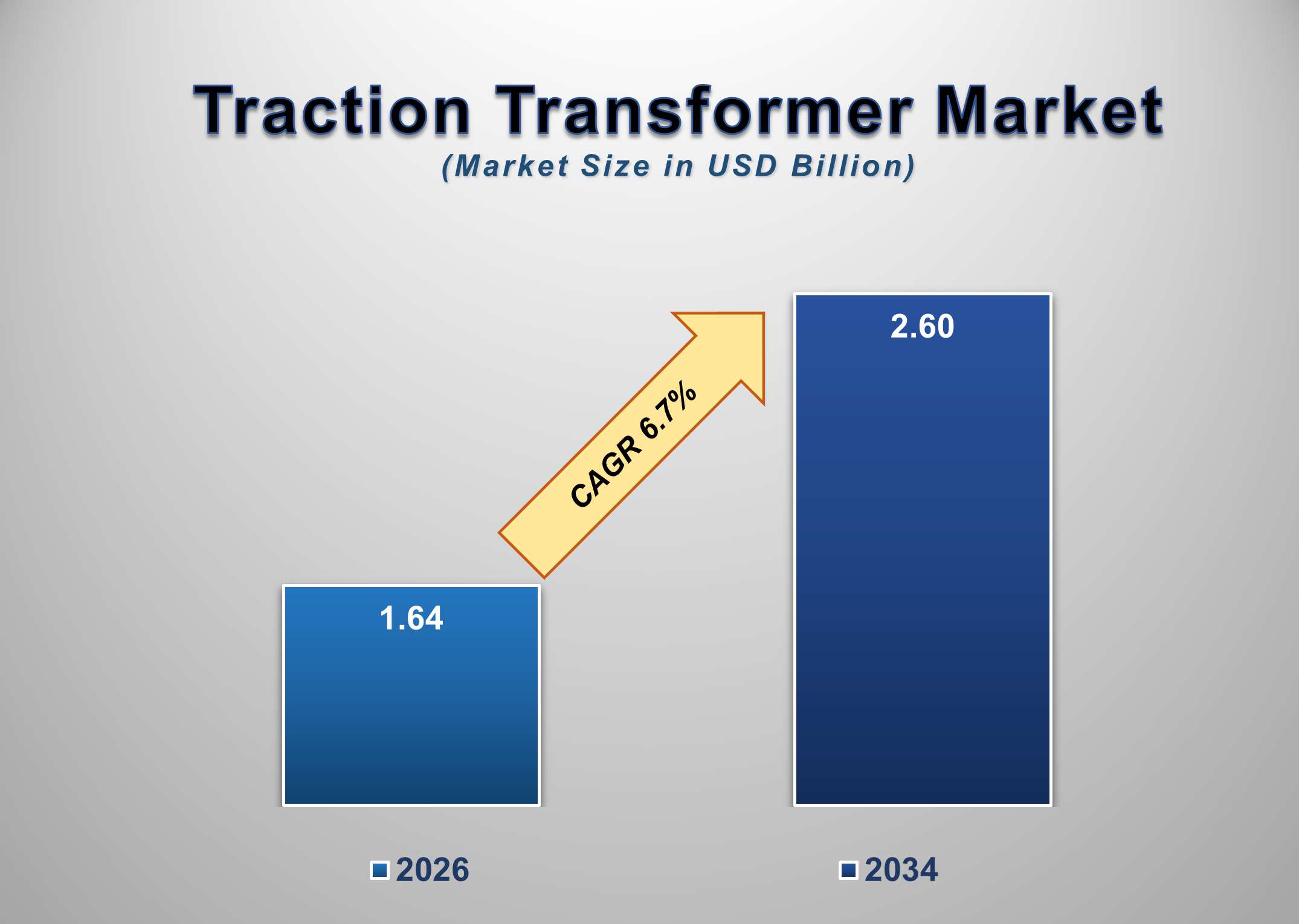

The global Traction Transformer Market is undergoing steady and structurally supported growth, primarily driven by accelerated railway electrification programs, large-scale investments in high-speed rail networks, and global efforts to reduce carbon emissions in the transportation sector. The global Traction Transformer Market is valued at USD 1.64 billion in 2026 and is projected to reach USD 2.60 billion by 2034, growing at a CAGR of 6.7% during the forecast period.

A traction transformer is a specialized power transformer installed in electric locomotives, metro rail systems, light rail vehicles, and high-speed trains. Its primary function is to step down high-voltage electricity supplied through overhead catenary systems or third rails into lower voltage levels suitable for traction motors and auxiliary onboard systems such as lighting, air conditioning, braking controls, and communication systems.

Unlike conventional industrial transformers, traction transformers are engineered to operate under extreme mechanical stress, rapid load fluctuations, vibration, thermal cycling, and varying climatic conditions. They must maintain high reliability and efficiency despite continuous acceleration, deceleration, and regenerative braking cycles. Modern traction transformers are increasingly designed with compact architecture, lightweight materials, and enhanced insulation systems to improve power density and reduce energy losses.

The global shift toward electrified and sustainable public transport infrastructure is fundamentally strengthening demand for high-performance traction transformers. Railway modernization initiatives across Asia-Pacific, Europe, and North America are creating consistent procurement cycles for new-generation transformer systems.

Traction Transformer Market Drivers and Opportunities

Accelerated Railway Electrification and High-Speed Rail Expansion are anticipated to lift the Traction Transformer market growth during the forecast period

Governments worldwide are prioritizing railway electrification as part of broader decarbonization and energy efficiency strategies. Electrified rail systems significantly reduce greenhouse gas emissions compared to diesel locomotives while delivering higher operational efficiency and lower long-term maintenance costs. As a result, multiple countries are aggressively phasing out diesel-powered rolling stock and upgrading rail corridors to electric traction systems.

Large-scale high-speed rail projects in Asia-Pacific and Europe require advanced traction transformers capable of handling higher voltage inputs, rapid acceleration demands, and sustained high-speed operation. High-speed trains operate under continuous heavy electrical loads, necessitating transformers with superior thermal performance, insulation durability, and efficient magnetic core design.

In emerging economies, railway electrification also improves freight transport efficiency and reduces dependence on imported fossil fuels. The expansion of electrified rail routes directly increases demand for traction transformers, as each new locomotive or train set requires a customized transformer configuration. Consequently, railway electrification projects represent a foundational growth pillar for the traction transformer market.

Rapid Urbanization and Expansion of Metro & Light Rail Systems are vital drivers for influencing the growth of the global Traction Transformer market

Urban population growth and increasing traffic congestion are compelling governments to invest heavily in metro rail, suburban rail, and light rail transit systems. Electrified urban transit solutions offer a sustainable alternative to road-based transportation while supporting economic productivity in densely populated cities.

Metro systems require compact and lightweight traction transformers that can fit within restricted vehicle spaces while maintaining high power output. Advances in insulation materials, improved silicon steel core laminations, and optimized cooling mechanisms have enabled manufacturers to design transformers with enhanced energy efficiency and reduced physical footprint.

Additionally, the integration of regenerative braking systems in modern metro trains introduces bidirectional power flow challenges. Traction transformers must efficiently manage dynamic power conversion when excess braking energy is fed back into the grid. This technical requirement has driven innovation in transformer design, further expanding market opportunities.

The continuous rollout of urban rail networks across Asia-Pacific, the Middle East, and Latin America ensures sustained demand for traction transformer installations over the forecast period.

Adoption of Energy-Efficient and Lightweight Transformer Technologies is poised to create significant opportunities in the global Traction Transformer market

An emerging opportunity in the traction transformer market lies in the development of energy-efficient, lightweight, and environmentally optimized transformer solutions. Rail operators are increasingly focused on reducing energy losses, lowering operational costs, and enhancing overall train performance.

Manufacturers are investing in advanced magnetic core materials, improved winding techniques, and high-performance insulation systems to reduce transformer weight while increasing efficiency. Lightweight transformers contribute to lower overall train mass, resulting in improved acceleration, reduced track wear, and lower energy consumption.

Furthermore, the growing emphasis on lifecycle cost optimization is encouraging the adoption of transformers with enhanced durability and predictive maintenance capabilities. Integration of sensor-based monitoring systems allows operators to track temperature, load variations, and performance parameters in real time, minimizing unexpected failures and reducing downtime.

As railway operators transition toward smarter and greener transportation systems, demand for technologically advanced traction transformers is expected to rise significantly.

Traction Transformer Market Scope

Traction Transformer Market Report Segmentation Analysis

The global Traction Transformer Market industry analysis is segmented by type, mounting position, rolling stock, core type, cooling type, and region.

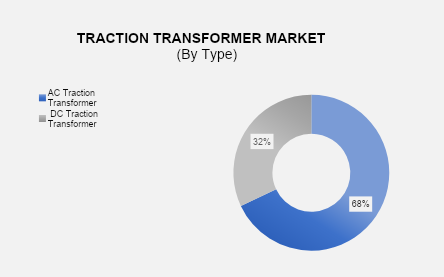

AC Traction Transformer Dominates the Type Segment

By Type, the market is segmented into AC Traction Transformer and DC Traction Transformer. AC traction transformers dominate the market due to the widespread adoption of alternating current electrification systems across modern railway corridors. AC systems allow efficient long-distance transmission with reduced transmission losses, making them suitable for intercity and high-speed networks. These transformers are designed to manage high input voltages and deliver stable output to traction motors, even under fluctuating load conditions. DC traction transformers continue to serve legacy urban transit systems and certain regional rail networks where DC electrification remains operational.

Underframe-mounted holds the highest share of the Mounting Position Segment

Based on mounting position, the market is segmented into Underframe Mounted, Roof Mounted, and Machine Room Mounted configurations. Underframe-mounted traction transformers hold the highest share because they optimize space utilization and improve weight distribution along the train body. This positioning enhances vehicle stability and allows better interior design flexibility for passenger compartments. Roof-mounted systems are used in specific rolling stock designs where underframe space is limited, while machine room-mounted transformers are typically found in larger locomotives.

Electric Locomotives Segment Leads by Rolling Stock

In terms of rolling stock, the market is segmented into Electric Locomotives, High-Speed Trains, Metros, Light Rail Vehicles, and Others. Electric locomotives represent the largest segment due to their extensive deployment in freight and passenger rail services globally. These locomotives require high-capacity traction transformers capable of handling heavy electrical loads over long operational hours. High-speed trains are projected to witness strong growth due to ongoing bullet train and intercity rapid transit projects across the Asia-Pacific and Europe.

Oil-cooled Transformers are a key Cooling Type

In terms of cooling type, the market is segmented into Oil-cooled and Air-cooled transformers. Oil-cooled transformers dominate due to superior heat dissipation efficiency and enhanced load-bearing capability. Oil serves both as an insulating medium and a cooling agent, enabling the transformer to operate under high-power conditions without overheating. Air-cooled transformers are typically used in lighter rolling stock applications where compact design and reduced maintenance are prioritized.

The following segments are part of an in-depth analysis of the global Traction Transformer Market:

Traction Transformer Market Share Analysis by Region

The Asia-Pacific region is projected to hold the largest share of the global Traction Transformer Market over the forecast period.

Asia-Pacific leads the market due to extensive railway electrification programs, high-speed rail expansion, and rapid metro development in China, India, Japan, and South Korea. Europe maintains a substantial share supported by cross-border rail modernization and sustainable transport policies. North America is witnessing stable growth driven by infrastructure upgrades and freight rail electrification initiatives.

Global Traction Transformer Market Recent Developments News:

o In July 2025, a leading rail equipment manufacturer introduced a next-generation lightweight traction transformer optimized for high-speed rail applications.

o In May 2025, a European metro authority upgraded its rolling stock fleet with energy-efficient oil-cooled traction transformers to improve operational performance.

o In March 2025, an Asian rail infrastructure project commissioned high-capacity traction transformers for a newly electrified freight corridor.

The Global Traction Transformer Market is dominated by a few large companies, such as

● Siemens Mobility

● ABB Ltd.

● Alstom SA

● Hitachi Rail

● Mitsubishi Electric Corporation

● CRRC Corporation Limited

● Toshiba Corporation

● Hyundai Rotem

● Wabtec Corporation

● Schneider Electric

● Fuji Electric Co., Ltd.

● CG Power and Industrial Solutions

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Traction Transformer Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables