Workspace As a Service Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Desktop as a Service (DaaS), Application as a Service), By Deployment (Public Cloud, Private Cloud, Hybrid Cloud), By End-User (IT & Telecommunications, BFSI, Healthcare, Manufacturing, Government, Education, Others) And Geography

2025-11-26

Healthcare

Swetal (Research Analyst)

Description

Workspace As a Service

Market Overview

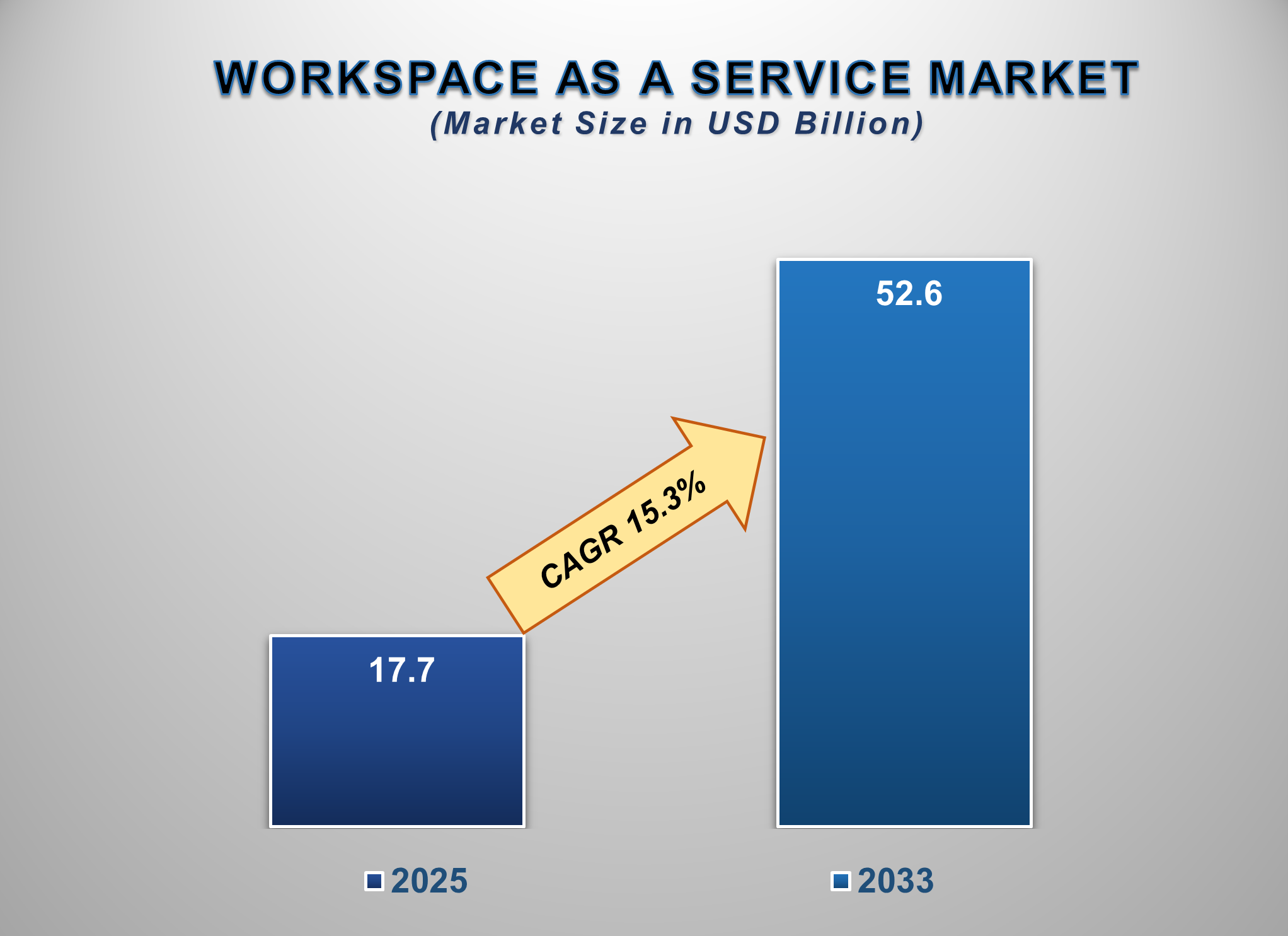

The Workspace as a Service (WaaS) market is

positioned for a period of dynamic and sustained expansion from 2025 to 2033,

fueled by the global shift towards hybrid work models, the imperative for

digital transformation, and the growing need for secure, scalable, and

cost-effective IT solutions. The market is projected to be valued at

approximately USD 17.7 billion in 2025 and is forecasted to reach nearly USD

52.6 billion by 2033, exhibiting a robust compound annual growth rate (CAGR) of

15.3% during this period.

Workspace as a Service is a cloud-based delivery model that provides a unified platform for delivering virtual desktops, applications, and data to any device, anywhere. It bundles the infrastructure, platform, and software needed to provide a complete, managed desktop experience. The market growth is primarily driven by the permanent adoption of remote and hybrid work policies, which require organizations to provide seamless and secure access to corporate resources.

Furthermore, the pressing need for business

continuity and disaster recovery, coupled with the desire to reduce capital

expenditure on hardware and simplify IT management, is creating massive demand.

Technological advancements such as the integration of advanced security

protocols like Zero Trust, improvements in virtualization technology for a

better user experience, and the adoption of AI for automated management and

performance optimization are key market enablers. North America remains the

dominant regional market due to early technology adoption and a high

concentration of WaaS providers, while the Asia-Pacific region is expected to

witness the fastest growth, driven by rapid digitalization and expanding IT

infrastructure.

Workspace As a Service Market Drivers and

Opportunities

The Permanence of Hybrid

and Remote Work Models is a Foundational Market Driving Workspace As a Service

Market

The global pandemic served as a catalyst,

fundamentally altering work culture and proving the viability of distributed

workforces. As organizations formalize long-term hybrid work strategies, WaaS

has become a critical enabler. It provides the agility, security, and

consistent user experience required to support a workforce that is no longer

tethered to a physical office. WaaS solutions allow employees to access their

personalized digital workspace from any location or device, ensuring

productivity and collaboration without compromising on security or IT control.

This structural shift in how and where work is done ensures a sustained,

non-discretionary demand for WaaS solutions.

The Imperative for

Enhanced Security and Business Continuity is a Primary Growth Engine

With the perimeter of the corporate network

dissolving, securing endpoints and data has become a top priority. WaaS offers

a more secure alternative to traditional distributed computing models by

centralizing data and applications in the cloud or a secure data center, rather

than on vulnerable endpoint devices. This significantly reduces the risk of

data loss and mitigates threats from malware and ransomware. Furthermore, WaaS

provides inherent business continuity and disaster recovery capabilities. In the

event of a local outage or disruption, employees can instantly reconnect to

their virtual workspace from an alternate location, minimizing downtime and

ensuring operational resilience. This security and continuity value proposition

is a powerful driver, especially for regulated industries like BFSI and

healthcare.

Digital Transformation

and the Shift to OPEX Models Present Significant Opportunities

The overarching trend of digital transformation,

where businesses are modernizing their IT estates for greater agility, is

creating fertile ground for WaaS adoption.

WaaS aligns perfectly with the shift from Capital Expenditure (CAPEX) to

Operational Expenditure (OPEX), allowing organizations to pay a predictable

subscription fee instead of making large upfront investments in hardware refresh

cycles. This opportunity is further amplified by the development of more

specialized and performance-optimized WaaS offerings. Key areas of innovation

include the emergence of GPU-powered DaaS for power users in engineering and

design, the integration of unified communications and collaboration tools

directly into the workspace, and the use of analytics to provide insights into

user experience and resource utilization, enabling proactive management and

cost optimization.

Workspace As a Service Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 17.7 Billion |

|

Market Forecast in 2033 |

USD 52.6 Billion |

|

CAGR % 2025-2033 |

15.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Application Analysis, Company Market Share,

Company Heatmap, Regulatory Landscape, Growth Factors and more |

|

Segments Covered |

●

By Type ●

By Deployment ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Workspace As a Service Market Report Segmentation Analysis

The global Workspace as a Service

market industry analysis is segmented by Type, by Deployment, by End-User, and

by Region.

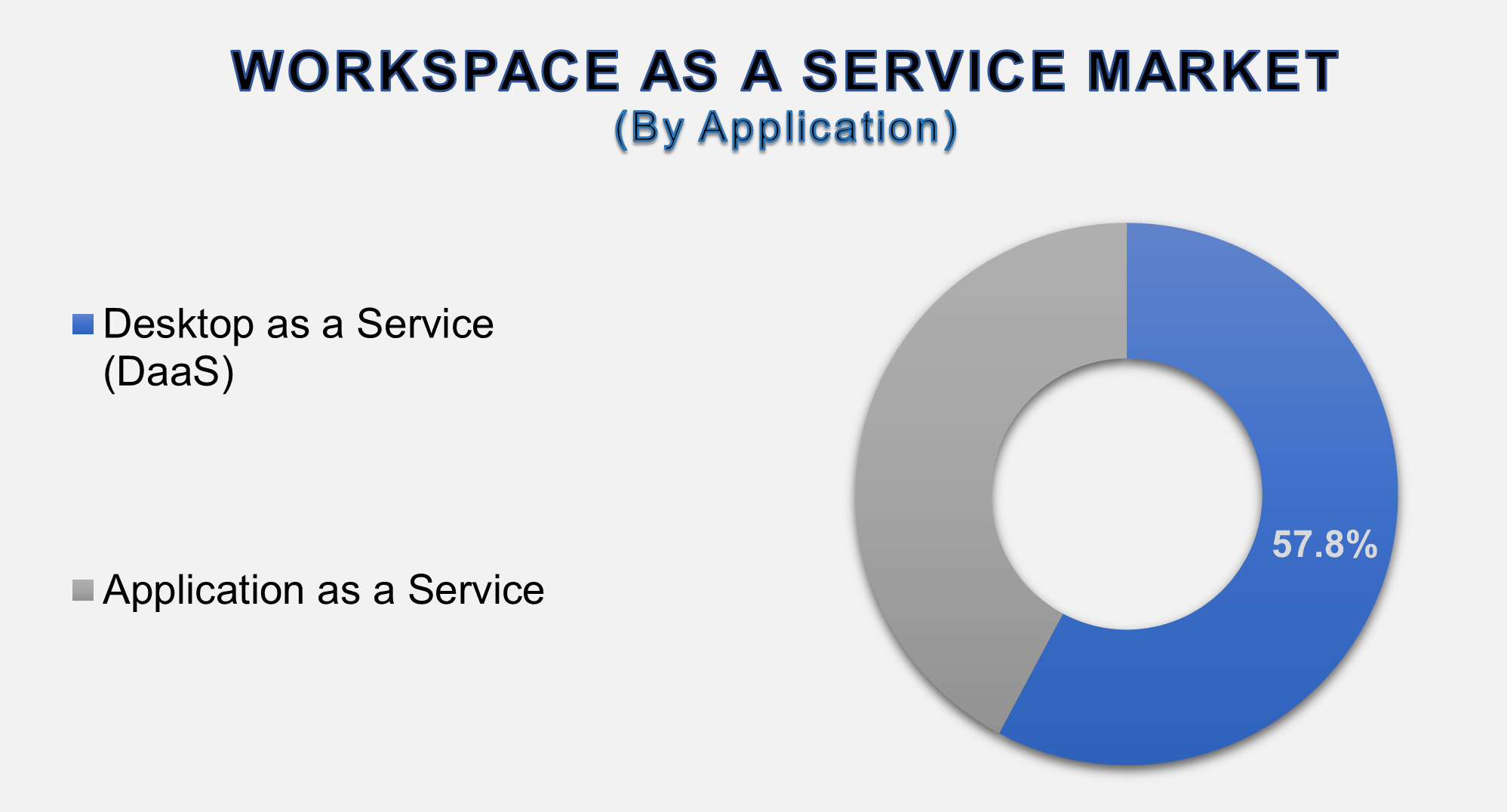

The Desktop as a Service (DaaS) segment is anticipated to

command a significant share in the global Workspace as a Service Market during

the forecast period.

Based on type, the market is divided into Desktop

as a Service (DaaS) and Application as a Service. The DaaS segment is the

dominant and fastest-growing category. Its prominence is due to its comprehensive

nature, delivering a full, managed virtual desktop infrastructure (VDI) from

the cloud. This eliminates the need for companies to manage the backend

infrastructure, offering a true turnkey solution that is highly scalable and

simplifies IT operations, making it particularly attractive for small and

medium-sized businesses.

The IT & Telecommunications segment dominated the market

in 2025 and is projected to grow at a significant CAGR during the forecast

period.

Based on application, the market is segmented

into IT & Telecommunications, BFSI, Healthcare, Manufacturing, Government,

Education, and Others. The IT & Telecommunications segment holds a

substantial share. This is a natural fit, as IT companies were early adopters

of remote work and possess the in-house skills to leverage cloud technologies

effectively. They use WaaS to provide secure, flexible development and testing

environments and to support a globally distributed workforce.

The IT & Telecommunications segment's

dominance is a direct reflection of the sector's inherent characteristics: a

digitally native workforce, a culture of technology adoption, and project-based

work that benefits from flexible resource allocation. For IT companies, WaaS is

not just a tool for remote work but a strategic asset that enables them to

rapidly scale up or down for projects, provide contractors with secure access

without provisioning physical hardware, and maintain stringent security protocols

for sensitive intellectual property and client data. The ability to deliver a

high-performance development environment from the cloud is a key factor driving

adoption within this segment.

The Large Enterprises segment is expected to hold the largest

market share in 2025.

By end-user, the market is divided into Large

Enterprises and Small & Medium Enterprises (SMEs). The Large Enterprises

segment is the largest end-user. This is attributed to their complex IT

environments, significant security and compliance requirements, and larger

budgets for digital transformation initiatives. Large enterprises are

leveraging WaaS to standardize desktop management across thousands of users and

to support a global, mobile workforce.

The following segments

are part of an in-depth analysis of the global Workspace As a Service Market:

|

Market Segments |

|

|

By Type |

●

Desktop as a Service

(DaaS) ●

Application as a

Service |

|

By Deployment |

●

Public Cloud ●

Private Cloud ●

Hybrid Cloud |

|

By Application |

●

IT &

Telecommunications ●

BFSI ●

Healthcare ●

Manufacturing ●

Others |

|

By End-user |

●

Large Enterprises ●

Small & Medium

Enterprises (SMEs) |

Workspace As a Service Market Share Analysis by Region

The North America region is anticipated to hold the largest

portion of the Workspace as a Service Market globally throughout the forecast

period.

North America is the leading segment, holding a

dominant share. This leadership is anchored by the early and widespread

adoption of cloud technologies, the presence of major WaaS vendors, and a

mature corporate sector that has aggressively embraced hybrid work. High

internet penetration, strong IT infrastructure, and a focus on cybersecurity

and operational efficiency collectively contribute to the region's market

supremacy.

The dominance of North America, particularly the

United States, in the WaaS market is underpinned by a robust ecosystem of

technology innovators and early-adopter enterprises. The region is home to the

world's largest cloud hyperscalers (AWS, Microsoft Azure, and

Google Cloud), whose infrastructure is the

foundation for most WaaS offerings. Furthermore, a competitive business

landscape and the need for agility force enterprises to adopt

productivity-enhancing technologies like WaaS rapidly. High awareness of

cybersecurity threats and stringent data protection regulations in industries

like finance and healthcare drive the adoption of the centralized security

model that WaaS provides, creating a strong, compliance-driven demand.

Workspace As a Service Market Competition Landscape Analysis

The global Workspace as a Service market is competitively

intense and features a diverse landscape of technology giants, specialized

virtualization vendors, and telecom service providers. Competition is based on

factors such as performance and user experience, security features, global

scale and reliability, pricing flexibility, and the strength of partner

ecosystems. Key strategies observed in the market include continuous innovation

in virtualization protocols to improve graphics performance and reduce latency,

strategic partnerships with cloud hyperscalers and hardware OEMs, and

acquisitions to consolidate market position and acquire new technologies. A

strong focus on developing value-added services around security, monitoring,

and management is also a key differentiator.

Global Workspace As a Service Market Recent Developments

News:

- In January 2025, Citrix Systems, a part of Cloud

Software Group, announced a new partnership with a major

telecommunications provider to offer a fully managed DaaS solution

tailored for the mid-market.

- In November 2024, VMware, by Broadcom, enhanced its VMware Horizon

Cloud platform with integrated Zero Trust security capabilities and

improved Microsoft Teams optimization for a superior user experience.

- In September 2024, Amazon Web Services (AWS)

launched a new tier of its Amazon WorkSpaces DaaS product, specifically

designed for graphics-intensive workloads in the media and entertainment

industry.

- In July 2024, Microsoft Corporation integrated new AI-powered

analytics into Windows 365 and Azure Virtual Desktop to provide IT

administrators with proactive insights into endpoint performance and user

connectivity issues.

The Global Workspace As a

Service Market is Dominated by a Few Large Companies, such as

●

Microsoft Corporation

●

Amazon Web Services,

Inc.

●

Citrix Systems (Cloud

Software Group)

●

VMware, Inc.

(Broadcom)

●

Google LLC

●

IBM Corporation

●

Cisco Systems, Inc.

●

Nutanix, Inc.

●

Oracle Corporation

●

Hewlett Packard

Enterprise Development LP

●

Cloud Software

Group

●

EVOXYB

●

Unisys Corporation

●

Datacom Group Ltd.

●

Rackspace Technology

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Workspace As a

Service Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Workspace as a Service Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Workspace As a

Service Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Workspace

As a Service Market

1.3.2.Deployment of Global

Workspace As A Service Market

1.3.3.Application of Global Workspace

As a Service Market

1.3.4.End-user of Global Workspace

As a Service Market

1.3.5.Region of Global Workspace

As a Service Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5. Pricing Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Workspace As a Service Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Workspace As a Service Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Workspace As a Service Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.Desktop as a Service

(DaaS)

4.1.2.Application as a Service

5. Global

Workspace As a Service Market Estimates

& Forecast Trend Analysis, by Deployment

5.1.

Global

Workspace As a Service Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

5.1.1.Public Cloud

5.1.2.Private Cloud

5.1.3.Hybrid Cloud

6. Global

Workspace As a Service Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Workspace As a Service Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.IT &

Telecommunications

6.1.2.BFSI

6.1.3.Healthcare

6.1.4.Manufacturing

6.1.5.Others

7. Global

Workspace As a Service Market Estimates

& Forecast Trend Analysis, by End-user

7.1.

Global

Workspace As a Service Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

7.1.1.Large Enterprises

7.1.2.Small & Medium

Enterprises (SMEs)

8. Global

Workspace As a Service Market Estimates

& Forecast Trend Analysis, by Region

8.1.

Global

Workspace As a Service Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Workspace

As a Service Market: Estimates &

Forecast Trend Analysis

9.1. North America Workspace As

a Service Market Assessments & Key Findings

9.1.1.North America Workspace As

a Service Market Introduction

9.1.2.North America Workspace As

a Service Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Application

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1. The U.S.

9.1.2.4.2. Canada

10. Europe Workspace

As a Service Market: Estimates &

Forecast Trend Analysis

10.1. Europe Workspace As a

Service Market Assessments & Key Findings

10.1.1. Europe Workspace As a

Service Market Introduction

10.1.2. Europe Workspace As a

Service Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Deployment

10.1.2.3.

By Application

10.1.2.4.

By End-user

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Workspace

As a Service Market: Estimates &

Forecast Trend Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Workspace As a Service Market Introduction

11.1.2.

Asia

Pacific Workspace As a Service Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Deployment

11.1.2.3.

By Application

11.1.2.4.

By End-user

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Workspace

As a Service Market: Estimates &

Forecast Trend Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Workspace As a Service Market Introduction

12.1.2. Middle

East & Africa

Workspace As a Service Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

12.1.2.1.

By Type

12.1.2.2.

By Deployment

12.1.2.3.

By Application

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Workspace As a Service Market:

Estimates & Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Workspace As

a Service Market Introduction

13.1.2. Latin America Workspace As

a Service Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Type

13.1.2.2.

By Deployment

13.1.2.3.

By Application

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Workspace As a

Service Market Product Mapping

15.2. Global Workspace As a

Service Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

15.3. Global Workspace As a

Service Market Tier Structure Analysis

15.4. Global Workspace As a

Service Market Concentration & Company Market Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

Microsoft Corporation

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2.

Amazon Web Services, Inc.

16.3.

Citrix Systems (Cloud Software Group)

16.4.

VMware, Inc. (Broadcom)

16.5.

Google LLC

16.6.

IBM Corporation

16.7.

Cisco Systems, Inc.

16.8.

Nutanix, Inc.

16.9.

Oracle Corporation

16.10.

Hewlett Packard Enterprise Development LP

16.11.

Cloud Software Group

16.12.

EVOXYB

16.13.

Unisys Corporation

16.14.

Datacom Group Ltd.

16.15.

Rackspace Technology

16.16.

Other Prominent Players

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables