Low Emission Vehicle Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Propulsion (Battery Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicles (PHEV), Fuel Cell Electric Vehicles (FCEV)); By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers); By Power Source (Less than 100 kW, 100-250 kW, More than 250 kW) and Geography

2025-11-13

Automotive & Transportation (Mobility)

Ekta Chaurasia (Team Lead)

Description

Low Emission Vehicle Market Overview

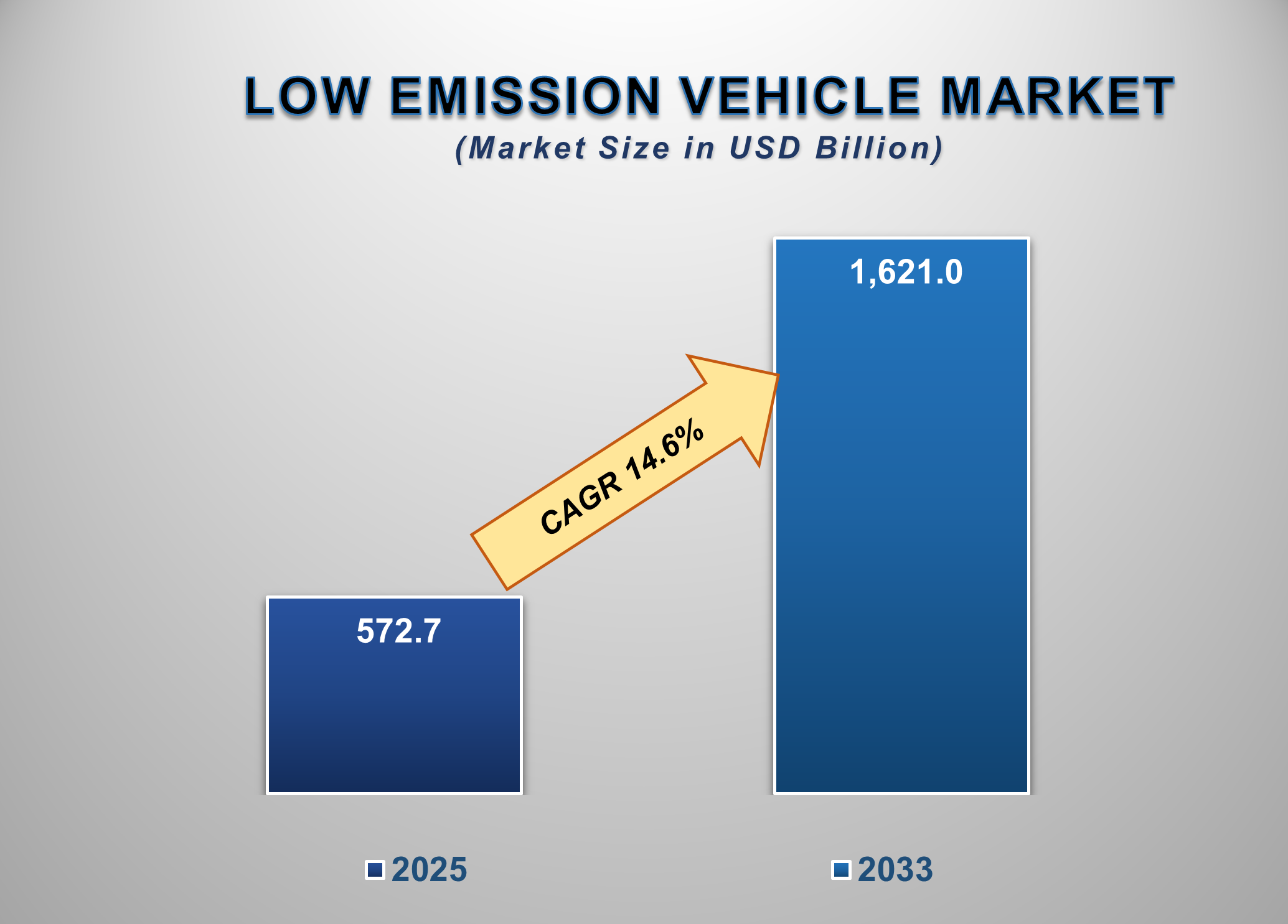

The low-emission vehicle market size is projected to witness exponential growth from 2025 to 2033, propelled by stringent global emission regulations, rising consumer environmental awareness, declining battery costs, and substantial government incentives and investments in charging infrastructure. Valued at approximately USD 572.7 Billion in 2025, the market is expected to surge to USD 1,621.0 Billion by 2033, reflecting a robust compound annual growth rate (CAGR) of 14.6% over the forecast period.

The low-emission vehicle market

is at the forefront of a fundamental transformation in the global automotive

industry, driven by the urgent need to decarbonize transport and achieve

climate goals. This paradigm shift is moving low- and zero-emission vehicles

from a niche segment to the mainstream of automotive production and consumer

choice. Technological advancements, particularly in battery energy density and

charging speed, are continuously improving vehicle range and performance,

thereby alleviating consumer range anxiety. The market's growth is further

accelerated by the entry of a diverse range of models from both traditional

OEMs and new entrants, covering various segments from economy to luxury. Key

growth areas include long-range BEVs, affordable urban EVs, and the emerging

FCEV segment for heavy-duty transport. The market is also benefiting from

corporate sustainability commitments and the growing total cost of ownership

advantage of electric vehicles over their internal combustion engine counterparts.

Low Emission Vehicle

Market Drivers and Opportunities

Stringent

Government Regulations and Policy Support

Globally, governments are implementing

increasingly strict emission standards and fuel economy mandates, compelling

automakers to electrify their fleets. Policies such as the European Union's

"Fit for 55" package, China's dual-credit policy, and the U.S.

Inflation Reduction Act are creating a powerful regulatory push. These are

often coupled with direct consumer incentives like tax credits, purchase

subsidies, and non-financial benefits such as access to bus lanes or exemption

from congestion charges. This regulatory framework is the single most

significant driver, de-risking investments for automakers and making LEVs more

financially accessible to consumers.

Rising Consumer

Environmental Awareness and Falling Battery Costs

A profound shift in consumer consciousness

towards environmental sustainability is creating a strong demand pull for

cleaner transportation options. Consumers are increasingly factoring in carbon

footprints and air quality impacts into their purchasing decisions.

Concurrently, the continuous decline in lithium-ion battery costs, which

constitute a significant portion of an EV's price, is making low-emission

vehicles more price-competitive with conventional vehicles. This economic

viability, combined with lower operating and maintenance costs, is accelerating

consumer adoption across both personal and commercial vehicle segments.

Opportunity

for the Low Emission Vehicle Market

Expansion into

the Commercial Vehicle Segment and Emerging Economies

A significant opportunity lies in the

electrification of the commercial vehicle segment, including logistics vans,

buses, and trucks. As cities implement low-emission zones and companies seek to

green their supply chains, the demand for electric commercial vehicles is set

to explode. Furthermore, a massive opportunity exists in the untapped potential

of emerging economies in the

Asia-Pacific, Latin America, and Africa. While

adoption is currently led by China, Europe, and North America, rising

urbanization, air quality concerns, and supportive local policies in countries

like India, Brazil, and Thailand are expected to be the next major growth

frontiers. Companies that can develop affordable, locally-suited LEVs and

associated infrastructure are poised to capture a substantial market share.

Low Emission Vehicle

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 572.7 Billion |

|

Market Forecast in 2033 |

USD 1,621.0 Billion |

|

CAGR % 2025-2033 |

14.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, Company Share, Company Heatmap, Company

Production, Growth Factors and more |

|

Segments Covered |

●

By Propulsion ●

By Power Source ●

By Vehicle Type |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Low Emission Vehicle

Market Report Segmentation Analysis

The global Low Emission Vehicle

Market industry analysis is segmented by Propulsion, by Vehicle Type, and by

Power Source.

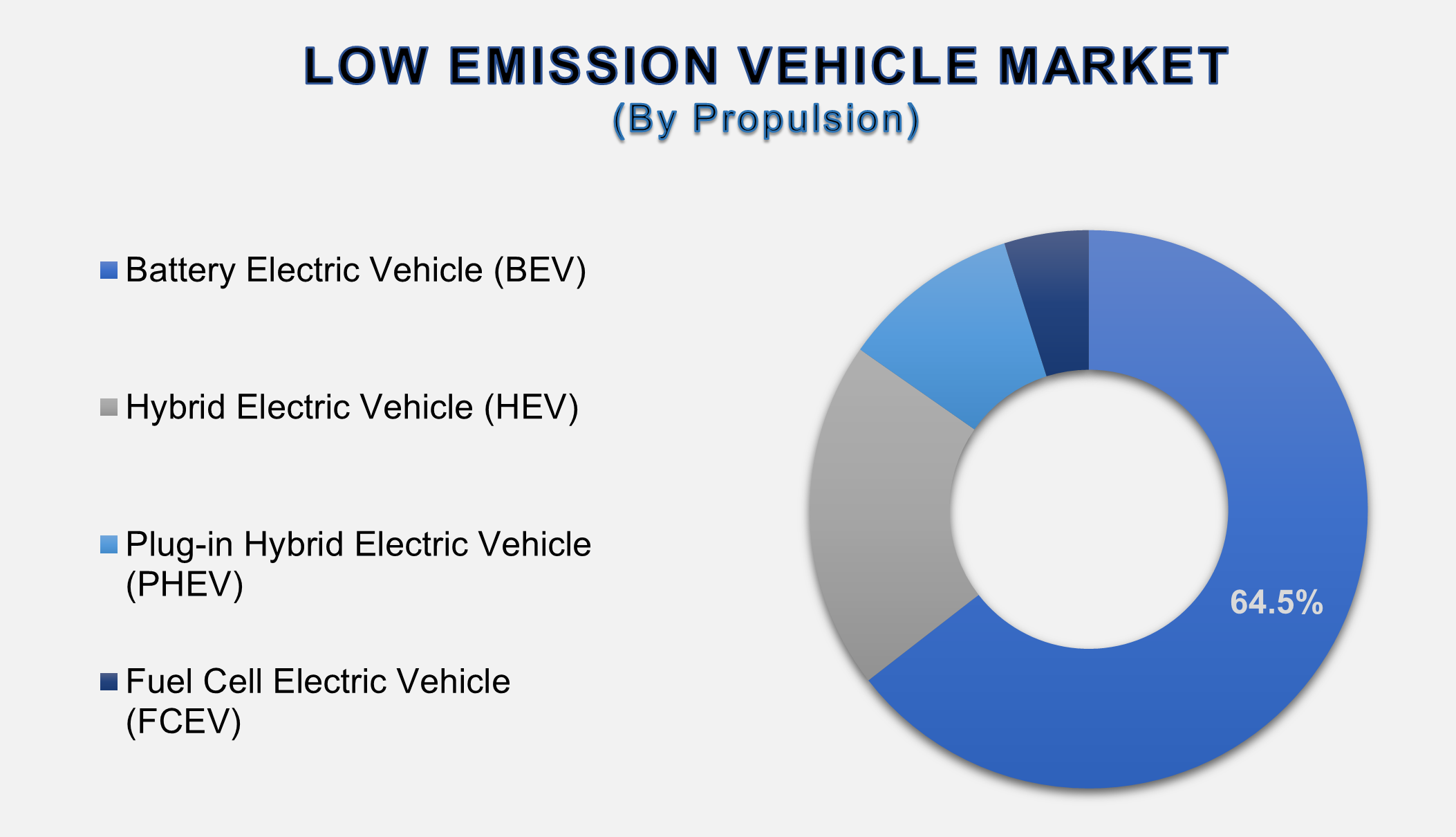

The Dominance of

the Battery Electric Vehicle (BEV) Propulsion Segment

The BEV segment is the fastest-growing and

increasingly dominant segment in the low-emission vehicle market. This

leadership is driven by the global push for full decarbonization, as BEVs

produce zero tailpipe emissions. Major automotive OEMs are channeling the bulk of their R&D and capital expenditure into BEV

platforms, leading to a rapid expansion of available models. Continuous

improvements in charging infrastructure, coupled with significant advancements

in battery technology that extend range and reduce cost, are making BEVs a

viable primary vehicle for a growing number of consumers. With governments

planning to phase out internal combustion engine vehicles, the BEV segment is

poised to capture the largest market share over the forecast period.

The Passenger

Cars application segment commands a major share of the market

The Passenger Cars segment commands the dominant

market share, as it represents the largest volume segment of the global

automotive industry. The transition to low-emission vehicles is currently most visible and advanced in this

category, driven by consumer demand, a wide array of model choices, and strong

government purchase incentives. The high rate of personal vehicle ownership

globally, combined with the daily use case of passenger cars, makes their

electrification critical to achieving transportation emission targets. The

segment benefits from intense competition, which is driving down prices and

accelerating innovation in features, design, and performance.

The Leadership of

the 100-250 kW Power Source Segment

The 100-250 kW power output segment represents

the sweet spot for the majority of the market, balancing performance, cost, and

range. This segment covers a wide range of mainstream passenger cars and SUVs

that offer sufficient power for highway driving and acceleration, along with a

range that meets the daily needs of most consumers. As battery technology

improves, the cost of producing powertrains in this power band is decreasing,

making it the most competitive and high-volume segment. It appeals to the broadest

consumer base, securing its leadership position among power source segments.

The following segments are part of an in-depth analysis of the global

Low Emission Vehicle Market:

|

Market Segments |

|

|

By Propulsion |

●

Battery Electric

Vehicle (BEV) ●

Hybrid Electric

Vehicle (HEV) ●

Plug-in Hybrid

Electric Vehicle (PHEV) ●

Fuel Cell Electric

Vehicle (FCEV) |

|

By Vehicle Type |

●

Passenger Cars ●

Commercial Vehicles ●

Two-Wheelers |

|

By Power Source

|

●

Less than 100 kW ●

100-250 kW ●

More than 250 kW |

Low Emission Vehicle

Market Share Analysis by Region

The Asia-Pacific region is expected to dominate the Global

Low Emission Vehicle Market during the forecast period.

Asia-Pacific is the undisputed leader in

the global Low Emission Vehicle Market, both in terms of production and sales.

This dominance is anchored by China, which is the world's largest market for

EVs, supported by aggressive government policies, a robust domestic supply

chain for batteries and components, and the presence of leading manufacturers

like BYD and SAIC. Other key contributors include Japan, with its strong HEV

and BEV legacy, and South Korea, home to leaders like Hyundai and Kia. The

region's massive population, rapid urbanization, severe air quality issues in

major cities, and strong government backing create an unparalleled ecosystem

for LEV growth, ensuring its leading position.

Global Low Emission

Vehicle Market Recent Developments News:

- In

February 2025, Tesla announced a breakthrough in its 4680 battery cell

production, significantly reducing costs and paving the way for a new

generation of more affordable EVs.

- In

March 2025, A consortium of European automakers (VW, Stellantis, Renault)

finalized a joint venture to build a network of ultra-fast charging

stations across major European highways.

- In

April 2025, BYD launched its "Seagull" model in emerging markets

across Southeast Asia and Latin America, targeting the ultra-affordable

small EV segment.

The Global Low Emission Vehicle Market is dominated by a few

large companies, such as

●

Tesla, Inc.

●

BYD Company Ltd.

●

Volkswagen AG

●

Stellantis N.V.

●

Hyundai Motor Group

●

General Motors Company

●

Ford Motor Company

●

Toyota Motor

Corporation

●

Rivian Automotive,

Inc.

●

Lucid Motors, Inc.

●

NIO Inc.

●

XPeng Inc.

●

Li Auto Inc.

●

Nissan Motor Co., Ltd.

●

BMW AG

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Low Emission

Vehicle Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Low Emission Vehicle Market Scope and Market Estimation

1.2.1.Global Low Emission

Vehicle Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Low Emission

Vehicle Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Propulsion of Global Low

Emission Vehicle Market

1.3.2.Power Source of Global Low

Emission Vehicle Market

1.3.3.Vehicle Type of Global Low

Emission Vehicle Market

1.3.4.Region of Global Low

Emission Vehicle Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Low Emission Vehicle Market

2.8.

Key

Products/Brand Analysis

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

2.11.

Key

Regulation

3. Global

Low Emission Vehicle Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Low Emission

Vehicle Market Estimates

& Forecast Trend Analysis, by Propulsion

4.1.

Global

Low Emission Vehicle Market Revenue (US$ Bn) Estimates and Forecasts, by Propulsion,

2020 - 2033

4.1.1.Battery Electric Vehicle

(BEV)

4.1.2.Hybrid Electric Vehicle

(HEV)

4.1.3.Plug-in Hybrid Electric

Vehicle (PHEV)

4.1.4.Fuel Cell Electric Vehicle

(FCEV)

5.

Global Low Emission

Vehicle Market Estimates

& Forecast Trend Analysis, by Power Source

5.1.

Global

Low Emission Vehicle Market Revenue (US$ Bn) Estimates and Forecasts, by Power

Source, 2020 - 2033

5.1.1.Less than 100 kW

5.1.2.100-250 kW

5.1.3.More than 250 kW

6.

Global Low Emission

Vehicle Market Estimates

& Forecast Trend Analysis, by Vehicle Type

6.1.

Global

Low Emission Vehicle Market Revenue (US$ Bn) Estimates and Forecasts, by Vehicle

Type, 2020 - 2033

6.1.1.Passenger Cars

6.1.2.Commercial Vehicles

6.1.3.Two-Wheelers

7. Global

Low Emission Vehicle Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Low Emission Vehicle Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Low

Emission Vehicle Market: Estimates

& Forecast Trend Analysis

8.1. North America Low Emission

Vehicle Market Assessments & Key Findings

8.1.1.North America Low Emission

Vehicle Market Introduction

8.1.2.North America Low Emission

Vehicle Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Propulsion

8.1.2.2. By Power

Source

8.1.2.3. By Vehicle

Type

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Low

Emission Vehicle Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Low Emission Vehicle Market Assessments & Key Findings

9.1.1.Europe Low Emission

Vehicle Market Introduction

9.1.2.Europe Low Emission

Vehicle Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Propulsion

9.1.2.2. By Power

Source

9.1.2.3. By Vehicle

Type

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Netherlands

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Low

Emission Vehicle Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Low Emission Vehicle Market Introduction

10.1.2.

Asia

Pacific Low Emission Vehicle Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Propulsion

10.1.2.2. By Power

Source

10.1.2.3. By Vehicle

Type

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Low

Emission Vehicle Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Low Emission Vehicle Market

Introduction

11.1.2.

Middle East & Africa Low Emission Vehicle Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Propulsion

11.1.2.2. By Power

Source

11.1.2.3. By Vehicle

Type

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4.

Rest of MEA

12. Latin America

Low Emission Vehicle Market: Estimates

& Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Low Emission Vehicle Market Introduction

12.1.2.

Latin

America Low Emission Vehicle Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Propulsion

12.1.2.2. By Power

Source

12.1.2.3. By Vehicle

Type

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Low Emission Vehicle Market Product Mapping

14.2.

Global

Low Emission Vehicle Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Low Emission Vehicle Market Tier Structure Analysis

14.4.

Global

Low Emission Vehicle Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1. Tesla, Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. BYD Company

Ltd.

15.3. Volkswagen AG

15.4. Stellantis

N.V.

15.5. Hyundai Motor

Group

15.6. General

Motors Company

15.7. Ford Motor

Company

15.8. Toyota Motor

Corporation

15.9. Rivian

Automotive, Inc.

15.10. Lucid Motors,

Inc.

15.11. NIO Inc.

15.12. XPeng Inc.

15.13. Li Auto Inc.

15.14. Nissan Motor

Co., Ltd.

15.15. BMW AG

15.16. Other

Prominent Players

16. Research

Methodology

16.1.

External

Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables