Wireless Infrastructure Market Size and Forecast (2026-2034), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Component (Hardware, Software, Services), Technology (4G LTE, 5G, Small Cells, Wi-Fi 6/6E/7), End Use (Telecom Operators, Enterprises, Government & Public Safety, Others), and Geography

2026-03-11

ICT

Ekta Chaurasia (Team Lead)

Description

Wireless Infrastructure Market Overview

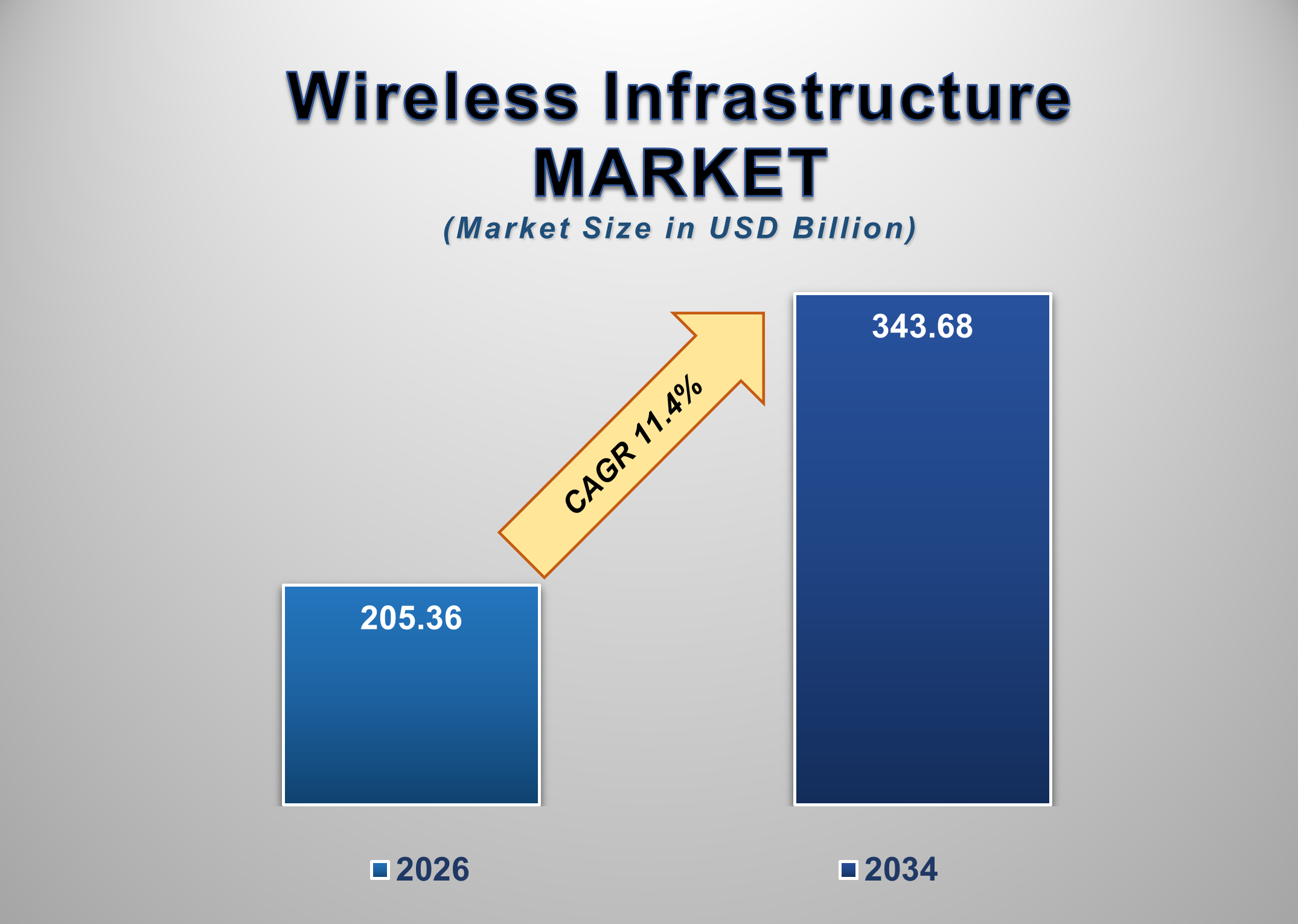

The global wireless infrastructure market is undergoing transformative growth, driven by rapid mobile data traffic expansion, adoption of next-generation network technologies, and increasing demand for low-latency connectivity across industries. Valued at USD $205.36 billion in 2026, the market is projected to reach USD $343.68 billion by 2034, growing at a CAGR of 6.5% during the forecast period.

Wireless infrastructure comprises the essential hardware, software, and services required to enable wireless communication networks, including base stations, antennas, radio access networks (RAN), small cells, and network management systems. With the global shift toward 5G technology, service providers are upgrading legacy 4G LTE networks and deploying advanced hardware to support enhanced mobile broadband, ultra-reliable low-latency communications (URLLC), and massive Internet of Things (IoT) connectivity.

Mobile data traffic has surged due to video streaming, cloud services, and digital applications across consumer and enterprise segments. Telecom operators are investing heavily in densifying network coverage and enhancing capacity using small cells and distributed antenna systems (DAS), particularly in urban and enterprise environments. Additionally, Wi-Fi 6/6E/7 technologies are complementing cellular networks to support high-density user environments such as stadiums, campuses, and public venues.

Despite strong growth potential, the market faces challenges, including high capital expenditure on infrastructure rollout, spectrum licensing complexities, and technical hurdles in integrating multi-vendor technologies. Furthermore, the transition to open RAN architectures presents both uncertainties and opportunities as operators look to optimize costs and foster vendor interoperability.

Government initiatives supporting digital inclusion, smart city deployments, and Industry 4.0 applications are further accelerating market expansion across North America, Asia-Pacific, and Europe. As wireless connectivity becomes a foundational utility for economic development and digital transformation, investments in wireless infrastructure are expected to remain robust through 2033.

Wireless Infrastructure Market Drivers and Opportunities

5G Deployment & Network Modernization

The global push for 5G networks represents the most significant driver for wireless infrastructure demand. 5G offers substantially higher data rates, improved reliability, and lower latency compared to previous generations, enabling advanced applications such as autonomous vehicles, remote surgery, and industrial automation. To support 5G capabilities, wireless providers must deploy new base stations, massive MIMO antennas, and upgraded RAN components. This wave of network modernization is fueling capital expenditure across developed and emerging markets alike.

For instance, operators in the United States and South Korea have accelerated macrocell and small cell deployment to support urban 5G coverage and fixed wireless access services. Similarly, China’s aggressive 5G rollout, backed by government incentives, has scaled network infrastructure at an unprecedented pace. This sustained investment cycle continues to expand the market for 5G-compatible infrastructure hardware and supporting software.

Enterprise Digital Transformation and Private Networks

Enterprises across manufacturing, logistics, healthcare, and education are adopting private wireless networks, especially 5G and advanced Wi-Fi deployments, to enable mission-critical connectivity, automation, and real-time analytics. Private networks offer dedicated spectrum, enhanced security, and predictable performance compared to public wireless services. Wireless infrastructure vendors are offering integrated solutions tailored for smart factories, automated warehouses, and campus network deployments.

Telecom operators are also partnering with enterprises to provide managed private network services, leveraging small cells, edge computing, and network slicing capabilities. This shift from consumer-focused deployments toward enterprise use cases significantly expands infrastructure demand beyond traditional telecom applications.

Integration of Open RAN & Virtualized Network Functions

The transition toward Open Radio Access Network (Open RAN) and network function virtualization (NFV) presents a major opportunity for innovation and competitive differentiation. Open RAN decouples hardware from software, enabling multi-vendor interoperability and reducing dependency on traditional proprietary equipment. This architectural shift allows operators to adopt best-of-breed components, scale network capabilities flexibly, and optimize total cost of ownership.

Virtualization of network functions enables wireless infrastructure to be deployed on cloud-native platforms, improving agility and enabling real-time orchestration. Telecom operators in Europe and Asia-Pacific are conducting extensive Open RAN trials, collaborating with systems integrators and software vendors to pilot scalable, software-driven architectures. As Open RAN matures, it is expected to unlock new revenue streams for software providers, system integrators, and infrastructure manufacturers while lowering barriers for new entrants.

Wireless Infrastructure Market Scope

Segments Covered

Wireless Infrastructure Market Report Segmentation Analysis

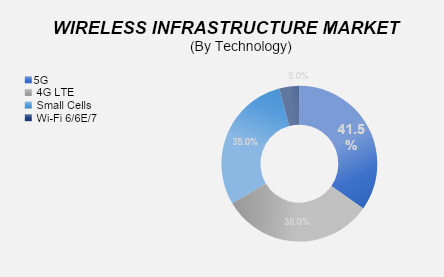

The global wireless infrastructure market analysis is segmented by component, technology, end use, and region. The 5G segment dominated the market in 2025 and is projected to sustain the highest CAGR over the forecast period.

By technology, the market comprises legacy 4G LTE networks, 5G infrastructure, small cells, and Wi-Fi technologies. 5G captured the largest share due to massive network upgrades and spectrum reallocations across major markets. 5G infrastructure requires deployment of new base stations, massive MIMO antennas, and integrated software platforms to support diverse use cases such as enhanced mobile broadband, ultra-reliable low-latency communications (URLLC), and massive IoT connections. Investment in 5G network densification and backhaul capacity continues to drive long-term demand for advanced wireless infrastructure.

End Use Segment Analysis

The Telecom Operators segment holds the highest share of the market over the forecast period.

Telecom operators are the principal buyers of wireless infrastructure equipment and services, investing heavily to expand network coverage, enhance capacity, and launch next-generation services. With the rollout of 5G and plans for future 6G evolution, operators are upgrading core and radio access networks. The need to support higher subscriber densities, growing mobile broadband usage, and enterprise private networks further reinforces operators’ central role in infrastructure procurement. Telecom operators also collaborate with infrastructure vendors and integrators to deploy optimized network solutions tailored to regional regulatory requirements and spectrum allocations.

Wireless Infrastructure Market Share Analysis by Region

Asia-Pacific is projected to hold the largest share of the global wireless infrastructure market over the forecast period.

The Asia-Pacific region accounts for a significant share due to aggressive 5G deployments in China, South Korea, and Japan, supported by government policies and large telecom operator investments. China leads global 5G base station installations, driving demand for advanced hardware, software platforms, and network services. India’s telecom infrastructure expansion and ambitious digital inclusion programs further contribute to regional growth. Additionally, rapid urbanization, digitization of industries, and adoption of advanced wireless technologies in Southeast Asian markets strengthen the Asia-Pacific’s market position.

Wireless Infrastructure Market Recent Developments News

In January 2025, Ericsson announced a strategic partnership with a major U.S. telecom operator to deploy Open RAN-aligned 5G infrastructure across key metropolitan markets.

In June 2025, Nokia launched a new suite of 5G-optimized base station hardware with built-in AI-enabled network automation capabilities for energy reduction and performance optimization.

In November 2025, Qualcomm Technologies introduced an integrated mmWave 5G small cell solution designed to accelerate densification efforts in dense urban environments.

Competitive Landscape

The Global Wireless Infrastructure Market is dominated by a few large companies, such as

Huawei Technologies Co., Ltd.

Ericsson

Nokia Corporation

Samsung Electronics Co., Ltd.

Cisco Systems, Inc.

Qualcomm Incorporated

ZTE Corporation

Motorola Solutions, Inc.

CommScope Holding Company, Inc.

American Tower Corporation

Crown Castle International Corp.

Corning Incorporated

NEC Corporation

Fujitsu Limited

Juniper Networks, Inc.

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Wireless Infrastructure Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables