Wood Protection Chemicals Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Preservatives, Flame Retardants, Water Repellents, Insecticides, Others), By Application (Residential, Commercial & Industrial), By End-Use (Construction, Furniture & Decking, Marine), And Geography

2025-12-12

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Wood

Protection Chemicals Market Overview

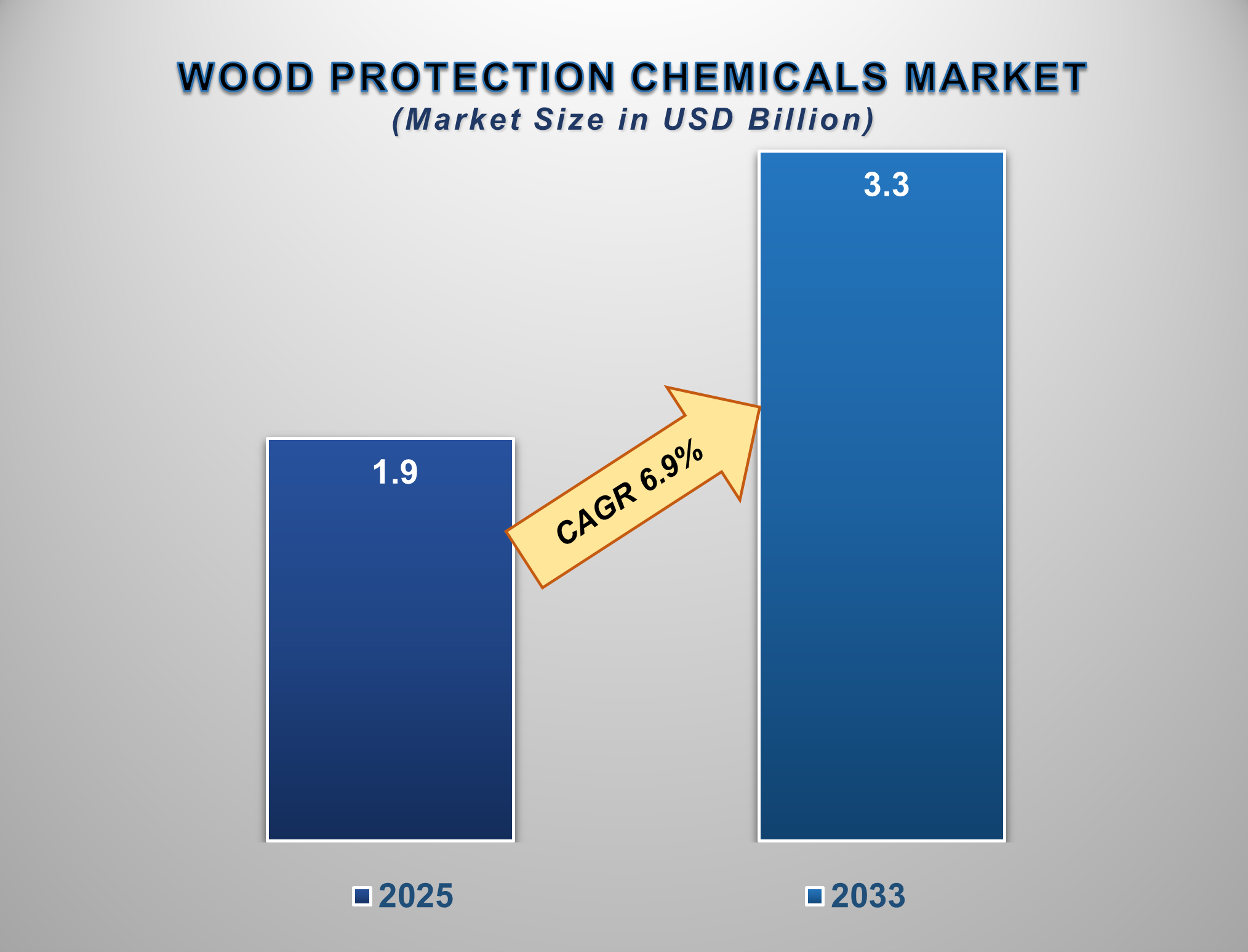

The Wood Protection Chemicals Market is set for steady growth from 2025 to 2033, driven by rising global construction activity, increasing demand for durable and sustainable building materials, and stringent fire safety regulations. The market is projected to be valued at approximately USD 1.9 billion in 2025 and is forecasted to reach nearly USD 3.3 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.9% during this period.

Wood protection chemicals are specialized

formulations designed to extend the lifespan of wood by protecting it from

biological decay (fungi, termites), moisture, fire, and UV radiation. The

market's expansion is underpinned by the growing preference for wood as a

renewable and aesthetically pleasing construction material, necessitating

treatments to enhance its performance and longevity. The construction boom in

emerging economies, coupled with the renovation and repair activities in

developed regions, is fueling demand.

Furthermore, technological advancements leading to more effective,

low-toxicity, and environmentally friendly formulations are creating new market

opportunities. North America and Europe are established markets with strict

regulatory standards, while the Asia-Pacific region is expected to witness the

fastest growth due to rapid urbanization and infrastructure development.

Wood Protection Chemicals Market Drivers and

Opportunities

Growth in Construction and Infrastructure Development is the

Primary Market Driver

The most significant driver for the wood

protection chemicals market is the robust growth in the global construction

industry, particularly in residential and commercial sectors. Wood is a

fundamental material for framing, decking, fencing, and structural components.

As construction volumes rise, so does the need to protect these investments

from degradation, ensuring structural integrity and safety. This is especially

critical in regions with high humidity, termite prevalence, or significant

rainfall, where untreated wood is highly susceptible to damage.

Stringent Fire Safety Regulations and Sustainability Trends

are Accelerating Market Growth

Increasingly stringent building codes and fire

safety regulations across the globe are mandating the use of fire-retardant-treated wood in various applications, from residential buildings

to public infrastructure. This regulatory push is a major growth factor for flame-retardant chemicals. Simultaneously, the global focus on

sustainability is driving the use of wood as a renewable and

carbon-sequestering resource. To maximize its sustainability benefits,

protecting wood to ensure a long service life is paramount, creating a

consistent demand for high-performance preservatives and coatings.

Development of Bio-Based and Hybrid Formulations Presents

Significant Opportunities

The shift towards eco-friendly and low-VOC

(Volatile Organic Compound) products represents a major growth frontier.

Significant opportunities exist in the research and development of bio-based

wood protection chemicals derived from natural sources, which offer an

effective and environmentally responsible alternative to traditional synthetic

chemicals. Additionally, the development of multi-functional hybrid

formulations that combine preservative, water-repellent, and UV-resistant

properties in a single treatment is gaining traction. For manufacturers,

investing in R&D for these advanced, sustainable, and integrated solutions

is a key strategy to capture value from environmentally conscious consumers and

industrial clients.

Wood Protection Chemicals Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 1.9 Billion |

|

Market Forecast in 2033 |

USD 3.3 Billion |

|

CAGR % 2025-2033 |

6.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Wood Protection Chemicals Market Report

Segmentation Analysis

The global Wood Protection

Chemicals Market industry analysis is segmented by Product Type, by

Application, by End-Use, and by Region.

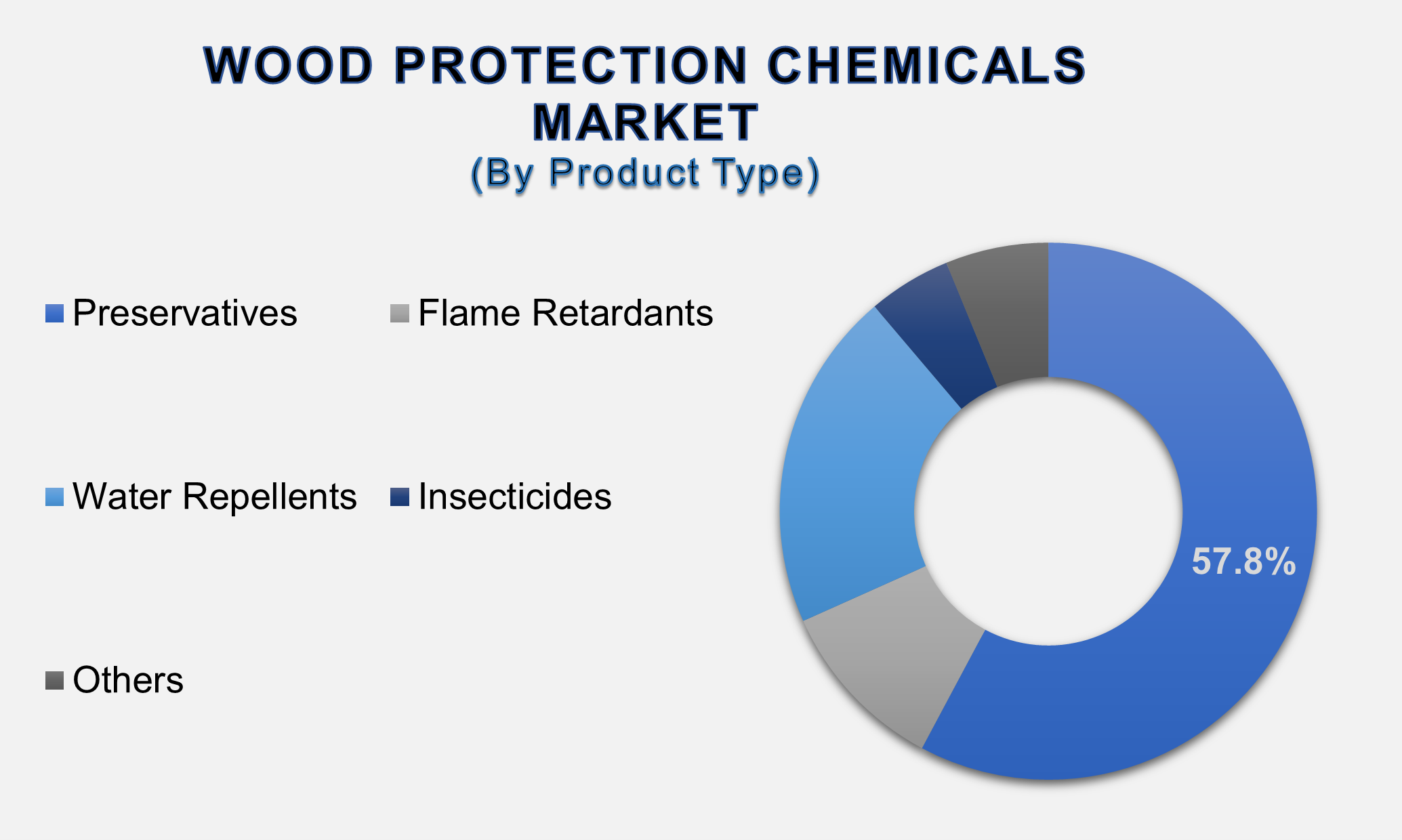

The Preservatives segment

is anticipated to command a significant market share in 2025.

The

Product Type segment is categorized into Preservatives, Flame Retardants, Water

Repellents, Insecticides, and Others. Preservatives, which protect wood from

fungal decay and insect attack, form the backbone of the market. Their

dominance is due to the fundamental need to prevent biological degradation,

which is the primary cause of wood failure in most environments. The widespread

use of pressure-treated lumber in residential construction and outdoor

applications ensures consistent and high demand for this segment.

The wood protection chemicals market relies heavily on preservatives, the dominant product segment, which are categorized by their composition and application. Water-based preservatives form the largest category, led by Alkaline Copper Quat (ACQ) and Copper Azole (CA), which use copper as a fungicide paired with other biocides to protect against decay and insects in residential applications like decking and fencing. Borates offer a low-toxicity alternative but are primarily used for interior framing, as they can leach out when exposed to weather.

For

extreme-duty industrial applications such as railroad ties and utility poles,

heavy-duty oil-based preservatives like creosote and pentachlorophenol are

employed for their superior durability and water resistance, though their use

is restricted due to environmental concerns. Light Organic Solvent

Preservatives (LOSP) are used where a clean, paintable finish is required, such

as in window frames and millwork. The market is also seeing emerging trends

with the development of systems that reduce copper content and the exploration

of bio-based alternatives derived from natural oils and extracts, driven by

growing demand for more environmentally benign and sustainable wood protection

solutions.

The Residential

application segment is projected to hold the largest market share.

The

Application segment is divided into Residential and Commercial &

Industrial. The Residential segment is the most lucrative, driven by

high-volume use of treated wood in single-family and multi-family housing

projects. Key applications include decking, fencing, sill plates, roof trusses,

and landscaping. The DIY (Do-It-Yourself) trend for home improvement projects,

such as building or refurbishing decks and fences, also contributes

significantly to the consumption of wood protection chemicals in this segment.

The Construction end-use

segment is projected to maintain its dominance.

The

Construction segment's leading position is a direct reflection of wood's

extensive use as a building material. From structural framing and sheathing to

windows, doors, and exterior cladding, wood requires protection at multiple

stages of construction. The growth in green building standards, which often favors wood for its sustainability credentials, further bolsters

the demand for protective chemicals in this sector to ensure the long-term

durability and performance of wooden structures.

The following segments are

part of an in-depth analysis of the global Wood Protection Chemicals Market:

|

Market

Segments |

|

|

By Product

Type |

●

Preservatives ●

Flame Retardants ●

Water Repellents ●

Insecticides ●

Others |

|

By Application

|

●

Residential

Application ●

Commercial

Application ●

Industrial

Application |

|

By End-use |

●

Construction ●

Furniture &

Decking ●

Marine ●

Other |

Wood Protection Chemicals Market Share Analysis

by Region

The Asia Pacific region

is anticipated to hold the largest portion of the Wood Protection Chemicals

Market globally throughout the forecast period.

Asia-Pacific's

dominance is attributed to its massive and ongoing construction and

infrastructure boom, particularly in countries like China, India, and Southeast

Asian nations. Rapid urbanization, rising disposable incomes, and government

investments in residential and commercial projects are driving unprecedented

consumption of construction materials, including treated wood. The region's

warm and humid climate in many areas also necessitates the use of wood

preservatives to prevent decay, creating a vast and growing market for these

products.

China

and India are undergoing unprecedented urban transformations, driving massive

demand for construction materials, including treated wood. China's urbanization

rate surged from about 36% in 2000 to over 65% of its population residing in

cities by 2023, a shift involving hundreds of millions of people. This has been

fueled by government initiatives and immense infrastructure investment,

creating sprawling megacities and new urban centers. Similarly, India's urban

population is projected to grow rapidly, potentially reaching over 800 million

by 2050, with its government actively promoting smart city development and

industrial corridors to manage this growth.

This

breakneck urbanization directly fuels the wood protection chemicals market. The

construction boom necessitates vast quantities of wood for everything from

concrete formwork and structural framing to interior finishes, decking, and

fencing. Furthermore, the warm, humid climates prevalent in large parts of both

countries accelerate wood decay from fungi and increase the threat of termite

infestations, making chemical treatment not just an option but a necessity for

material longevity and structural safety. Consequently, the Asia-Pacific

region, led by China and India, has become the dominant and fastest-growing

market for wood preservatives and flame retardants, as the scale of urban

development creates a sustained, high-volume demand for durable, protected

building materials.

Wood Protection Chemicals Market Competition

Landscape Analysis

The global wood protection

chemicals market is moderately consolidated and competitive, featuring a mix of

large multinational chemical corporations and specialized chemical formulators.

Competition is based on product efficacy, technological innovation, regulatory

compliance, price, and distribution network. Key strategies include heavy

investment in R&D to develop more sustainable and effective formulations;

strategic mergers and acquisitions to expand product portfolios and geographic

reach; and forming strong partnerships with wood treaters and large

construction material suppliers. Adherence to stringent environmental and

safety regulations (e.g., EPA, REACH) is critical for market participation.

Global Wood Protection

Chemicals Market Recent Developments News:

- In February 2025, LANXESS AG launched a new generation of wood

preservatives with a reduced environmental footprint, targeting the

residential decking and fencing market.

- In December 2024, Koppers Holdings Inc. completed the acquisition of

a regional wood treater to strengthen its distribution network in the

European market.

- In October 2024, BASF SE introduced a novel fire-retardant coating

for engineered wood products (like CLT) used in mass timber construction,

addressing the growing demand for tall wood buildings.

- In August 2024, a consortium of

leading manufacturers allied to

promote the use of pressure-treated wood in sustainable construction

projects, highlighting its longevity and environmental benefits.

The Global Wood

Protection Chemicals Market Is Dominated by a Few Large Companies, such as

●

BASF SE

●

LANXESS AG

●

Koppers Holdings Inc.

●

Lonza Group Ltd.

●

Arch Lonza (Lonza)

●

RPM International Inc.

(Tremco)

●

Akzo Nobel N.V.

●

The Sherwin-Williams

Company

●

PPG Industries, Inc.

●

Kurt Obermeier GmbH

& Co. KG

●

Janssen Preservation

& Protection

●

Hoover Color Corp.

●

Rio Tinto Minerals

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Wood Protection

Chemicals Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Wood Protection Chemicals Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Wood Protection

Chemicals Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Wood

Protection Chemicals Market

1.3.2.Application of Global Wood

Protection Chemicals Market

1.3.3.End-use of Global Wood

Protection Chemicals Market

1.3.4.Region of Global Wood

Protection Chemicals Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Wood Protection Chemicals Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Wood Protection Chemicals Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Wood Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Preservatives

4.1.2.Flame Retardants

4.1.3.Water Repellents

4.1.4.Insecticides

4.1.5.Others

5. Global

Wood Protection Chemicals Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Wood Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Residential Application

5.1.2.Commercial Application

5.1.3.Industrial Application

6. Global

Wood Protection Chemicals Market Estimates

& Forecast Trend Analysis, by End-use

6.1.

Global

Wood Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by End-use

2020 - 2033

6.1.1.Construction

6.1.2.Furniture & Decking

6.1.3.Marine

6.1.4.Other

7. Global

Wood Protection Chemicals Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Wood Protection Chemicals Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Wood

Protection Chemicals Market: Estimates

& Forecast Trend Analysis

8.1.

North

America Wood Protection Chemicals Market Assessments & Key Findings

8.1.1.North America Wood

Protection Chemicals Market Introduction

8.1.2.North America Wood

Protection Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Application

8.1.2.3. By End-use

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Wood

Protection Chemicals Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Wood Protection Chemicals Market Assessments & Key Findings

9.1.1.Europe Wood Protection

Chemicals Market Introduction

9.1.2.Europe Wood Protection

Chemicals Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Application

9.1.2.3. By End-use

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Wood

Protection Chemicals Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Wood Protection Chemicals Market Introduction

10.1.2.

Asia

Pacific Wood Protection Chemicals Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Application

10.1.2.3. By End-use

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Wood

Protection Chemicals Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Wood Protection Chemicals Market

Introduction

11.1.2.

Middle East & Africa Wood Protection Chemicals Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Application

11.1.2.3. By End-use

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Wood Protection Chemicals Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Wood Protection Chemicals Market Introduction

12.1.2.

Latin

America Wood Protection Chemicals Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Application

12.1.2.3. By End-use

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Wood Protection Chemicals Market Product Mapping

14.2.

Global

Wood Protection Chemicals Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Wood Protection Chemicals Market Tier Structure Analysis

14.4.

Global

Wood Protection Chemicals Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

BASF SE

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. LANXESS AG

15.3. Koppers

Holdings Inc.

15.4. Lonza Group

Ltd.

15.5. Arch Lonza

(Lonza)

15.6. RPM

International Inc. (Tremco)

15.7. Akzo Nobel

N.V.

15.8. The

Sherwin-Williams Company

15.9. PPG

Industries, Inc.

15.10. Kurt

Obermeier GmbH & Co. KG

15.11. Janssen

Preservation & Protection

15.12. Hoover Colour

Corp.

15.13. Rio Tinto

Minerals

15.14. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables