Wound Closure Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Sutures, Hemostatic Agents, Staplers, Others), By Application (Orthopedics, Gynecology and Obstetrics, General Surgery, Ophthalmology, Cardiology, Others), By End-user (Hospitals & ASCs, Specialty Clinics, Others), and Geography

2026-01-02

Healthcare

Swetal (Research Analyst)

Description

Wound

Closure Market Overview

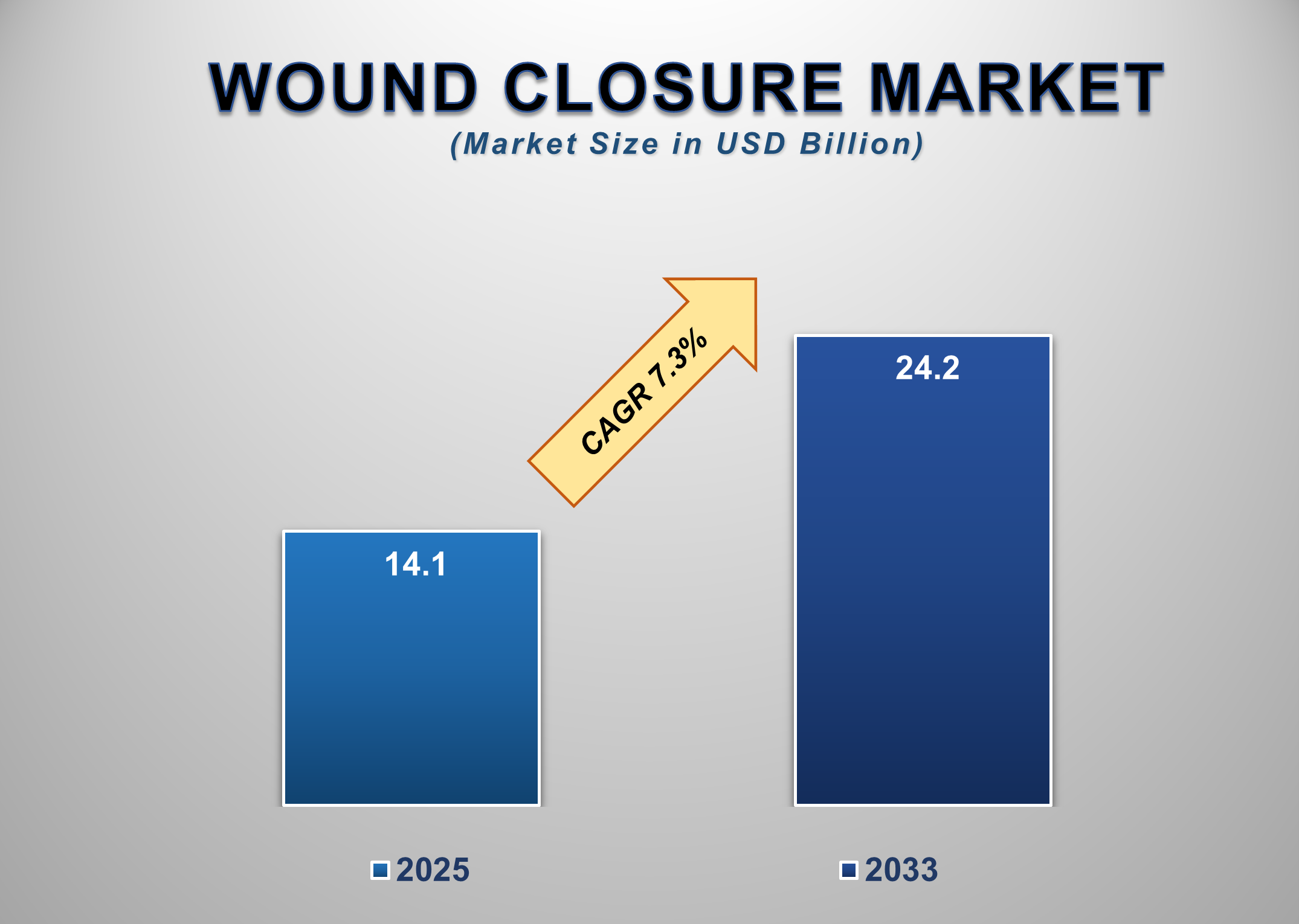

The global Wound Closure Market is poised for steady growth, reaching USD 24.2 billion by 2033, up from USD 14.1 billion in 2025, advancing at a CAGR of 7.3% during the forecast period. Market expansion is driven by the rising volume of surgical procedures, increasing traumatic injuries, and the growing prevalence of chronic wounds associated with diabetes, obesity, and vascular diseases. The rapid uptake of minimally invasive and robotic-assisted surgeries continues to elevate the demand for advanced wound closure solutions, including absorbable sutures, topical hemostatic agents, and innovative stapling devices.

Healthcare systems worldwide are prioritizing faster wound healing, reduced hospital stays, and improved surgical outcomes, contributing to higher adoption of reliable closure products across hospitals and ambulatory surgical centers. Technological advancements such as antibacterial-coated sutures, bioengineered sealants, and combination hemostats support improved infection control and better hemostatic performance, further boosting market penetration. Additionally, the rising aging population is leading to higher surgical needs, especially orthopedic and cardiovascular procedures, thereby sustaining long-term demand. However, product pricing and regulatory complexities continue to influence market dynamics.

Wound Closure Market Drivers and Opportunities

Rising Surgical Volume

and Trauma Cases are Driving the Growth of the Wound Closure Market

The increasing global surgical

burden remains a primary factor accelerating the growth of the wound closure

market. A significant rise in elective, trauma-related, and chronic

disease–associated surgeries has created sustained demand for sutures, staplers,

hemostatic agents, and combination wound closure products. Orthopedic,

bariatric, cardiovascular, and gynecological surgeries continue to expand,

driven by aging populations, higher obesity rates, and rising sports-related

injuries. Additionally, road accidents and trauma incidents, particularly in

Asia-Pacific and Latin America, are contributing substantially to the uptake of

wound closure materials across emergency care settings. As healthcare systems

strive to improve surgical outcomes and minimize postoperative complications,

there is heightened adoption of advanced closure solutions that reduce

scarring, promote faster recovery, and minimize infection risk. Innovations

such as absorbable sutures, antimicrobial coatings, plasma-derived sealants,

and minimally invasive stapling systems are increasingly being integrated into

surgical workflows. Hospitals and ambulatory surgical centers are also adopting

highly efficient hemostatic agents to manage blood loss and increase procedural

precision. The growing availability of skilled surgeons and improved access to

surgical care in emerging markets further supports expansion. Collectively,

rising surgical volume and trauma incidence significantly reinforce market

momentum and long-term growth prospects.

Increasing Adoption of

Advanced Hemostatic Agents and Minimally Invasive Stapling Technologies is

Fueling Market Expansion

The wound closure market is

witnessing strong traction from advanced hemostatic agents and next-generation

stapling devices, which are rapidly replacing traditional suturing techniques

in several procedures. Surgeons prefer modern hemostats such as active,

passive, and combination agents owing to their ability to achieve rapid

coagulation, reduce intraoperative bleeding, and improve procedural efficiency.

Combination hemostats, in particular, are gaining popularity for their enhanced

adhesive strength and extended applicability across cardiovascular, orthopedic,

and neurological surgeries. Minimally invasive surgical (MIS) procedures

continue to surge globally, increasing the demand for powered staplers and

precision-driven closure systems that enhance accuracy while reducing operative

time. Innovations such as battery-powered staplers, absorbable clips, and

robotic-compatible closure tools are driving adoption, especially across

hospitals and ASCs focused on improving workflow optimization. Additionally,

the integration of antimicrobial materials and bioresorbable technologies is

supporting improved postoperative outcomes. The rising need to reduce surgical

site infections (SSIs), improve wound healing, and shorten recovery time

further strengthens the market shift toward advanced wound closure products. As

hospitals increasingly prioritize efficiency, safety, and patient-centric

results, technologically enhanced closure systems are emerging as essential

tools, thereby supporting sustained market growth.

Growing Penetration of

Wound Closure Products in Emerging Markets is Expected to Create Significant

Opportunities Worldwide

Emerging regions are becoming key

growth hubs for the global wound closure market due to expanding healthcare

infrastructure, rising surgical procedures, and increased investment in

hospital capacity development. Countries across Asia-Pacific, the Middle East,

and Latin America are witnessing rapid advancements in trauma care systems and

specialized surgical departments, creating substantial demand for affordable

and effective wound closure products. The rising incidence of chronic diseases

such as diabetes and cardiovascular disorders is contributing to higher

surgical interventions, especially in low- and middle-income countries. Several

global manufacturers are strategically entering these markets with localized

manufacturing, cost-optimized product lines, and expanded distribution networks

to address affordability constraints. Government initiatives supporting

universal health coverage, improvements in emergency care services, and

increasing adoption of ambulatory surgical centers further open new opportunities

for product adoption. Additionally, growing awareness of infection control and

wound management practices is driving adoption of advanced closure solutions

such as coated sutures, bioresorbable sealants, and modern hemostatic agents.

As surgical care becomes more accessible and patient awareness increases,

emerging markets present a significant long-term opportunity for scalable,

innovative, and cost-effective wound closure solutions.

Wound Closure Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 14.1 Billion |

|

Market Forecast in 2033 |

USD 24.2 Billion |

|

CAGR % 2025-2033 |

7.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors

and more |

|

Segments Covered |

●

By Product Type ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Wound Closure Market

Report Segmentation Analysis

The global wound closure market

is segmented by product type, by application, by end-user, and by geography.

Sutures Segment Accounted

for the Largest Market Share in the Global Wound Closure Market

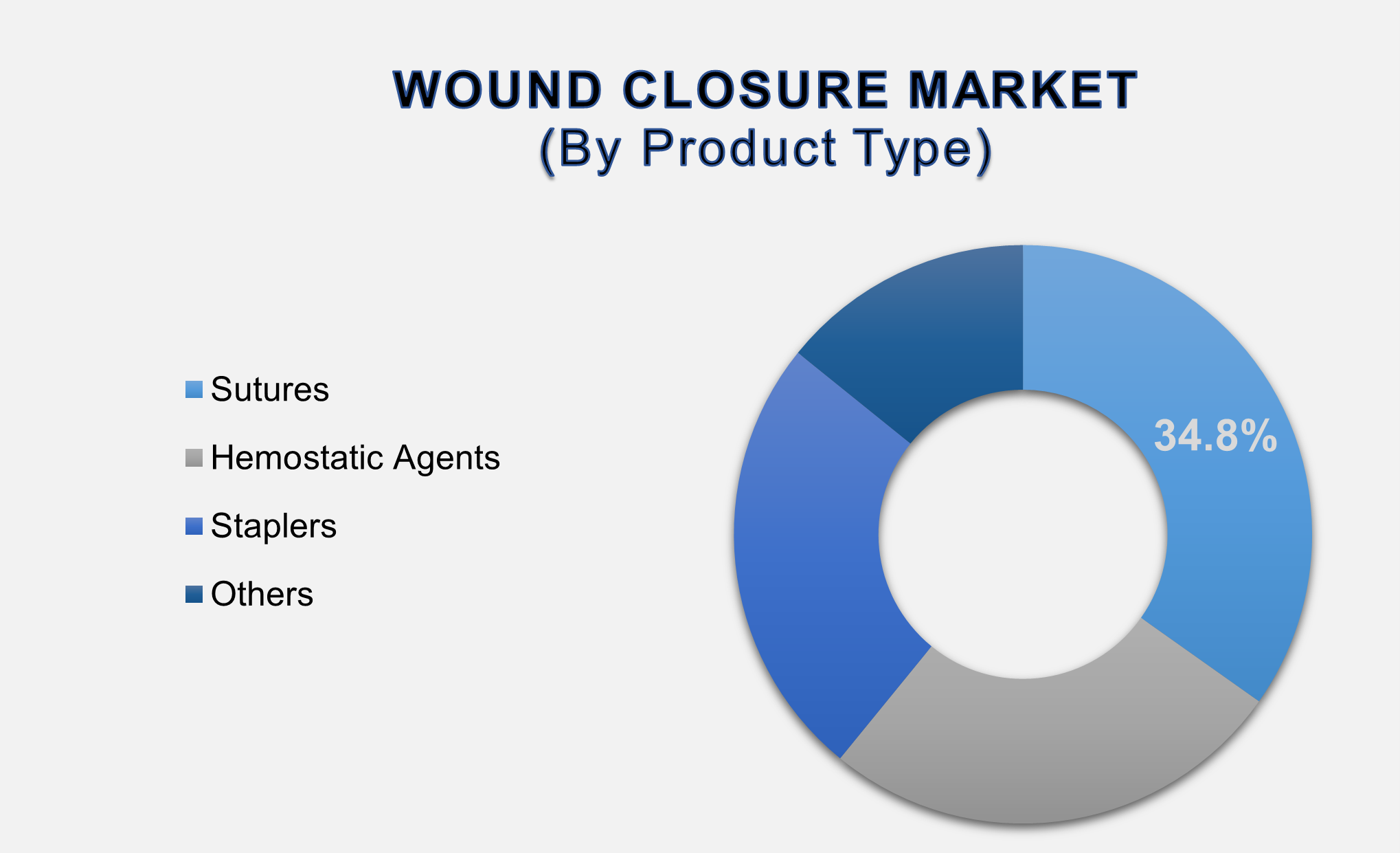

The Sutures segment held the largest market share in 2025, accounting for 34.8%, driven by their widespread usage across nearly all surgical disciplines and wound types. Sutures remain the most preferred closure solution due to their reliability, versatility, and cost-effectiveness, making them indispensable across general surgery, orthopedics, gynecology, cardiology, ophthalmology, and trauma care. Surgeons continue to rely on both absorbable and non-absorbable sutures depending on the anatomical site, tissue type, and procedural requirements. Innovations such as antimicrobial-coated sutures, barbed sutures, synthetic bioresorbable materials, and enhanced tensile-strength filaments are supporting improved wound healing and infection control. The high volume of routine surgical procedures, including cesarean sections, appendectomies, hernia repairs, and trauma suturing, contributes to consistent demand worldwide. Emerging economies with rising surgical infrastructure further strengthen segment growth. Despite increased adoption of staplers and sealants in specific procedures, sutures maintain dominance due to broad applicability, surgeon familiarity, and cost advantages, ensuring their continued leadership in the wound closure market.

Orthopedics Segment

Dominated the Global Wound Closure Market Owing to High Surgical Volume and

Increasing Trauma Cases

The

Orthopedics segment represents the largest application category in the wound

closure market, supported by a steady rise in joint replacement procedures,

fracture repairs, ligament reconstruction surgeries, and sports-related

interventions. The global aging population, rising road accidents, and growing

prevalence of osteoporosis contribute significantly to the expanding orthopedic

surgical burden. These procedures often involve deep tissue layers, requiring

multiple closure techniques such as sutures, staplers, and advanced hemostatic

agents to ensure stability and reduce postoperative complications. Increasing

adoption of minimally invasive orthopedic surgeries also drives demand for

specialized closure products designed to reduce scarring and accelerate

healing. Hospitals and orthopedic specialty centers are integrating modern

closure systems such as barbed sutures, absorbable clips, and biologically

active hemostats to improve patient recovery outcomes. With orthopedic

surgeries continuing to increase across North America, Europe, and

Asia-Pacific, this segment is expected to maintain strong growth momentum

throughout the forecast period.

Hospitals & ASCs

Segment Accounted for the Largest Share in the Wound Closure Market Owing to

High Surgical Capacity and Infrastructure Strength

The Hospitals & Ambulatory

Surgical Centers (ASCs) segment leads the wound closure market due to the

extensive volume of surgical procedures conducted in these facilities and their

ability to adopt advanced wound closure technologies. Hospitals and ASCs

possess the infrastructure required for complex procedures in orthopedics,

cardiology, neurology, gynecology, and general surgery, all of which require a

diverse range of closure methods. Increasing preference for outpatient

surgeries, supported by advancements in minimally invasive techniques,

continues to boost demand for efficient closure devices that minimize operative

time and enhance recovery. These healthcare settings also maintain high usage

of hemostatic agents, powered staplers, and bioresorbable sutures to reduce

infection risks and improve postoperative outcomes. Moreover, growing

investment in surgical suites, the rise of day-care procedures, and the

availability of skilled clinicians further support the segment. dominance. With

global healthcare systems expanding capacity, the hospitals & ASCs segment

is expected to remain the leading end-user category throughout the forecast

period.

The following segments are

part of an in-depth analysis of the global Wound Closure Market:

|

Market

Segments |

|

|

By Product

Type |

●

Sutures o

Absorbable o

Non-Absorbable ●

Hemostatic Agents o

Active Hemostats o

Passive Hemostats o

Combination

Hemostats o

Others ●

Staplers o

Powered o

Manual ●

Others |

|

By Application |

●

Orthopedics ●

Gynecology and

Obstetrics ●

General Surgery ●

Ophthalmology ●

Cardiology ●

Others |

|

By End-user |

●

Hospitals & ASCs ●

Specialty Clinics ●

Others |

Wound Closure Market Share Analysis by Region

The Asia Pacific region

is projected to hold the largest share of the global Wound Closure Market over

the forecast period.

Asia-Pacific dominated the global

wound closure market with a 39.9% share in 2025, driven by rapid expansion of

healthcare infrastructure, rising surgical volumes, and increasing trauma

incidence, particularly in China and India. The region continues to benefit

from improving access to surgical care, a growing middle-class population, and

government initiatives aimed at strengthening hospital capacity and emergency

response systems. Additionally, the rising prevalence of chronic diseases

contributes to higher procedural demand across general surgery, orthopedics,

and cardiovascular care.

North America, meanwhile, is

expected to register the fastest CAGR, supported by advanced surgical

technologies, increasing adoption of minimally invasive surgeries, and strong

reimbursement structures. Europe maintains a steady share driven by high-quality

healthcare systems and early adoption of innovative wound closure technologies.

Latin America and the Middle East & Africa are emerging growth regions due

to increasing investments in hospital expansion, medical tourism, and rising

awareness of infection control practices. Overall, regional growth is shaped by

infrastructure development, surgical accessibility, and evolving clinical

standards.

Wound Closure Market Competition Landscape

Analysis

The wound

closure market is moderately consolidated, with leading players such as Johnson

& Johnson, Medtronic, Baxter International, Abbott Laboratories, B. Braun

Melsungen, Smith & Nephew, 3M, Teleflex, and Stryker dominating global

distribution. These companies focus on expanding portfolios through the

development of antimicrobial sutures, powered stapling systems, bioresorbable

sealants, and advanced hemostatic agents.

Global Wound Closure Market Recent Developments

News:

- In March 2024, Intuitive

Surgical received U.S. FDA 510(k) clearance for the da Vinci 5, its

next-generation multiport robotic-assisted surgical system, enhancing

capabilities for minimally invasive procedures.

- In February 2024, Boston

Scientific Corporation announced that the UK's National Institute for

Health and Care Excellence (NICE) confirmed the safety and efficacy of

endoscopic sleeve gastroplasty (ESG) using its OverStitch™ endoscopic

suturing system, supporting its use as a minimally invasive weight-loss

procedure.

- In August 2023, Healthium

Medtech Limited launched TRUMAS, a range of synthetic absorbable sutures

in India, designed to improve performance and ease of use in minimally

invasive surgeries.

The Global Wound Closure Market is dominated by a

few large companies, such as

●

Johnson & Johnson

●

Medtronic

●

Baxter International

●

Abbott Laboratories

●

B. Braun Melsungen

●

Smith & Nephew

●

3M

●

Integra LifeSciences

●

Merit Medical Systems

●

Teleflex

●

Cardinal Health

●

Stryker

●

Derma Sciences

●

Molnlycke Health Care

●

Hartmann Group

●

Lohmann & Rauscher

●

Dynarex

●

Dukal

●

Covidien

●

Ethicon

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Wound Closure

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Wound Closure Market Scope and Market Estimation

1.2.1.Global Wound Closure

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Wound Closure

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Wound

Closure Market

1.3.2.Application of Global Wound

Closure Market

1.3.3.End-user of Global Wound

Closure Market

1.3.4.Region of Global Wound

Closure Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Wound Closure Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Wound Closure Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Wound Closure

Market Estimates & Forecast Trend

Analysis, by Product Type

4.1.

Global

Wound Closure Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type,

2020 - 2033

4.1.1.Sutures

4.1.1.1.

Absorbable

4.1.1.2.

Non-Absorbable

4.1.2.Hemostatic Agents

4.1.2.1.

Active

Hemostats

4.1.2.2.

Passive

Hemostats

4.1.2.3.

Combination

Hemostats

4.1.2.4.

Others

4.1.3.Staplers

4.1.3.1.

Powered

4.1.3.2.

Manual

4.1.4.Others

5.

Global Wound Closure

Market Estimates & Forecast Trend

Analysis, by Application

5.1.

Global

Wound Closure Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020

- 2033

5.1.1.Orthopedics

5.1.2.Gynecology and Obstetrics

5.1.3.General Surgery

5.1.4.Ophthalmology

5.1.5.Cardiology

5.1.6.Others

6.

Global Wound Closure

Market Estimates & Forecast Trend

Analysis, by End-user

6.1.

Global

Wound Closure Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020

- 2033

6.1.1.Hospitals & ASCs

6.1.2.Specialty Clinics

6.1.3.Others

7. Global

Wound Closure Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Wound Closure Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Wound

Closure Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Wound Closure Market Assessments & Key Findings

8.1.1.North America Wound

Closure Market Introduction

8.1.2.North America Wound

Closure Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Application

8.1.2.3. By End-user

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Wound

Closure Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Wound Closure Market Assessments & Key Findings

9.1.1.Europe Wound Closure

Market Introduction

9.1.2.Europe Wound Closure

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Application

9.1.2.3. By End-user

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Wound

Closure Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Wound Closure Market Introduction

10.1.2.

Asia

Pacific Wound Closure Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Application

10.1.2.3. By End-user

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Wound

Closure Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Wound Closure Market Introduction

11.1.2.

Middle East & Africa Wound Closure Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Application

11.1.2.3. By End-user

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Wound Closure Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Wound Closure Market Introduction

12.1.2.

Latin

America Wound Closure Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Application

12.1.2.3. By End-user

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Wound Closure Market Product Mapping

14.2.

Global

Wound Closure Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Wound Closure Market Tier Structure Analysis

14.4.

Global

Wound Closure Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1. Johnson

& Johnson

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Medtronic

15.3. Baxter

International

15.4. Abbott

Laboratories

15.5. B. Braun

Melsungen

15.6. Smith &

Nephew

15.7. 3M

15.8. Integra

LifeSciences

15.9. Merit Medical

Systems

15.10. Teleflex

15.11. Cardinal

Health

15.12. Stryker

15.13. Derma

Sciences

15.14. Molnlycke

Health Care

15.15. Hartmann

Group

15.16. Lohmann &

Rauscher

15.17. Dynarex

15.18. Dukal

15.19. Covidien

15.20. Ethicon

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables