Veterinary Point of Care Diagnostics Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Consumables, Devices), By Technology (Immunoassay, Clinical Chemistry, Haematology, Urinalysis, Others), By Animal Type (Companion Animals, Livestock Animals), By End-User (Veterinary Hospitals & Clinics, Home Care Settings, Research Institutes) And Geography

2025-12-12

Healthcare

Swetal (Research Analyst)

Description

Veterinary

Point of Care Diagnostics Market Overview

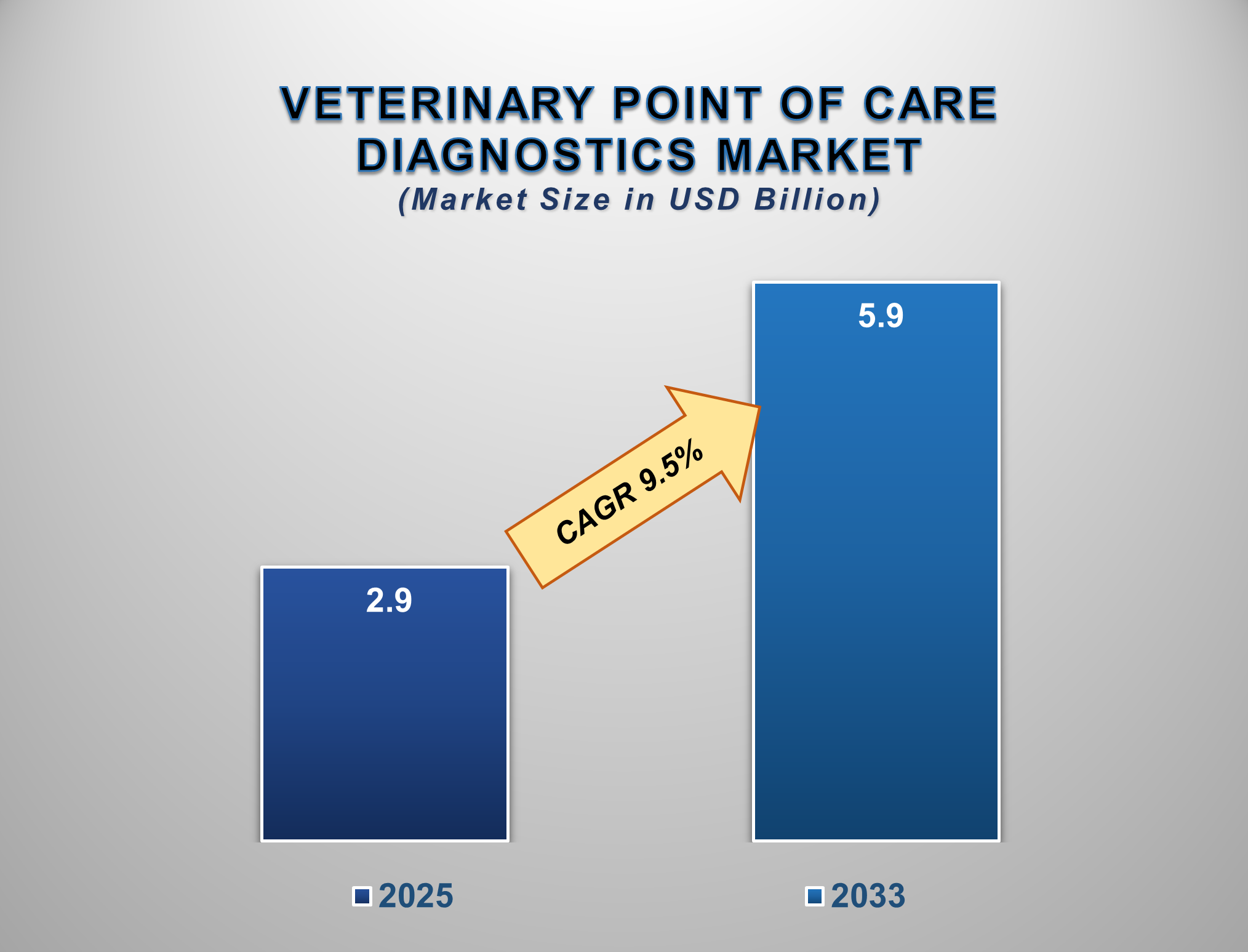

The Veterinary Point of Care (POC) Diagnostics Market is set to experience significant expansion from 2025 to 2033, fueled by the growing demand for immediate clinical decisions, the rising prevalence of animal diseases, and the increasing integration of pets into families. The market is projected to be valued at approximately USD 2.9 billion in 2025 and is forecasted to reach nearly USD 5.9 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 9.5% during this period.

Veterinary point-of-care diagnostics encompass a wide range of tests and devices used to perform diagnostic procedures at or near the site of patient care, delivering results within minutes. This immediacy allows veterinarians to diagnose conditions, monitor treatments, and initiate therapies without delay, greatly enhancing patient outcomes and client satisfaction. The market's growth is primarily driven by the surging pet ownership globally, coupled with the increasing willingness of pet owners to spend on advanced healthcare.

The trend towards humanization of pets is

leading to a higher standard of care, comparable to human medicine, where rapid

diagnostics are the norm. Technological advancements that have made POC devices

more compact, affordable, and user-friendly are also critical drivers. North

America currently leads the market, while the Asia-Pacific region is

anticipated to witness the fastest growth, spurred by a growing middle class,

increasing awareness of animal health, and the development of veterinary

infrastructure.

Veterinary Point of Care Diagnostics Market

Drivers and Opportunities

Rising Pet Ownership and Humanization of Pets are the Primary

Market Drivers

The increasing number of companion animals and

their elevated status as family members represent the most significant driver

for the veterinary POC diagnostics market. Pet owners are now more invested in

the health and well-being of their animals, seeking immediate and high-quality

medical care. This shift in mindset translates to a greater demand for

in-clinic testing that provides quick answers, avoids the anxiety of waiting

for external lab results, and enables faster treatment. Conditions like diabetes,

kidney disease, and infections can be managed more effectively with regular,

on-the-spot monitoring. This client-driven demand for rapid service and

comprehensive care is compelling veterinary practices to invest in POC

diagnostic equipment, making it a standard of care in modern veterinary

practice.

Growing Prevalence of Zoonotic and Chronic Diseases in

Animals is Driving Market Evolution

The rising incidence of chronic diseases such as

diabetes, arthritis, and renal failure in aging pet populations, alongside the

persistent threat of zoonotic diseases (like Lyme disease or leptospirosis), necessitates frequent and rapid diagnostic monitoring. POC

testing allows for the immediate detection of these conditions during a single

visit, facilitating prompt intervention and long-term disease management. For

livestock, the economic impact of diseases like Bovine Respiratory Disease

(BRD) or mastitis drives the need for rapid on-farm testing to isolate sick

animals, prevent herd-wide outbreaks, and optimize antibiotic use. This focus

on preventive healthcare and biosecurity in both companion and livestock

animals is a major catalyst for the adoption of POC diagnostics.

Technological Innovation and Expansion into Home Care Present

Significant Opportunities

Continuous technological advancements are

creating substantial growth frontiers for the market. Key opportunities lie in

the development of multi-analyte platforms that can run a suite of tests (e.g.,

chemistry, electrolytes, immunoassays) from a single small blood sample. The

integration of connectivity features, such as cloud-based data management and

digital health records, allows for seamless tracking of patient health over

time. Another significant opportunity is the emerging market for at-home POC

test kits, allowing pet owners to monitor certain health parameters, such as

glucose levels or UTI strips, between veterinary visits. For manufacturers,

investing in R&D for novel biomarkers, creating more robust and portable

devices for field use in livestock, and tapping into the vast potential of

emerging markets are key strategies for future growth.

Veterinary Point of Care Diagnostics Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.9 Billion |

|

Market Forecast in 2033 |

USD 5.9 Billion |

|

CAGR % 2025-2033 |

9.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product ●

By Technology ●

By Animal Type ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Veterinary Point of Care Diagnostics Market

Report Segmentation Analysis

The global Veterinary Point of

Care Diagnostics Market industry analysis is segmented by Product, by

Technology, by Animal Type, by End-User, and by region.

The Consumables segment

is anticipated to command a dominant market share in 2025.

The Product segment is categorized into Consumables and Devices. The Consumables segment, which includes test kits, reagents, cartridges, and dipsticks, commands the largest market share. This is due to their recurrent nature of purchase; while a diagnostic analyzer is a one-time capital investment, the consumables are purchased continuously for every test run. The high and growing volume of POC tests performed daily in veterinary clinics and hospitals worldwide ensures consistent and recurring revenue from this segment. The development of multi-test panels and the expansion of test menus further drive the consumption of these disposable products.

The Companion Animals

segment is projected to be the largest and fastest-growing.

The

Animal Type segment is divided into Companion Animals and Livestock Animals.

The Companion Animals segment is the largest and fastest-growing segment. This

dominance is directly linked to the primary market driver of pet humanization.

The deep emotional bond between owners and their pets leads to higher spending

on advanced healthcare services. Companion animals, especially dogs and cats,

are also more frequently presented to veterinarians for routine check-ups,

vaccinations, and illness, creating more opportunities for POC testing compared

to livestock, where testing is often more targeted towards disease outbreaks or

herd health screening.

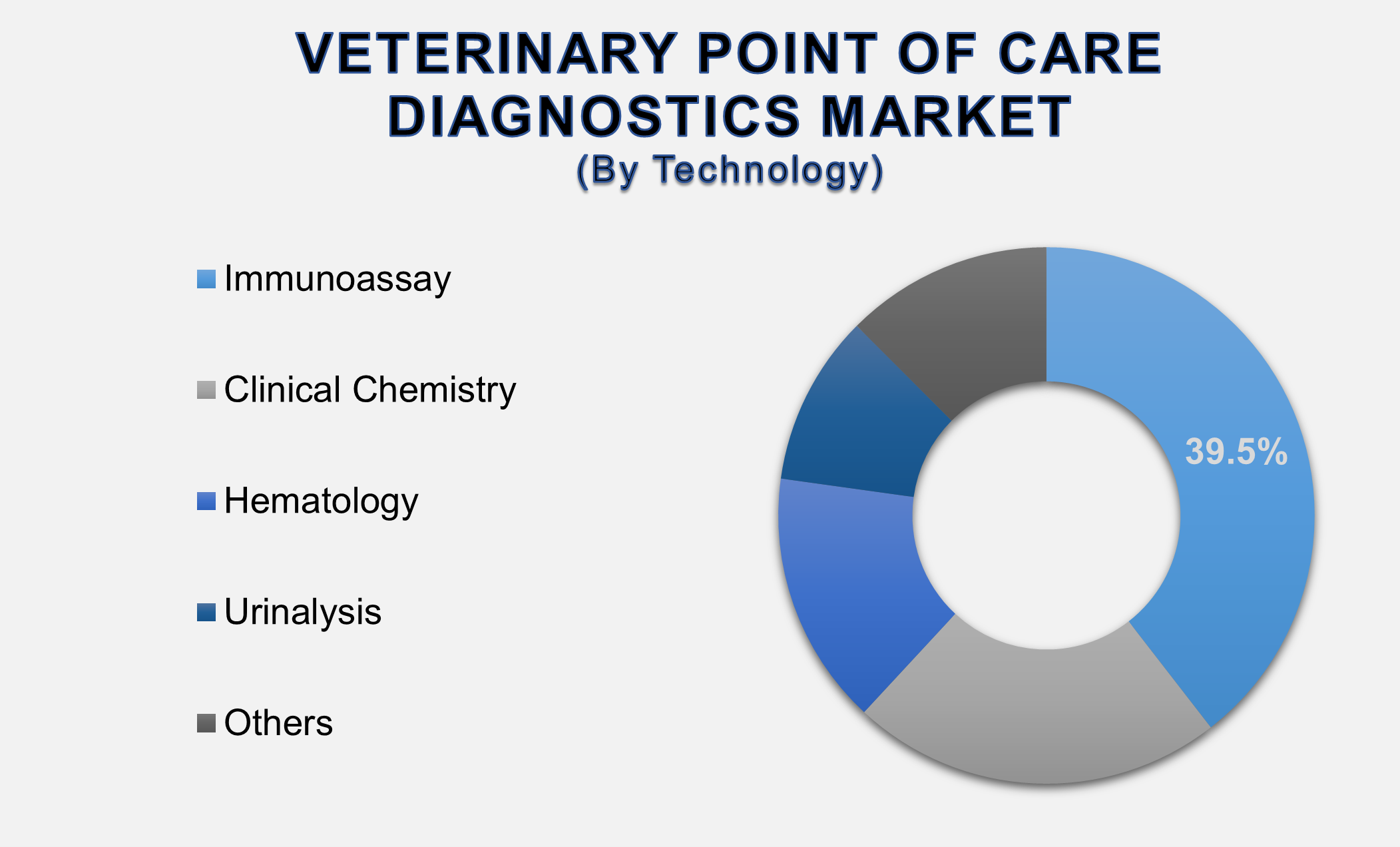

The Immunoassay segment

is projected to exhibit strong growth.

The

Technology segment includes Immunoassay, Clinical Chemistry, Hematology,

Urinalysis, and Others. The Immunoassay segment exhibits strong growth due to

its critical role in detecting specific pathogens, hormones, and biomarkers.

This technology is essential for rapid tests for heartworm, Lyme disease,

Ehrlichia, Parvovirus, and Feline Immunodeficiency Virus (FIV). The high

sensitivity and specificity of immunoassays, combined with their format as

easy-to-use lateral flow assays (rapid test kits), make them immensely popular

in the clinic for confirming infections and guiding treatment decisions

quickly. The continuous introduction of new tests for various infectious

diseases ensures this segment's robust expansion.

The following segments are

part of an in-depth analysis of the global Veterinary Point of Care Diagnostics

Market:

|

Market

Segments |

|

|

By Product |

●

Consumables ●

Devices |

|

By Technology |

●

Immunoassay ●

Clinical Chemistry ●

Hematology ●

Urinalysis ●

Others |

|

By Animal Type |

●

Companion Animals ●

Livestock Animals |

|

By End-user |

●

Veterinary Hospitals

& Clinics ●

Home Care Settings |

Veterinary Point of Care Diagnostics Market Share

Analysis by Region

The North America region

is anticipated to hold the largest portion of the Veterinary Point of Care

Diagnostics Market globally throughout the forecast period.

North

America's dominance is attributed to its well-established and technologically

advanced veterinary healthcare infrastructure, high pet insurance penetration,

and strong presence of leading market players. The region has a high number of

veterinary practices that have adopted POC diagnostics as a standard of care.

High awareness and spending power of pet owners, coupled with stringent

regulations promoting animal health and welfare, solidify North America's

position as the largest regional market.

The

U.S. boasts the world's largest per capita

expenditure on pet care, with the American Pet Products Association (APPA)

estimating national spending to exceed US$147 billion in 2023. This

immense financial commitment directly fuels the demand for advanced veterinary

services, including immediate diagnostics. The country's advanced veterinary

infrastructure is a key driver, with over 30,000 private veterinary

clinics and a rapidly consolidating network of large corporate-owned

hospitals. These entities heavily invest in POC equipment to enhance clinical

efficiency and client service.

Technologically,

the U.S. is the headquarters for global industry leaders like IDEXX

Laboratories and Zoetis, which continuously drive innovation and set the

standard for in-clinic testing. Their widespread distribution networks and deep

market penetration ensure the rapid adoption of new devices and consumables.

Culturally, the intense "humanization" of pets compels owners to seek

a standard of care parallel to human medicine, where rapid, accurate

diagnostics are non-negotiable. This demand, supported by high pet insurance

adoption and stringent standards of care, ensures the U.S. will maintain its

dominant market position for the foreseeable future.

Veterinary Point of Care Diagnostics Market

Competition Landscape Analysis

The global veterinary point of

care diagnostics market is moderately consolidated and is characterized by the

presence of both large, diversified medical companies and specialized

veterinary diagnostic firms. Competition is intense and based on factors such

as product accuracy, test menu breadth, ease of use, price, and the strength of

distribution and support networks. Key strategies observed in the market

include continuous product innovation and launches, strategic acquisitions to

expand technological portfolios and geographic reach, and forming partnerships

with veterinary teaching hospitals and large corporate practice chains.

Global Veterinary Point

of Care Diagnostics Market Recent Developments News:

- In January 2025, IDEXX Laboratories, Inc.,

announced the launch of its next-generation in-clinic chemistry analyzer,

featuring enhanced connectivity and a broader test menu for exotic pets.

- In October 2024, Zoetis Inc. acquired a company specializing in

digital cytology and AI-based image analysis for POC diagnostics.

- In August 2024, Heska Corporation (now part of Mars, Inc.) received

CE marking for its new multi-parameter POC blood analyzer designed for

high-volume veterinary hospitals.

- In May 2024, Virbac launched a new rapid, single-use test for the

early detection of Feline Leukemia

Virus (FeLV) antigen in-clinic.

The Global Veterinary

Point of Care Diagnostics Market Is Dominated by a Few Large Companies, such as

●

IDEXX Laboratories,

Inc.

●

Zoetis Inc.

●

Thermo Fisher

Scientific Inc.

●

Heska Corporation

●

Virbac

●

bioMérieux SA

●

Randox Laboratories

Ltd.

●

Woodley Equipment

Company Ltd.

●

CareHealth America

Corporation

●

Eurolyser Diagnostica

GmbH

●

NeuroLogica Corp.

●

Shenzhen Mindray

Animal Medical Technology Co., Ltd.

●

Henry Schein, Inc.

●

Abaxis

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Veterinary Point of Care Diagnostics Market Introduction

and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Veterinary Point of Care Diagnostics Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Mn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Veterinary Point of

Care Diagnostics Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Veterinary

Point of Care Diagnostics Market

1.3.2.Technology of Global Veterinary

Point of Care Diagnostics Market

1.3.3.Animal Type of Global Veterinary

Point of Care Diagnostics Market

1.3.4.End-user of Global Veterinary

Point of Care Diagnostics Market

1.3.5.Region of Global Veterinary

Point of Care Diagnostics Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Mn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Regulatory

Scenario by Region

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Veterinary Point of Care Diagnostics Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Veterinary Point of Care Diagnostics Market

Estimates & Forecast Trend Analysis, by Product

4.1.

Global

Veterinary Point of Care Diagnostics Market Revenue (US$ Mn) Estimates and

Forecasts, by Product, 2020 - 2033

4.1.1.Consumables

4.1.2.Devices

5. Global

Veterinary Point of Care Diagnostics Market

Estimates & Forecast Trend Analysis, by Technology

5.1.

Global

Veterinary Point of Care Diagnostics Market Revenue (US$ Mn) Estimates and

Forecasts, by Technology, 2020 - 2033

5.1.1.Immunoassay

5.1.2.Clinical Chemistry

5.1.3.Hematology

5.1.4.Urinalysis

5.1.5.Others

6. Global

Veterinary Point of Care Diagnostics Market

Estimates & Forecast Trend Analysis, by Animal

Type

6.1.

Global

Veterinary Point of Care Diagnostics Market Revenue (US$ Mn) Estimates and

Forecasts, by Animal Type 2020 - 2033

6.1.1.Companion Animals

6.1.2.Livestock Animals

7. Global

Veterinary Point of Care Diagnostics Market

Estimates & Forecast Trend Analysis, by End-user

7.1.

Global

Veterinary Point of Care Diagnostics Market Revenue (US$ Mn) Estimates and

Forecasts, by End-user 2020 - 2033

7.1.1.Veterinary Hospitals &

Clinics

7.1.2.Home Care Settings

8. Global

Veterinary Point of Care Diagnostics Market

Estimates & Forecast Trend Analysis, by region

8.1.

Global

Veterinary Point of Care Diagnostics Market Revenue (US$ Mn) Estimates and

Forecasts, by region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Veterinary

Point of Care Diagnostics Market:

Estimates & Forecast Trend Analysis

9.1.

North

America Veterinary Point of Care Diagnostics Market Assessments & Key

Findings

9.1.1.North America Veterinary

Point of Care Diagnostics Market Introduction

9.1.2.North America Veterinary

Point of Care Diagnostics Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

9.1.2.1. By Product

9.1.2.2. By Technology

9.1.2.3. By Animal

Type

9.1.2.4. By End-user

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Veterinary

Point of Care Diagnostics Market:

Estimates & Forecast Trend Analysis

10.1.

Europe

Veterinary Point of Care Diagnostics Market Assessments & Key Findings

10.1.1.

Europe

Veterinary Point of Care Diagnostics Market Introduction

10.1.2.

Europe

Veterinary Point of Care Diagnostics Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product

10.1.2.2. By Technology

10.1.2.3. By Animal

Type

10.1.2.4. By End-user

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Veterinary

Point of Care Diagnostics Market:

Estimates & Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Veterinary Point of Care Diagnostics Market Introduction

11.1.2.

Asia

Pacific Veterinary Point of Care Diagnostics Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

11.1.2.1. By Product

11.1.2.2. By Technology

11.1.2.3. By Animal

Type

11.1.2.4. By End-user

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Veterinary

Point of Care Diagnostics Market:

Estimates & Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Veterinary Point of Care Diagnostics

Market Introduction

12.1.2.

Middle East & Africa Veterinary Point of Care Diagnostics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

12.1.2.2. By Technology

12.1.2.3. By Animal

Type

12.1.2.4. By End-user

12.1.2.5.

By

Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Veterinary Point of Care Diagnostics Market: Estimates & Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Veterinary Point of Care Diagnostics Market Introduction

13.1.2.

Latin

America Veterinary Point of Care Diagnostics Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

13.1.2.1. By Product

13.1.2.2. By Technology

13.1.2.3. By Animal

Type

13.1.2.4. By End-user

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Veterinary Point of Care Diagnostics Market Product Mapping

15.2.

Global

Veterinary Point of Care Diagnostics Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

15.3.

Global

Veterinary Point of Care Diagnostics Market Tier Structure Analysis

15.4.

Global

Veterinary Point of Care Diagnostics Market Concentration & Company Market

Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

IDEXX Laboratories, Inc.

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2. Zoetis Inc.

16.3. Thermo Fisher

Scientific Inc.

16.4. Heska

Corporation (Part of Mars, Inc.)

16.5. Virbac

16.6. bioMérieux SA

(via its subsidiary bioMérieux Vet)

16.7. Randox

Laboratories Ltd.

16.8. Woodley

Equipment Company Ltd.

16.9. CareHealth

America Corporation

16.10. Eurolyser

Diagnostica GmbH

16.11. NeuroLogica

Corp. (A Samsung Electronics Company)

16.12. Shenzhen

Mindray Animal Medical Technology Co., Ltd.

16.13. Henry Schein,

Inc.

16.14. Abaxis

16.15. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables