Web Content Filtering Market Size and Forecast (2026–2034): Global and Regional Growth Trends, Market Share, and Industry Analysis Report by Component (Solutions, Services); Deployment Mode (Cloud, On-premise); Organization Size (Small & Medium Enterprises, Large Enterprises); Application (Network Security, Policy Enforcement, Malware Protection, Data Protection); End-use Industry (IT & Telecom, BFSI, Government, Education, Healthcare, and Others); and Geography

2026-03-12

ICT

Ekta Chaurasia (Team Lead)

Description

Web Content Filtering Market Overview

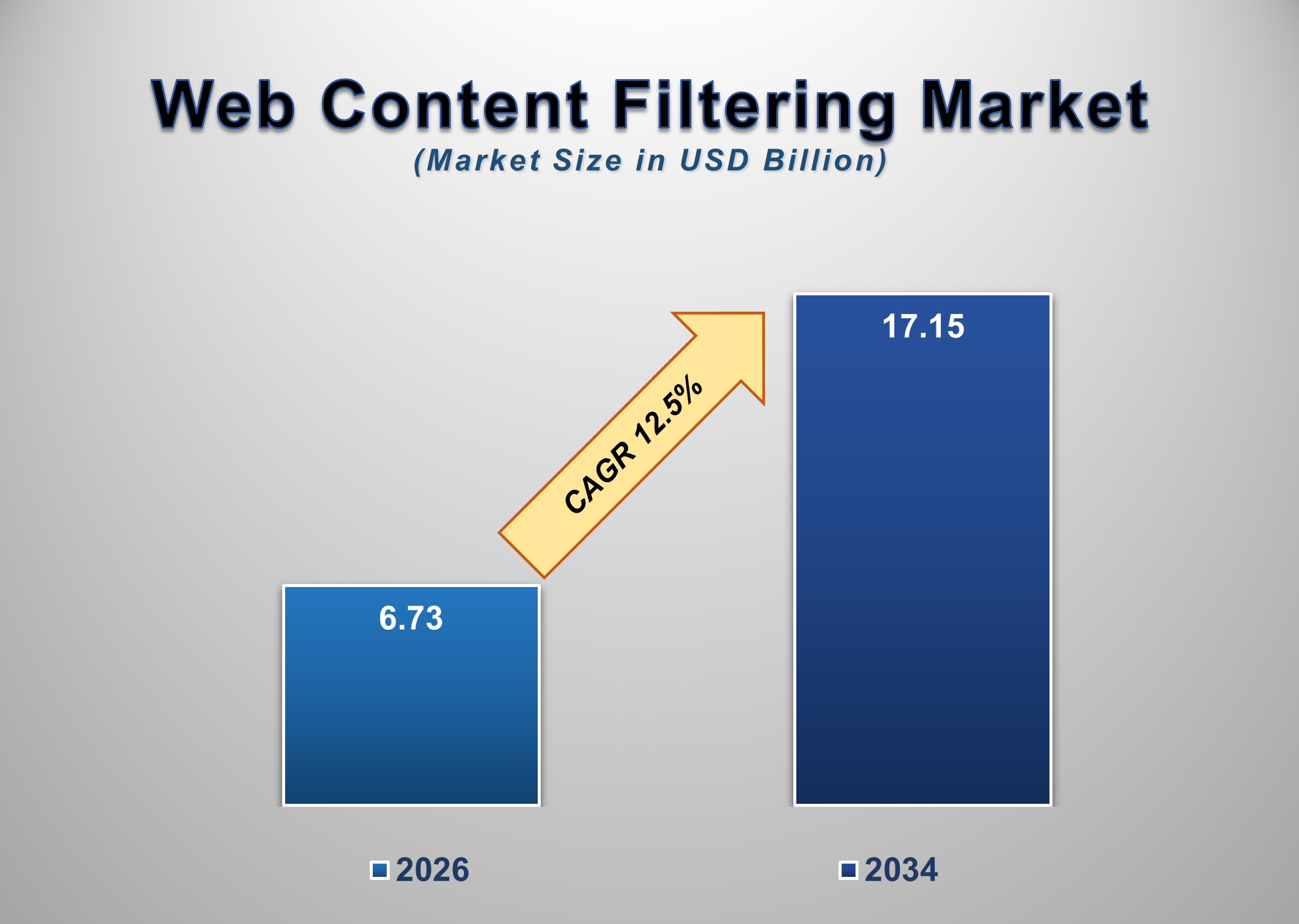

The global Web Content Filtering Market is experiencing steady expansion as organizations increasingly prioritize internet security, employee productivity management, and regulatory compliance. The market is estimated to reach USD 6.73 billion in 2026 and is projected to grow to USD 17.15 billion by 2034, registering a compound annual growth rate (CAGR) of 12.5% during the forecast period. Rising cybersecurity concerns, growing internet usage within enterprises, and increasing adoption of secure web gateways are key factors driving the growth of the web content filtering market worldwide.

Web content filtering refers to a set of technologies designed to monitor, restrict, and manage internet access based on predefined policies or security rules. These solutions allow organizations to block harmful or inappropriate websites, prevent access to malicious content, and enforce corporate internet usage policies. Web filtering technologies analyze URLs, keywords, IP addresses, and website categories to determine whether a user should be granted or denied access to specific online resources.

With the rapid expansion of digital workplaces and remote working environments, organizations are increasingly relying on secure internet access solutions to protect their networks from cyber threats such as phishing attacks, malware downloads, and unauthorized data transfers. Web content filtering tools are widely used in enterprise environments, educational institutions, government organizations, and healthcare systems to ensure safe browsing practices and maintain network security.

Additionally, the increasing adoption of cloud computing, mobile devices, and distributed IT infrastructures has made it more challenging for organizations to monitor internet activity across their networks. Modern web content filtering platforms integrate advanced capabilities such as real-time threat detection, artificial intelligence-driven analytics, and policy-based access controls. These features enable organizations to protect sensitive information, enhance cybersecurity frameworks, and ensure compliance with regulatory standards related to internet usage and data protection.

Web Content Filtering Market Drivers and Opportunities

Rising Cybersecurity Threats and Malicious Online Content Are Driving Market Growth

The increasing frequency and sophistication of cyber threats represent one of the primary drivers of the global web content filtering market. Modern organizations face constant risks from malware, ransomware, phishing attacks, and malicious websites designed to exploit system vulnerabilities. Many cyberattacks originate from compromised web pages or deceptive online platforms that trick users into downloading harmful software or revealing sensitive information.

Web content filtering solutions play a critical role in preventing such attacks by blocking access to malicious domains and suspicious websites before users can interact with them. These solutions rely on continuously updated threat intelligence databases and advanced scanning technologies to identify harmful web content. By analyzing URLs, website reputations, and embedded scripts, web filtering tools help organizations prevent security breaches and reduce the risk of malware infections.

Furthermore, businesses are increasingly adopting comprehensive cybersecurity frameworks that include web filtering as a key component of their network defense strategies. As cybercriminals continue to exploit web-based vulnerabilities, organizations are expected to increase their investments in web security solutions, thereby driving the demand for advanced content filtering technologies.

Growing Adoption of Internet Usage Policies in Enterprises

Enterprises worldwide are implementing strict internet usage policies to improve employee productivity, protect company resources, and prevent misuse of corporate networks. Unrestricted internet access can lead to productivity losses, bandwidth consumption issues, and increased exposure to cybersecurity threats. Web content filtering tools allow organizations to enforce internet access policies by blocking non-work-related websites such as social media platforms, entertainment sites, and gambling portals.

These solutions also help organizations monitor employee browsing activities and generate detailed reports on internet usage patterns. By analyzing this data, IT administrators can identify potential security risks, optimize bandwidth allocation, and ensure compliance with corporate policies. Educational institutions and government agencies also rely heavily on web filtering technologies to prevent access to inappropriate content and maintain safe digital environments.

As remote and hybrid work models become more prevalent, companies must manage internet usage across distributed networks and remote devices. Web content filtering solutions provide centralized management capabilities that allow administrators to apply security policies across multiple endpoints, including laptops, mobile devices, and cloud applications. This growing need for effective internet usage control is expected to drive the adoption of web content filtering solutions across various industries.

Integration with Cloud Security Platforms Creates New Opportunities

The increasing adoption of cloud-based security solutions presents significant opportunities for the web content filtering market. Traditional web filtering systems were typically deployed within on-premise network environments; however, the rapid migration of enterprise applications to cloud platforms has created a demand for cloud-based web filtering solutions that can protect users regardless of their location.

Cloud-based web content filtering platforms provide scalable and flexible security capabilities that allow organizations to monitor internet activity across remote networks, branch offices, and mobile devices. These platforms integrate with secure web gateways (SWG), cloud access security brokers (CASB), and zero-trust network access (ZTNA) solutions to deliver comprehensive protection against web-based threats.

Moreover, the integration of artificial intelligence and machine learning technologies within web filtering platforms enables advanced threat detection and automated policy enforcement. AI-driven analytics can identify suspicious browsing patterns, detect emerging threats, and automatically block harmful websites in real time. As organizations continue to adopt cloud-based IT infrastructures and remote work environments, the demand for cloud-native web content filtering solutions is expected to increase substantially.

Web Content Filtering Market Scope

Web Content Filtering Market Report Segmentation Analysis

The global web content filtering market industry analysis is segmented based on component, deployment model, organization size, application area, end-use industry, and geographic region.

Solutions Segment Dominates the Market

Based on component, the market is divided into solutions and services. The solutions segment currently holds the largest share because most organizations primarily invest in web filtering software platforms that monitor internet activity and block unauthorized web content. These solutions are designed to provide real-time website filtering, malware protection, and policy enforcement capabilities across enterprise networks.

Modern web filtering solutions incorporate advanced technologies such as artificial intelligence, machine learning, and behavioral analytics to detect malicious websites and suspicious browsing patterns. These capabilities enable organizations to enhance their cybersecurity frameworks and ensure safe internet usage within corporate environments.

Cloud Deployment Is Experiencing Rapid Growth

In terms of deployment models, the market is segmented into cloud-based and on-premise solutions. While many traditional enterprises still rely on on-premise filtering systems to maintain direct control over network security infrastructure, cloud-based deployment is experiencing rapid growth due to its scalability and flexibility.

Cloud-based web filtering platforms allow organizations to enforce security policies across distributed networks and remote devices without requiring complex hardware installations. These solutions are particularly beneficial for organizations with remote workforces, branch offices, and mobile employees.

IT & Telecom Sector Leads the End-use Segment

Among end-use industries, the IT & telecom sector accounts for the largest share of the web content filtering market. Technology companies and telecommunications providers operate extensive digital infrastructures that require continuous monitoring to prevent cyber threats and ensure secure internet access.

These organizations rely on web filtering solutions to block malicious websites, prevent data leakage, and protect network infrastructure from cyberattacks. Additionally, telecom companies often deploy web filtering systems to comply with government regulations and provide safe internet access services to their customers.

Web Content Filtering Market Share Analysis by Region

North America currently holds the largest share of the global web content filtering market due to strong cybersecurity awareness, advanced digital infrastructure, and the presence of major technology companies. Organizations in the United States and Canada have adopted comprehensive cybersecurity frameworks that include web filtering technologies to protect their networks from web-based threats.

Europe represents another significant market for web content filtering solutions. Governments and enterprises across the region are implementing strict data protection regulations and cybersecurity policies that require advanced internet monitoring technologies. Countries such as Germany, the United Kingdom, and France are investing heavily in digital security infrastructure to protect critical systems and data assets.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Rapid digitalization, increasing internet penetration, and expanding enterprise IT infrastructure in countries such as China, India, Japan, and South Korea are driving strong demand for web security solutions. Organizations in these countries are increasingly adopting web filtering technologies to safeguard their networks and maintain secure digital environments.

Global Web Content Filtering Market Recent Developments News

● In March 2025, Cisco introduced a new cloud-based secure web gateway platform with advanced content filtering and threat detection capabilities.

● In October 2024, Symantec expanded its enterprise web security portfolio with enhanced AI-powered web filtering features designed to detect emerging cyber threats.

● In July 2024, Fortinet launched an upgraded web security solution integrating DNS filtering and cloud-based content monitoring technologies.

Competitive Landscape

Major companies operating in the global Web Content Filtering Market include:

● Cisco Systems

● Broadcom (Symantec)

● Fortinet

● Palo Alto Networks

● Trend Micro

● McAfee

● Barracuda Networks

● Sophos

● Forcepoint

● Zscaler

● Check Point Software Technologies

● Kaspersky

● Webroot

● TitanHQ

● DNSFilter

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Global Web Content Filtering Market Introduction and Market Overview

Objectives of the Study

Market Segmentation

Component of Global Web Content Filtering Market

Deployment of Global Web Content Filtering Market

Organization Size of Global Web Content Filtering Market

Application of Global Web Content Filtering Market

End-use Industry of Global Web Content Filtering Market

Region of Global Web Content Filtering Market

Competition Coverage List of Market Participants

Market Definition: Web Content Filtering Market

Executive Summary

Global Web Content Filtering Market Estimation & Forecast

Global Web Content Filtering Market Size (US$ Million) Estimates & Historical Trend Analysis (2021 - 2025)

Global Web Content Filtering Overall Market Size (US$ Million), Growth Rate (Y-o-Y), Market CAGR (%), Market Forecast (2025 - 2033)

Snapshot of Global Web Content Filtering Market

Global Web Content Filtering Market Revenue Share (%) 2025

REGIONAL OUTLINE: Revenue CAGR, by Region

Key Competitors & Key Insights

Market Overview (Qualitative Analysis)

Demand Side Trends

Supply Side Trends / Manufacturing Trends

Demand and Opportunity Assessment, 2025 - 2033

Market Dynamics

Drivers

Limitations

Opportunities

Impact Analysis of Drivers and Restraints

Key Developments

Regulatory Landscape

Pricing Analysis

Value Chain / Ecosystem Analysis

Porter’s Five Forces Analysis

Bargaining Power of Suppliers

Bargaining Power of Buyers

Threat of Substitutes

Threat of New Entrants

Competitive Rivalry

PEST Analysis

Political Factors

Economic Factors

Social Factors

Technology Factors

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by Component

Global Web Content Filtering Market Assessments & Key Findings, by Component

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by Component, 2021 - 2033

Solutions

URL Filtering Solutions

DNS Filtering Platforms

Secure Web Gateway Systems

Content Monitoring Tools

Services

Consulting Services

Integration Services

Support & Maintenance Services

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by Deployment

Global Web Content Filtering Market Assessments & Key Findings, by Deployment

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by Deployment, 2021 - 2033

Cloud

On-premise

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by Organization Size

Global Web Content Filtering Market Assessments & Key Findings, by Organization Size

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by Organization Size, 2021 - 2033

Small & Medium Enterprises

Large Enterprises

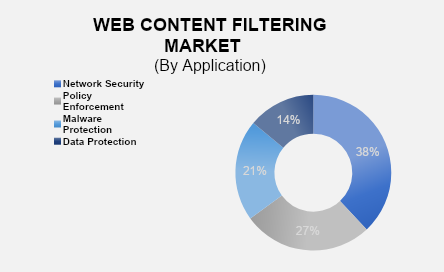

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by Application

Global Web Content Filtering Market Assessments & Key Findings, by Application

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by Application, 2021 - 2033

Network Security

Policy Enforcement

Malware Protection

Data Protection

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by End-use Industry

Global Web Content Filtering Market Assessments & Key Findings, by End-use Industry

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by End-use Industry, 2021 - 2033

IT & Telecom

BFSI

Government

Education

Healthcare

Others

Global Web Content Filtering Market Estimates & Forecast Trend Analysis, by Region

Global Web Content Filtering Market Assessments & Key Findings, by Region

Global Web Content Filtering Market Revenue (US$ Million) Estimates and Forecasts, by Region, 2021 - 2033

North America

Europe

Asia Pacific

Middle East & Africa

Latin America

North America Web Content Filtering Market: Estimates & Forecast Trend Analysis

North America Web Content Filtering Market Assessments & Key Findings

North America Web Content Filtering Market Introduction

North America Web Content Filtering Market Size Estimates and Forecast (US$ Million) (2021 - 2033)

By Component

By Deployment

By Organization Size

By Application

By End-use Industry

By Country

The U.S.

Canada

Europe Web Content Filtering Market: Estimates & Forecast Trend Analysis

Europe Web Content Filtering Market Assessments & Key Findings

Europe Web Content Filtering Market Introduction

Europe Web Content Filtering Market Size Estimates and Forecast (US$ Million) (2021 - 2033)

By Component

By Deployment

By Organization Size

By Application

By End-use Industry

By Country

Germany

Italy

U.K.

France

Spain

Switzerland

Rest of Europe

Asia Pacific Web Content Filtering Market: Estimates & Forecast Trend Analysis

Asia Pacific Market Assessments & Key Findings

Asia Pacific Web Content Filtering Market Introduction

Asia Pacific Web Content Filtering Market Size Estimates and Forecast (US$ Million) (2021 - 2033)

By Component

By Deployment

By Organization Size

By Application

By End-use Industry

By Country

China

Japan

India

Australia

South Korea

Rest of Asia Pacific

Middle East & Africa Web Content Filtering Market: Estimates & Forecast Trend Analysis

Middle East & Africa Market Assessments & Key Findings

Middle East & Africa Web Content Filtering Market Introduction

Middle East & Africa Web Content Filtering Market Size Estimates and Forecast (US$ Million) (2021 - 2033)

By Component

By Deployment

By Organization Size

By Application

By End-use Industry

By Country

South Africa

UAE

Saudi Arabia

Rest of MEA

Latin America Web Content Filtering Market: Estimates & Forecast Trend Analysis

Latin America Market Assessments & Key Findings

Latin America Web Content Filtering Market Introduction

Latin America Web Content Filtering Market Size Estimates and Forecast (US$ Million) (2021 - 2033)

By Component

By Deployment

By Organization Size

By Application

By End-use Industry

By Country

Brazil

Mexico

Argentina

Rest of LATAM

Competition Landscape

Global Web Content Filtering Market Product Mapping

Global Web Content Filtering Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

Global Web Content Filtering Market Tier Structure Analysis

Global Web Content Filtering Market Concentration & Company Market Shares (%) Analysis, 2025

Company Profiles

Cisco Systems

Company Overview & Key Stats

Financial Performance & KPIs

Product Portfolio

SWOT Analysis

Business Strategy & Recent Developments

Similar details would be provided for all the players mentioned below *

Broadcom (Symantec)

Fortinet

Palo Alto Networks

Trend Micro

McAfee

Barracuda Networks

Sophos

Forcepoint

Zscaler

Check Point Software Technologies

Kaspersky

Webroot

TitanHQ

DNSFilter

Other Prominent Players

Research Findings & Conclusion

Assumptions & Acronyms Used

Research Methodology

External Databases

Internal Proprietary Database

Primary Research

Secondary Research

Assumptions

Limitations

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables