Salad Dressings and Mayonnaise Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type (Salad Dressings, Mayonnaise); By Ingredient Source (Conventional, Organic & Natural, Plant-Based / Vegan); By Packaging Type (Jars, Sachets & Pouches, Bottles, Tubes & Containers); By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail/E-commerce, Specialty & Gourmet Stores, Food Service / HoReCa); and Geography

2025-11-26

Consumer Products

Jaya Bundele (Research Analyst)

Description

Salad Dressings & Mayonnaise Market Overview

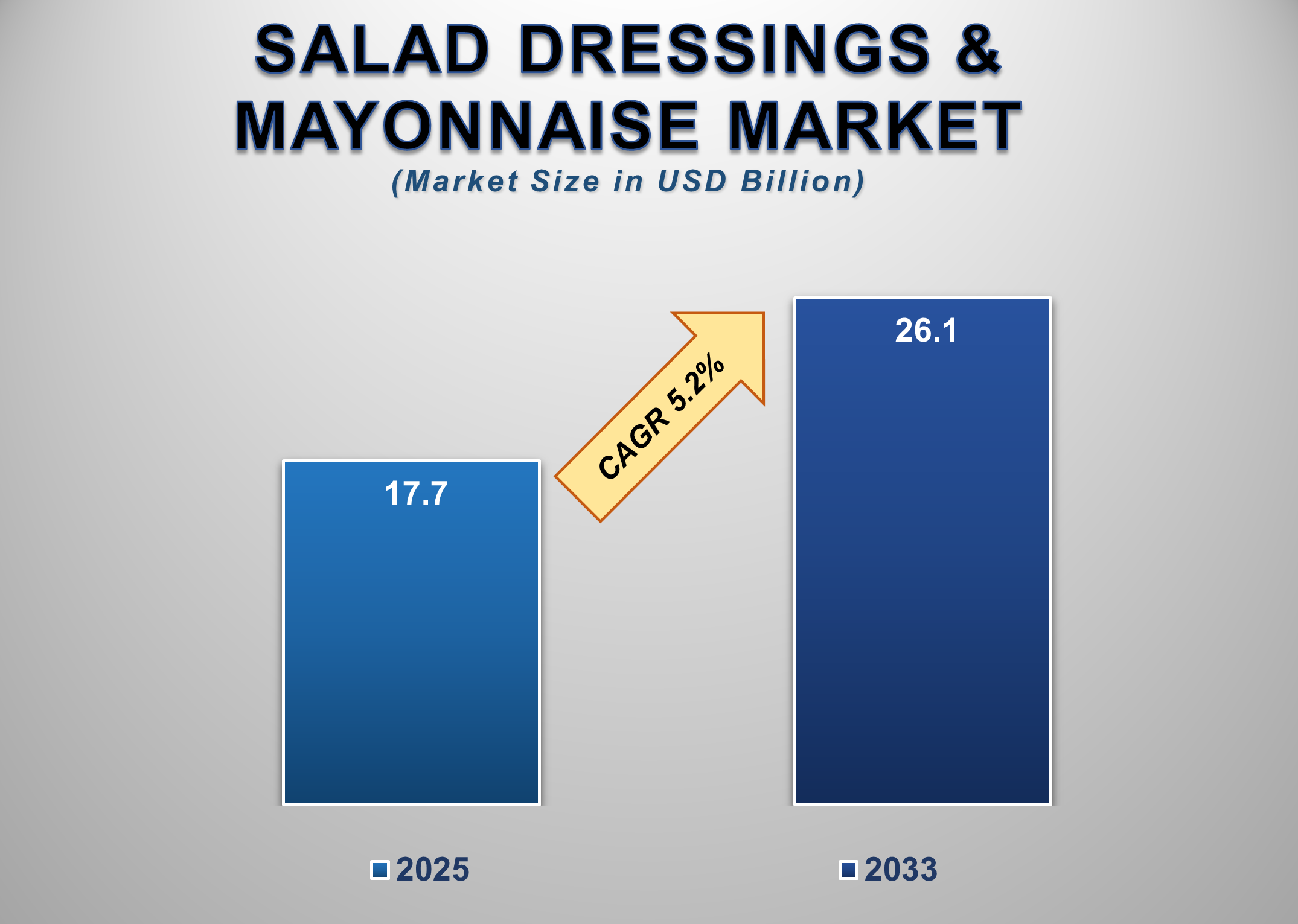

The Global Salad Dressings & Mayonnaise Market is experiencing robust expansion driven by evolving consumer dietary habits, rising health consciousness, and the growing global trend of convenient and ready-to-eat food products. The market was valued at USD 17.7 billion in 2025 and is projected to reach USD 26.1 billion by 2033, expanding at a CAGR of 5.2% during the forecast period.

Salad dressings and mayonnaise

are integral components of modern culinary practices, widely used across

households, restaurants, and the food service industry. The rising adoption of

Western-style diets, increasing global urbanization, and a growing preference

for flavorful, nutritious, and convenient meal options are major factors

boosting market growth. Moreover, the expansion of international fast-food

chains and the availability of diverse dressing varieties ranging from low-fat

to vegan and organic formulations have further contributed to widespread market

acceptance.

Salad Dressings &

Mayonnaise Market Drivers and Opportunities

Rising health awareness and demand for nutritious,

clean-label products are driving market growth

The global shift toward healthier lifestyles and balanced

nutrition is a primary growth driver for the salad dressings and mayonnaise

market. Consumers are increasingly conscious about the nutritional value of the

foods they consume, resulting in heightened demand for products with reduced

fat, sugar, and artificial additives. This has prompted manufacturers to

reformulate traditional dressings and mayonnaise with functional ingredients

such as olive oil, avocado oil, and yogurt bases that offer better nutritional

profiles.

The clean-label movement, emphasizing transparency, natural

ingredients, and minimal processing, has further reshaped consumer preferences.

Health-conscious buyers are actively seeking gluten-free, non-GMO, and organic

variants, while also favoring plant-based alternatives. In response, global

brands are expanding product lines to include vegan and eggless mayonnaise

options catering to ethical and dietary concerns.

Additionally, the increasing adoption of salads as a main course

meal in urban diets has significantly boosted dressing consumption. The

influence of social media-driven food trends and culinary innovation is also

enhancing consumer experimentation with new flavors, leading to strong demand

growth across both premium and mid-range product segments.

Expansion of food service and retail channels is fueling

market penetration

The rapid expansion of the global food service sector, including

quick-service restaurants (QSRs), cafés, and gourmet dining establishments, is

a major factor propelling the salad dressings and mayonnaise market. As the

global restaurant industry continues to rebound post-pandemic, sauces and

condiments have become indispensable ingredients for menu diversification and

flavor enhancement. Manufacturers are forming long-term supply partnerships

with food chains and catering services to ensure consistent demand and brand

visibility. Simultaneously, the proliferation of organized retail and

e-commerce has expanded consumer access to a diverse array of dressings and

mayonnaise products. Online grocery platforms and direct-to-consumer channels

have allowed brands to reach broader audiences with greater convenience and

personalized offerings. Furthermore, the integration of smart packaging,

improved shelf life, and portion-controlled formats is supporting product

innovation across various retail platforms.

Emerging markets in Asia-Pacific and Latin America are witnessing

rapid growth in both modern trade and HoReCa channels, presenting lucrative

opportunities for established players to expand geographically and diversify

their distribution networks.

The rising popularity of plant-based and vegan formulations

presents lucrative opportunities

The global rise in veganism and flexitarian diets is creating

substantial opportunities for innovation within the salad dressings and

mayonnaise market. With growing consumer demand for sustainable, ethical, and

plant-based alternatives, food manufacturers are investing heavily in eggless,

dairy-free, and allergen-friendly product development. Plant-derived

ingredients such as chickpea protein, aquafaba, and soy have become

increasingly popular as emulsifying bases in vegan mayonnaise and creamy salad

dressings.

Additionally, the rising environmental awareness among consumers

is pushing brands to adopt eco-friendly sourcing and sustainable packaging

solutions. Startups and premium brands are capitalizing on this trend by

introducing artisanal, organic, and superfood-infused dressings that align with

modern health and ethical preferences.

As regulatory support and consumer acceptance of vegan foods

continue to strengthen globally, the plant-based product segment is anticipated

to experience double-digit growth in the coming years. Companies that innovate

with natural flavorings, functional ingredients, and environmentally

responsible packaging are well-positioned to capitalize on this evolving

consumer landscape.

Salad Dressings &

Mayonnaise Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 17.7 Billion |

|

Market Forecast in 2033 |

USD 26.1 Billion |

|

CAGR % 2025-2033 |

5.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type ●

By Ingredient

Source ●

By Packaging Type ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Salad Dressings &

Mayonnaise Market Report Segmentation Analysis

The global Salad Dressings & Mayonnaise Market is segmented by

Type, by Ingredient Source, by Packaging Type, by Distribution Channel, and by

Region.

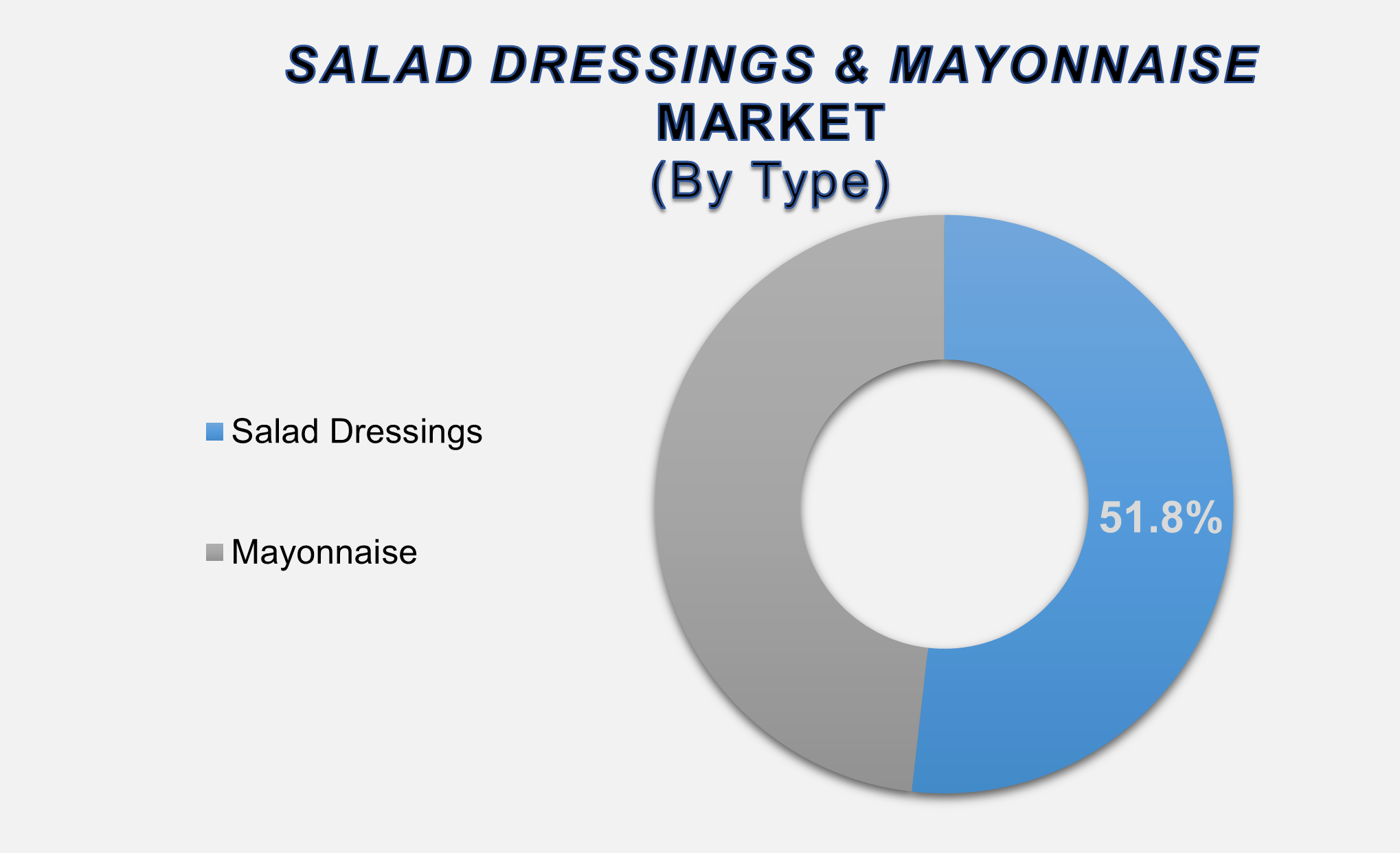

The

Salad Dressings segment accounted for the largest

market share in the global Salad Dressings & Mayonnaise market

By

Type, the market is divided into Salad Dressings and Mayonnaise. The Salad

Dressings segment dominated the market in 2025 with a share of 51.8%, driven by

increasing global consumption of salads as a staple meal option among

health-conscious consumers. The rising popularity of international cuisines,

including Mediterranean and continental dishes, has expanded the use of diverse

dressing varieties such as vinaigrettes, creamy blends, and yogurt-based

sauces. The introduction of premium, low-calorie, and functional dressings

infused with herbs, superfoods, and probiotics has further diversified product

offerings. Brands are focusing on reformulations that balance flavor with

nutritional benefits, appealing to wellness-oriented demographics. The growing

presence of salad bars, online recipe platforms, and meal kit services also

contributes to the strong growth of this segment globally.

The Conventional ingredient source segment holds the largest market share

in the Salad Dressings & Mayonnaise market

By Ingredient Source, the market is segmented into Conventional,

Organic & Natural, and Plant-Based / Vegan. The Conventional segment

currently leads the market, supported by its affordability, accessibility, and

widespread consumer familiarity. Despite the growing shift toward organic and

vegan options, conventional salad dressings and mayonnaise continue to account

for a significant share in both household and food service applications.

However, manufacturers are increasingly enhancing conventional formulations

with cleaner ingredient profiles and minimal additives to align with modern

health trends. While the conventional segment dominates in volume, the organic

and vegan categories are expected to register higher CAGR growth, driven by

increasing health awareness and ethical consumption preferences.

The Jars packaging type segment leads the global Salad Dressings

& Mayonnaise market

By

Packaging Type, the market is categorized into Jars, Sachets & Pouches,

Bottles, and Tubes & Containers. The Jars segment accounted for the largest

market share in 2025, owing to their durability, premium appeal, and

suitability for both retail and food service usage. Glass and PET jars provide

excellent product visibility and shelf presentation, making them preferred

formats for high-end brands and home consumption. Meanwhile, sachets and

pouches are gaining traction in emerging markets and food delivery services due

to their portability and single-use convenience. Manufacturers are also

adopting recyclable and biodegradable materials to enhance sustainability

across packaging lines, reflecting growing environmental awareness among

consumers and retailers alike.

The following segments are

part of an in-depth analysis of the global Salad Dressings & Mayonnaise

market:

|

Market Segments |

|

|

By Type |

●

Salad Dressings ●

Mayonnaise |

|

By Ingredient

Source |

●

Conventional ●

Organic &

Natural ●

Plant-Based / Vegan |

|

By Packaging

Type |

●

Jars ●

Sachets &

Pouches ●

Bottles ●

Tubes &

Containers |

|

By

Distribution Channel |

●

Supermarkets &

Hypermarkets ●

Convenience Stores ●

Online Retail /

E-commerce ●

Specialty &

Gourmet Stores ●

Food Service /

HoReCa |

Salad Dressings &

Mayonnaise Market Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Salad Dressings & Mayonnaise

Market globally throughout the forecast period.

North America accounted for the

largest market share of 51.3% in 2025, driven by high consumer preference for

convenience foods, strong retail penetration, and the well-established presence

of leading global brands such as Kraft Heinz, Unilever, and McCormick. The

region’s mature food service industry and rising demand for customized and

gourmet condiments further reinforce its dominance. Consumer inclination toward

low-fat, organic, and vegan products is also reshaping product innovation in

the region. The U.S., in particular, is witnessing increased adoption of

clean-label and functional salad dressings with natural ingredients.

Conversely, the Asia-Pacific

region is anticipated to record the fastest CAGR during the forecast period.

The growth is supported by rapid urbanization, expanding middle-class

populations, and increasing Western food influence. Countries such as China, India,

and Japan are seeing strong growth in both retail and HoReCa consumption. Local

brands, coupled with global entrants, are leveraging e-commerce and modern

trade channels to cater to evolving regional tastes and preferences.

Salad Dressings &

Mayonnaise Market Competition Landscape Analysis

The global salad dressings and

mayonnaise market is moderately consolidated, with leading multinational

players dominating key markets alongside regional and artisanal producers.

Competition centers around flavor innovation, health-oriented product launches,

sustainable packaging, and omnichannel distribution strategies.

Global Salad Dressings

& Mayonnaise Market Recent Developments News:

- In September 2025,

Dole introduced its Apple Harvest Premium Salad Kit, a seasonal fall

offering featuring a spring mix base, aged cheddar cheese, brown sugar

pecans, and apple cider vinaigrette. Designed to meet consumer interest in

restaurant-quality salads at home, the launch was supported by refreshed

packaging across Dole’s core product portfolio.

- In April 2025,

Hidden Valley launched seven new ranch flavor varieties and a redesigned

"Easy Squeeze" bottle with an improved applicator for better

control. The expansion addressed growing demand for flavor customization

and included both widely available and retailer-exclusive options to boost

in-store traffic.

The Global Salad Dressings & Mayonnaise Market Is Dominated by a Few Large Companies, such as

●

Kraft Heinz Company

●

Nestlé

●

McCormick &

Company

●

The J.M. Smucker

Company

●

Unilever

●

Kewpie Corporation

●

Nando’s

●

Veeba Professional

●

Ken’s Foods

●

Naturally Fresh

●

Sir Kensington’s

●

Primal Kitchen

●

Tessemae’s

●

Bolthouse Farms

●

Brianna's Fine Salad

Dressings

●

Litehouse Inc.

●

Marzetti Company

●

Walden Farms

●

Newman’s Own

●

Stonewall Kitchen

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Salad Dressings

& Mayonnaise Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Salad Dressings & Mayonnaise Market Scope and Market Estimation

1.2.1.Global Salad Dressings

& Mayonnaise Overall Market Size (US$ Bn), Market CAGR (%), Market forecast

(2025 - 2033)

1.2.2.Global Salad Dressings

& Mayonnaise Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Salad

Dressings & Mayonnaise Market

1.3.2.Ingredient Source of

Global Salad Dressings & Mayonnaise Market

1.3.3.Packaging Type of Global Salad

Dressings & Mayonnaise Market

1.3.4.Distribution Channel of

Global Salad Dressings & Mayonnaise Market

1.3.5.Region of Global Salad

Dressings & Mayonnaise Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Salad Dressings & Mayonnaise Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Salad Dressings & Mayonnaise Market

Estimates & Forecast Trend Analysis, by Type

4.1.

Global

Salad Dressings & Mayonnaise Market Revenue (US$ Bn) Estimates and

Forecasts, by Type, 2020 - 2033

4.1.1.Salad Dressings

4.1.2.Mayonnaise

5. Global

Salad Dressings & Mayonnaise Market

Estimates & Forecast Trend Analysis, by Ingredient

Source

5.1.

Global

Salad Dressings & Mayonnaise Market Revenue (US$ Bn) Estimates and

Forecasts, by Ingredient Source, 2020 - 2033

5.1.1.Conventional

5.1.2.Organic & Natural

5.1.3.Plant-Based / Vegan

6. Global

Salad Dressings & Mayonnaise Market

Estimates & Forecast Trend Analysis, by Packaging

Type

6.1.

Global

Salad Dressings & Mayonnaise Market Revenue (US$ Bn) Estimates and

Forecasts, by Packaging Type, 2020 - 2033

6.1.1.Jars

6.1.2.Sachets & Pouches

6.1.3.Bottles

6.1.4.Tubes & Containers

7. Global

Salad Dressings & Mayonnaise Market

Estimates & Forecast Trend Analysis, by Distribution

Channel

7.1.

Global

Salad Dressings & Mayonnaise Market Revenue (US$ Bn) Estimates and

Forecasts, by Distribution Channel, 2020 - 2033

7.1.1.Supermarkets &

Hypermarkets

7.1.2.Convenience Stores

7.1.3.Online Retail / E-commerce

7.1.4.Specialty & Gourmet

Stores

7.1.5.Food Service / HoReCa

8. Global

Salad Dressings & Mayonnaise Market

Estimates & Forecast Trend Analysis, by Region

8.1.

Global

Salad Dressings & Mayonnaise Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Salad

Dressings & Mayonnaise Market:

Estimates & Forecast Trend Analysis

9.1. North America Salad

Dressings & Mayonnaise Market Assessments & Key Findings

9.1.1.North America Salad

Dressings & Mayonnaise Market Introduction

9.1.2.North America Salad

Dressings & Mayonnaise Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

9.1.2.1.

By Type

9.1.2.2.

By Ingredient Source

9.1.2.3.

By Packaging Type

9.1.2.4.

By Distribution Channel

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Salad

Dressings & Mayonnaise Market:

Estimates & Forecast Trend Analysis

10.1. Europe Salad Dressings

& Mayonnaise Market Assessments & Key Findings

10.1.1. Europe Salad Dressings

& Mayonnaise Market Introduction

10.1.2. Europe Salad Dressings

& Mayonnaise Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Ingredient Source

10.1.2.3.

By Packaging Type

10.1.2.4.

By Distribution Channel

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Salad

Dressings & Mayonnaise Market:

Estimates & Forecast Trend Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Salad Dressings & Mayonnaise Market Introduction

11.1.2.

Asia

Pacific Salad Dressings & Mayonnaise Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Ingredient Source

11.1.2.3.

By Packaging Type

11.1.2.4.

By Distribution Channel

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Salad

Dressings & Mayonnaise Market:

Estimates & Forecast Trend Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Salad Dressings & Mayonnaise Market Introduction

12.1.2. Middle

East & Africa

Salad Dressings & Mayonnaise Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Ingredient Source

12.1.2.3.

By Packaging Type

12.1.2.4.

By Distribution Channel

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Salad Dressings & Mayonnaise Market:

Estimates & Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Salad

Dressings & Mayonnaise Market Introduction

13.1.2. Latin America Salad

Dressings & Mayonnaise Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

13.1.2.1.

By Type

13.1.2.2.

By Ingredient Source

13.1.2.3.

By Packaging Type

13.1.2.4.

By Distribution Channel

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Salad Dressings

& Mayonnaise Market Product Mapping

15.2. Global Salad Dressings

& Mayonnaise Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

15.3. Global Salad Dressings

& Mayonnaise Market Tier Structure Analysis

15.4. Global Salad Dressings

& Mayonnaise Market Concentration & Company Market Shares (%) Analysis,

2024

16.

Company

Profiles

16.1.

Kraft Heinz Company

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2.

Nestlé

16.3.

McCormick & Company

16.4.

The J.M. Smucker Company

16.5.

Unilever

16.6.

Kewpie Corporation

16.7.

Nando's

16.8.

Veeba Professional

16.9.

Ken's Foods

16.10.

Naturally Fresh

16.11.

Sir Kensington's

16.12.

Primal Kitchen

16.13.

Tessemae's

16.14.

Bolthouse Farms

16.15.

Briannas Fine Salad Dressings

16.16.

Litehouse Inc.

16.17.

Marzetti Company

16.18.

Walden Farms

16.19.

Newman's Own

16.20.

Stonewall Kitchen

16.21.

Others

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables