Virtual Companion Care Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Service Type (Video Service, Voice Service, Others), By End User (Long-term Care Centers, Home Care Settings, Rehabilitation Centers, Others), And Geography

2025-12-30

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Virtual

Companion Care Market Overview

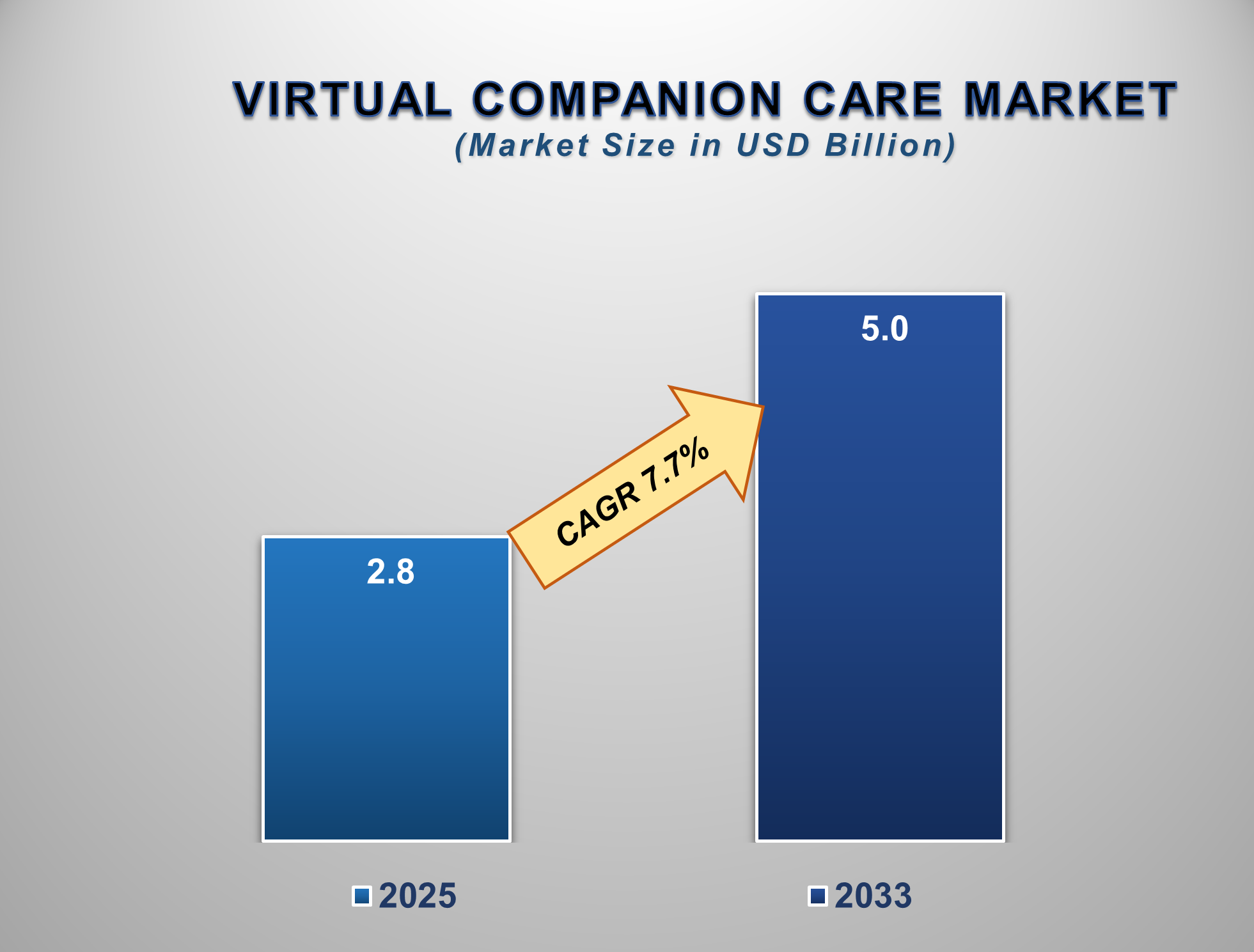

The global Virtual Companion Care Market is poised for exceptional growth from 2025 to 2033, driven by a rapidly aging global population, increasing societal focus on mental health and social isolation, and significant technological advancements in telehealth and artificial intelligence. The market was estimated at USD 2.8 billion in 2024 and is projected to reach USD 5.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 7.7% during this period.

Virtual companion care refers to digital services designed

to provide individuals, particularly the elderly and those with special needs,

with emotional support, social connection, and non-clinical assistance through

technological platforms. The market's expansion is underpinned by the critical

objective of promoting independent living, combating loneliness, and extending

care beyond the clinical setting to enhance overall quality of life. A key

trend is the evolution from basic voice and video calls to AI-driven,

empathetic interactions capable of monitoring health and providing personalized

engagement. Factors such as growing acceptance of telehealth, escalating

healthcare costs, and a global shortage of caregivers are key contributors to

market growth. North America currently holds the largest market share due to

advanced healthcare infrastructure and supportive regulatory environments,

while the Asia-Pacific region is expected to be the fastest-growing market,

fueled by a massive aging demographic, rapid digitalization, and government

initiatives.

Virtual Companion Care Market Drivers and

Opportunities

Aging Global Population and Rising Demand for Accessible Care

are the Primary Market Drivers

The most significant driver for the virtual companion care

market is the unprecedented demographic shift towards an older population

worldwide. By 2050, the global elderly population is expected to double,

creating immense pressure on traditional healthcare systems and families.

Virtual companion care offers a scalable, cost-effective solution that allows

seniors to age in place safely, providing continuous companionship and

monitoring without the need for a full-time, in-person caregiver. This demand is

further amplified by a well-documented shortage of professional caregivers and

the increasing prevalence of chronic diseases that require ongoing management

and support.

Technological Integration of AI and IoT Presents a Major

Growth Vector

A powerful and defining trend is the accelerated

integration of sophisticated technologies, including Artificial Intelligence

(AI), machine learning, and Internet of Things (IoT) devices. These

technologies are transforming virtual companions from simple communication

tools into proactive, predictive support systems. AI enables natural,

empathetic conversations, emotion recognition, and adaptive learning to

personalize interactions. When combined with IoT wearables and smart home

sensors, these systems can monitor vital signs, detect falls, and automate

daily tasks, creating a holistic and intelligent care ecosystem. This evolution

significantly enhances their value proposition and opens new revenue streams.

Post-Pandemic Acceptance of Telehealth and Corporate

Expansion Creates Significant Opportunities

The COVID-19 pandemic fundamentally accelerated the

adoption of all forms of remote care and normalized digital interaction for

vulnerable populations. This lasting shift in consumer and provider behavior presents a sustained tailwind for the market. Key

opportunities for market players lie in developing multilingual platforms for

global markets, forging partnerships with major healthcare providers and

insurers to integrate services into patient management and reimbursement

models, and creating specialized offerings for chronic disease management,

post-surgery care, and mental health support to address specific, high-need

applications.

Virtual Companion Care Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.8 Billion |

|

Market Forecast in 2033 |

USD 5.0 Billion |

|

CAGR % 2025-2033 |

7.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Service Type ●

By End-User |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Virtual Companion Care Market Report Segmentation

Analysis

The global Virtual

Companion Care Market is segmented by Service Type and End-user Region.

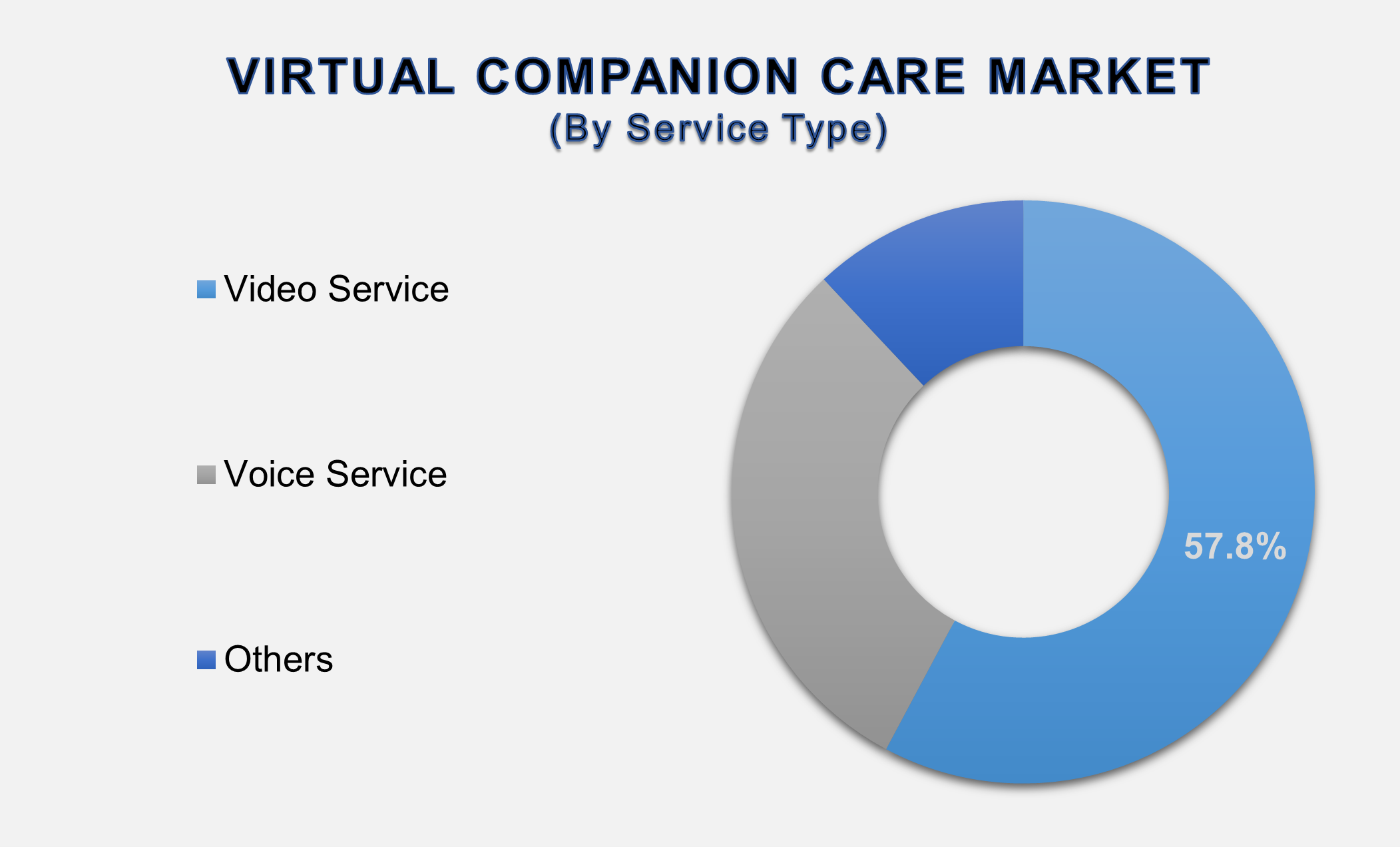

The

Video Service segment is positioned as both the largest and fastest-growing

category within the virtual companion care market due to its unparalleled

ability to deliver high-fidelity, emotionally resonant support. Unlike voice or

text-based services, live video facilitates genuine face-to-face interaction,

enabling caregivers and family members to observe a senior's physical

condition, living environment, and non-verbal cues—critical elements for holistic well-being and safety monitoring.

This visual component allows for proactive health checks, such as noticing changes in mobility, signs of potential falls, or fluctuations in general appearance that might indicate a health issue, turning a simple check-in into a valuable wellness assessment. The widespread proliferation of high-speed broadband and 5G, coupled with the mass adoption of intuitive video platforms during the COVID-19 pandemic, has normalized this technology for older adults and their support networks. Consequently, video service has evolved from a supplementary communication tool into the foundational medium for remote companionship and care, offering a scalable solution that effectively bridges geographical distance while preserving the human connection essential for combating social isolation and promoting mental health.

The Home Care Settings

Segment dominates the virtual companion care market

The

Home Care Settings segment is the cornerstone and dominant end-user of the

virtual companion care market, fundamentally driven by the powerful and nearly

universal preference among seniors for "aging in place." This trend

reflects a deep-seated desire to maintain independence, dignity, and comfort

within one's own familiar environment for as long as possible, rather than

transitioning to an institutional setting. Virtual companion care serves as a

critical technological enabler of this preference, offering a compelling and

cost-effective alternative to full-time, in-person caregiving.

By

providing scheduled and on-demand video check-ins, medication reminders, and

social engagement, these platforms directly address key challenges of living

alone, such as loneliness and safety concerns. For family members and

professional care coordinators, virtual services deliver indispensable peace of

mind through remote monitoring capabilities, allowing them to verify well-being

and intervene proactively if needed. This capability not only enhances the

quality of life for the senior but also acts as a powerful tool to delay or

reduce the need for more expensive and disruptive institutional care, aligning

perfectly with both personal desires and broader healthcare system goals

focused on reducing hospitalization and long-term care facility admissions.

The following segments are

part of an in-depth analysis of the global Virtual Companion Care Market:

|

Market

Segments |

|

|

By Service

Type |

●

Video Service ●

Voice Service ●

Others |

|

By

End-user |

●

Long-term Care

Centers ●

Home Care Settings ●

Rehabilitation

Centers ●

Others |

Virtual Companion Care Market Share Analysis by

Region

The North America region

is anticipated to hold the largest portion of the Virtual Companion Care Market

globally throughout the forecast period.

North

America's dominance is attributed to its advanced technological infrastructure,

high healthcare expenditure, and a mature telehealth regulatory framework that

facilitates reimbursement. The region has a high concentration of innovative

technology companies and healthcare providers who are early adopters of digital

health solutions. A significant aging population with growing disposable income

further drives demand, solidifying the region's leadership. The Asia-Pacific

region is poised to be the fastest-growing market, driven by its rapidly

expanding elderly population, particularly in countries like Japan and China,

coupled with improving digital connectivity and supportive government policies

promoting home-based care. Rising healthcare costs and a cultural emphasis on

family care are also accelerating the search for technological solutions to

support caregivers, creating a fertile ground for market expansion.

Virtual Companion Care Market Competition

Landscape Analysis

The global virtual companion

care market is fragmented and evolving, featuring a diverse mix of healthcare

technology firms, established medical device companies, telecommunications

giants, and innovative startups. Competition centers on technological sophistication

(especially AI capabilities), user experience, integration with broader

healthcare ecosystems, and the ability to form strategic partnerships with

insurers and care providers. Key strategies include heavy investment in R&D

for emotion-aware AI, forming alliances with hardware manufacturers for

integrated device solutions, and geographic expansion to capture growth in

underserved but populous regions like the Asia-Pacific.

Global Virtual Companion Care Market Recent Developments

News:

- In May 2025, Microsoft announced a strategic partnership with Elder

Care Technologies to integrate AI-powered companion features into Windows

and Azure for elder-care solutions.

- In June 2025, Google announced a collaboration with Intuition

Robotics to co-develop AI-assisted elder-care tools for Google Cloud and

Android devices.

- In April 2025, Amazon announced the launch of a home care assistant

robot integrated with Alexa for remote elder-care support.

- In March 2021, HealthTap, a virtual healthcare service provider,

announced the expansion of its primary care service in virtual mode,

starting in seven U.S. states.

The Global Virtual Companion Care Market Is

Dominated by a Few Large Companies, such as

●

Claris Healthcare Inc.

●

General Electric

Company (GE Healthcare)

●

AT&T Inc.

●

Koninklijke Philips NV.

●

GeriJoy Limited

●

UnitedHealth Group

(United HealthCare Services)

●

Amazon.com, Inc.

●

Apple Inc.

●

Google LLC (Alphabet

Inc.)

●

Microsoft Corporation

●

Intuition Robotics

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Virtual Companion

Care Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Virtual Companion Care Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Virtual Companion

Care Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Service Type of Global Virtual

Companion Care Market

1.3.2.End-user of Global Virtual

Companion Care Market

1.3.3.Region of Global Virtual

Companion Care Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Virtual Companion Care Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Virtual Companion Care Market Estimates

& Forecast Trend Analysis, by Service Type

4.1.

Global

Virtual Companion Care Market Revenue (US$ Bn) Estimates and Forecasts, by Service

Type, 2020 - 2033

4.1.1.Video Service

4.1.2.Voice Service

4.1.3.Others

5. Global

Virtual Companion Care Market Estimates

& Forecast Trend Analysis, by End-user

5.1.

Global

Virtual Companion Care Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

5.1.1.Long-term Care Centers

5.1.2.Home Care Settings

5.1.3.Rehabilitation Centers

6. Global

Virtual Companion Care Market Estimates

& Forecast Trend Analysis, by region

6.1.

Global

Virtual Companion Care Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Virtual

Companion Care Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Virtual Companion Care Market Assessments & Key Findings

7.1.1.North America Virtual

Companion Care Market Introduction

7.1.2.North America Virtual

Companion Care Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Service

Type

7.1.2.2. By End-user

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Virtual

Companion Care Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Virtual Companion Care Market Assessments & Key Findings

8.1.1.Europe Virtual Companion

Care Market Introduction

8.1.2.Europe Virtual Companion

Care Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Service

Type

8.1.2.2. By End-user

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Virtual

Companion Care Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Virtual

Companion Care Market Introduction

9.1.2.Asia Pacific Virtual

Companion Care Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Service

Type

9.1.2.2. By End-user

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Virtual

Companion Care Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Virtual Companion Care Market

Introduction

10.1.2.

Middle East & Africa Virtual Companion Care Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Service

Type

10.1.2.2. By End-user

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Virtual Companion Care Market:

Estimates & Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Virtual Companion Care Market Introduction

11.1.2.

Latin

America Virtual Companion Care Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Service

Type

11.1.2.2. By End-user

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Virtual Companion Care Market Product Mapping

13.2.

Global

Virtual Companion Care Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

13.3.

Global

Virtual Companion Care Market Tier Structure Analysis

13.4.

Global

Virtual Companion Care Market Concentration & Company Market Shares (%)

Analysis, 2024

14.

Company

Profiles

14.1.

Claris Healthcare Inc.

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. General

Electric Company (GE Healthcare)

14.3. AT&T Inc.

14.4. Koninklijke

Philips N.V.

14.5. GeriJoy

Limited

14.6. UnitedHealth

Group (United HealthCare Services)

14.7. Amazon.com, Inc.

14.8. Apple Inc.

14.9. Google LLC

(Alphabet Inc.)

14.10. Microsoft

Corporation

14.11. Intuition

Robotics

14.12. Other

Prominent Players

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables