Soybean Food & Beverage Products Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Soybean Food Products, Soybean Additives/Ingredients, Soybean Oil), By Application (Bakery & Confectionery, Animal Feed, Dairy Products, Functional Food & Supplements, Meat Products, Infant Foods, Other Applications), By Source (GM, Non-GM/GE), By Distribution Channel (Supermarkets, Hypermarkets, Specialty Stores, Online Retailers, Convenience Stores, Departmental Stores, Other Distribution Channels), and Geography

2025-12-18

Consumer Products

Jaya Bundele (Research Analyst)

Description

Soybean

Food & Beverage Products Market Overview

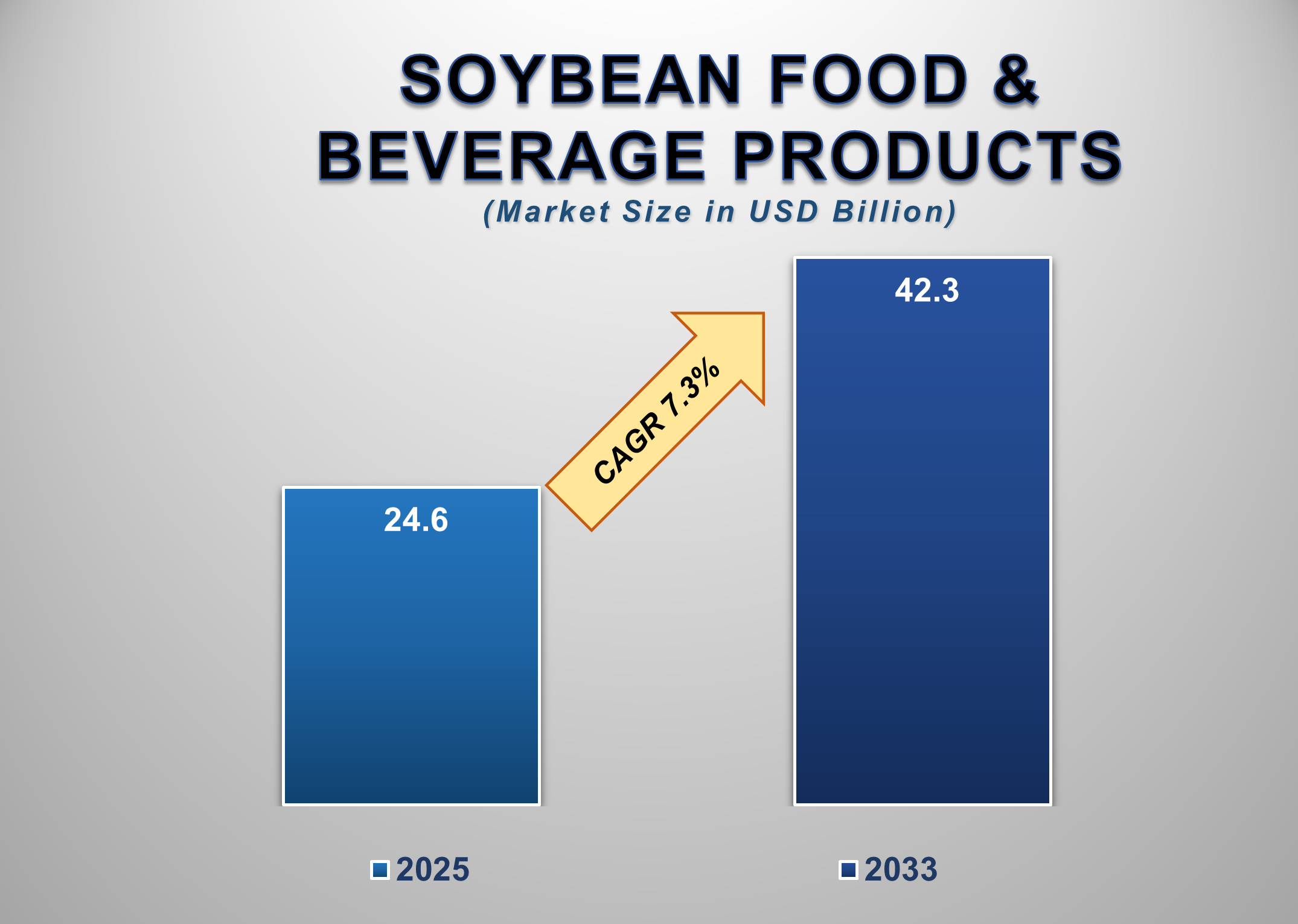

The Global Soybean Food & Beverage Products Market is projected to grow from USD 24.6 billion in 2025 to USD 42.3 billion by 2033, registering a CAGR of 7.3% during the forecast period. The growth is primarily driven by the rising shift toward plant-based diets, increasing demand for protein-rich food products, and the expanding use of soy derivatives across bakery, dairy alternative, functional food, and meat substitute applications. As consumers become more health-conscious and aware of sustainable food sources, soybean-based ingredients are gaining significant traction due to their high protein content, essential amino acids, and low environmental footprint.

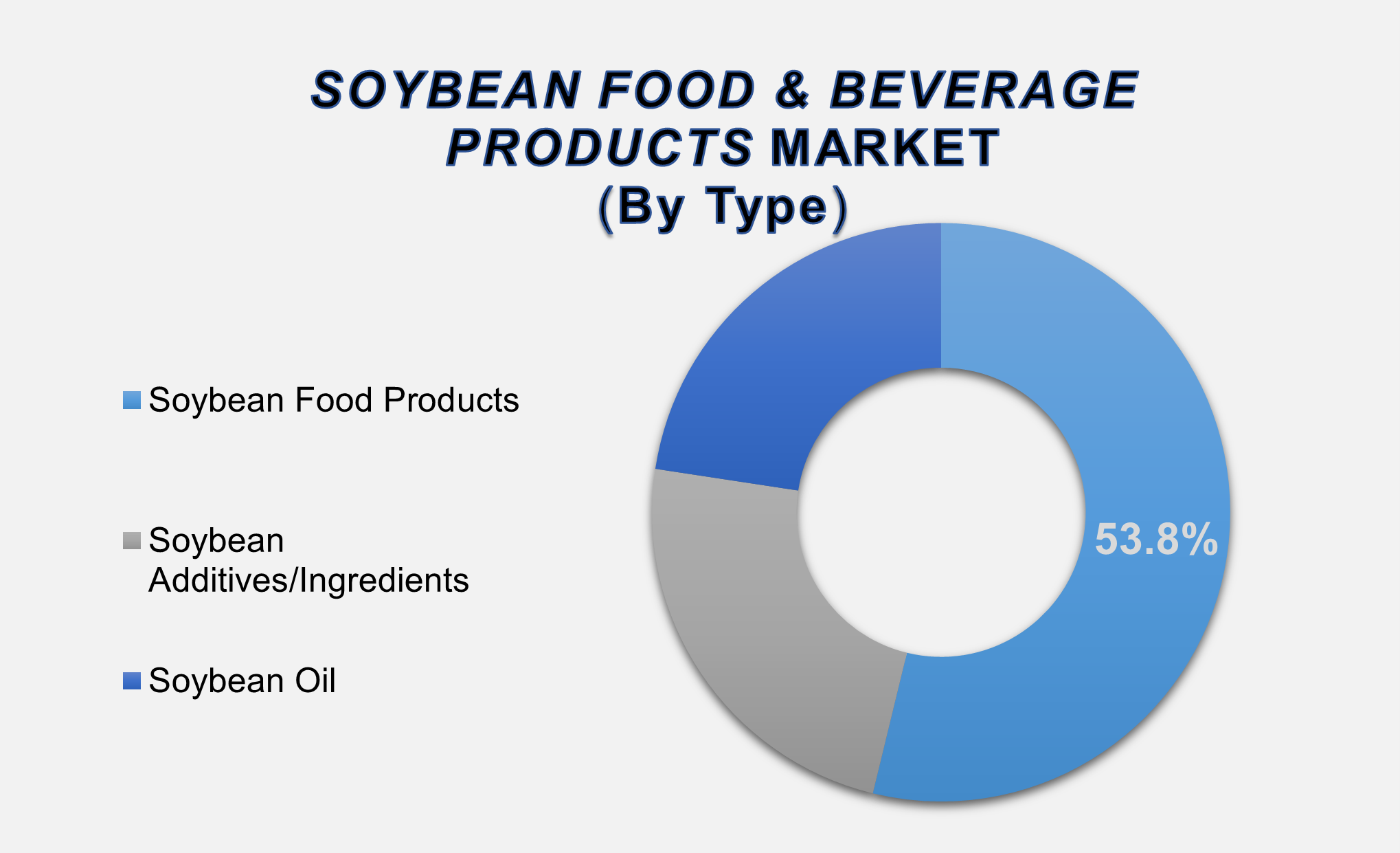

Soybean food products currently

account for 53.8% of the market share, supported by the rapid expansion of

ready-to-eat soy foods, tofu, tempeh, soy milk, textured vegetable protein

(TVP), and soy-based meat analogues. From a sourcing standpoint, GM soybeans

dominate the supply chain, driven by their strong global availability, higher

yield efficiency, and cost-effectiveness.

Soybean

Food & Beverage Products Market Drivers and Opportunities

Rising Plant-Based Food

Adoption Is Driving the Growth of the Soybean Food & Beverage Products

Market

A significant factor driving the

growth of the Soybean Food & Beverage Products Market is the exponential

rise in plant-based and vegan food consumption worldwide. As consumers

increasingly shift away from traditional animal-derived products due to health,

ethical, and environmental concerns, soybean-based foods have emerged as one of

the most widely adopted alternatives due to their versatility and nutritional

richness. Soybean food products offer complete proteins comparable to animal

protein, making them ideal for vegan diets, high-protein diets, sports

nutrition, and weight management applications. In addition, rising cases of

lactose intolerance and dairy allergies are further boosting the demand for

soy-based dairy alternatives such as soy milk, soy yogurt, soy cheese, and soy

protein beverages. Manufacturers are also focusing heavily on new product

innovations, including flavored soy beverages, fortified soy snacks, organic

tofu, and soy-based meat substitutes, appealing to both health-conscious consumers

and flexitarian populations.

Government initiatives supporting

sustainable farming and the promotion of plant-based protein sources are also

contributing to market expansion. As the global food industry moves toward

cleaner labels and environmentally friendly products, soy-based foods are

gaining mainstream acceptance across supermarkets, online retail platforms,

restaurants, and food service chains, significantly driving market growth.

Increasing Use of Soy

Ingredients in Functional Foods and Nutraceuticals Is Driving Market Expansion

Another major driver shaping the

market is the expanding application of soy-derived ingredients in functional

foods, dietary supplements, sports nutrition, and nutraceutical formulations.

Soy protein isolates, concentrates, fibers, and oils are increasingly used by

manufacturers to enhance nutritional value, improve product texture, and

deliver targeted health benefits. Consumers are increasingly demanding products

that support heart health, hormonal balance, weight management, and muscle

development, all areas where soy ingredients have scientifically supported

advantages.

Soy isoflavones, in particular,

are gaining attention for their antioxidant and anti-inflammatory properties,

driving their incorporation into supplements focused on women’s health,

menopausal support, and bone strength. Meanwhile, soy lecithin and soy fiber

are becoming widely used in bakery, confectionery, beverage, and snacking

applications due to their emulsifying and stabilizing properties.

The growth of the fitness and

wellness industry, coupled with rising consumer interest in clean-label and

plant-derived supplements, is making soy one of the most preferred sources of

alternative protein. Food manufacturers, sports nutrition brands, and dietary

supplement companies are significantly expanding their portfolios, further

fueling demand for soybean ingredients across global markets.

Growth of Sustainable and

Clean-Label Products Is Creating Significant Opportunities in The Global

Soybean Food & Beverage Products Market

The rising consumer preference

for sustainable, environmentally friendly, and clean-label food products

presents a major opportunity for the soybean food and beverage industry. As

concerns over climate change and resource-intensive livestock farming grow,

plant-based proteins are increasingly being recognized as a sustainable

alternative. Soybeans require significantly less land, water, and energy to

produce compared to animal protein sources, making them highly attractive to

eco-conscious consumers and global food manufacturers working to lower carbon

footprints. Additionally, the increasing availability of non-GMO and organic

soybean products is opening new avenues for premium food categories and

natural-label products. Health-conscious consumers are increasingly seeking soy

foods that are minimally processed, free from artificial additives, and

responsibly sourced—which is driving innovation in organic tofu, non-GMO soy

milk, soy-based nutritional snacks, and allergen-friendly soy ingredients.

Furthermore, food brands are

exploring the use of soy protein in next-generation plant-based meat products

as they attempt to mimic the texture and sensory properties of animal meat.

With restaurant chains and food service companies expanding meat-free menus

globally, soybean-based ingredients are positioned to gain substantial growth

momentum in the coming years.

Soybean Food & Beverage

Products Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 24.6 Billion |

|

Market Forecast in 2033 |

USD 42.3 Billion |

|

CAGR % 2025-2033 |

7.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Type,

Application, Source, Distribution Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Soybean Food & Beverage

Products Market Report Segmentation Analysis

The Soybean Food & Beverage

Products Market is segmented by Type, by Application, by Source, by

Distribution Channel, and by Geography.

The Soybean Food Products

Segment Accounted for the Largest Market Share

Soybean Food Products accounted

for the largest market share of 53.8%, driven by strong consumer demand for

plant-based, protein-rich, and sustainable food options. This segment includes

tofu, soy milk, tempeh, textured vegetable protein (TVP), soy snacks, fermented

soy foods, and emerging plant-based meat analogues, all experiencing strong

growth due to rising health awareness and shifting dietary preferences. These

products appeal to vegetarians, vegans, and flexitarians seeking healthier

alternatives to meat and dairy. Increased product availability across

supermarkets, hypermarkets, and online platforms is further strengthening

segment penetration. Manufacturers are also innovating with flavored tofu,

fortified soy beverages, organic soy snacks, and non-GMO variants, broadening

consumer appeal. With nutritional superiority, affordability, and broad

culinary versatility, soybean food products will continue to dominate the

market throughout the forecast period.

The Bakery & Confectionery

Segment Accounted for the Largest Share in the Global Soybean Food &

Beverage Products Market

The Bakery & Confectionery

segment accounted for the largest share of the Soybean Food & Beverage

Products Market, driven by the increasing use of soy derivatives such as soy

flour, soy protein concentrates, soy lecithin, and defatted soy in baked goods

and confectionery items. Soy ingredients offer functional benefits such as

improved dough handling, enhanced texture, extended shelf life, and better

moisture retention, making them highly preferred by commercial bakery

manufacturers. In confectionery applications, soy lecithin acts as an excellent

emulsifier, improving viscosity, product smoothness, and cocoa butter reduction

in chocolates. Rising demand for protein-enriched bakery foods, gluten-free

formulations, and plant-based snacks has further strengthened soy adoption. Soy

flour and soy protein isolates are widely incorporated into bread, cookies,

cakes, pastries, protein bars, and sugar confectionery products to boost

nutritional value. With consumers increasingly seeking high-protein,

fiber-rich, and clean-label bakery items, manufacturers are innovating with

soy-enriched variants across mainstream and premium product lines.

GM Soybeans Dominated the

Source Segment

GM Soybeans held the dominant

share of the source segment due to their extensive global production, high

yield efficiency, and cost-effectiveness. GM crops provide strong resistance to

pests and environmental stress, ensuring a stable supply for food, beverage,

and animal feed industries. Their competitive pricing and large-scale

availability make them the preferred choice for mass manufacturing of soy

products such as soy protein, soy oil, soy lecithin, and soy flour. While

demand for non-GMO soy is rising in premium, organic, and clean-label

categories, GM soy’s efficiency advantages continue to support its widespread

use in mainstream food production. The segment is expected to maintain its

leadership over the forecast period.

The following segments are

part of an in-depth analysis of the global Soybean Food & Beverage Products

Market:

|

Market

Segments |

|

|

By Type |

●

Soybean Food

Products ●

Soybean

Additives/Ingredients ●

Soybean Oil |

|

By Application |

●

Bakery &

Confectionery ●

Animal Feed ●

Dairy Products ●

Functional Food

& Supplements ●

Meat Products ●

Infant Foods ●

Other Applications |

|

By Source |

●

GM ●

Non-GM/GE |

|

By

Distribution Channel |

●

Supermarkets ●

Hypermarkets ●

Specialty Stores ●

Online Retailers ●

Convenience stores ●

Departmental stores ●

Other Distribution

Channels |

Soybean Food & Beverage Products Market Share

Analysis by Region

The North America region is

projected to hold the largest share of the global Soybean Food & Beverage

Products market over the forecast period.

North America dominated the

market with a 40.1% share, driven by strong demand for plant-based foods,

robust processing infrastructure, and high consumer acceptance of soy-based

dairy alternatives, snacks, and meat substitutes. The United States leads the

region, supported by sophisticated retail distribution, rapid product

innovation, and the significant presence of global manufacturers such as ADM,

Cargill, DuPont, and WhiteWave Foods.

Asia-Pacific, however, is

expected to record the highest CAGR during the forecast period. Soy foods are

deeply rooted in regional diets, particularly in China, Japan, Indonesia, and

South Korea, where tofu, soy milk, tempeh, and edamame are consumed regularly.

Rising disposable incomes, urbanization, and health awareness further support

market growth. APAC also benefits from strong soybean farming, processing, and

supply chain presence. Europe shows solid growth driven by veganism and the

rise of flexitarian diets, while Latin America and the Middle East & Africa

are gradually expanding due to rising health consciousness and increased market

penetration of functional foods.

Soybean Food & Beverage

Products Market Competition Landscape Analysis

The market is

moderately fragmented, with companies focusing on production expansion, non-GMO

product development, sustainability-led sourcing, and new product innovation.

Key players include Archer Daniels Midland, Cargill, DuPont, Kerry Group, The

Scoular Company, Fuji Oil Group, House Foods Group, WhiteWave Foods, Eden

Foods, Pulmuone, Dean Foods, Hain Celestial Group, Northern Soy, American Soy

Products, Sanitarium Health and Wellbeing, Sojaprotein, Soy Austria, Alpro,

Vitasoy, and Kikkoman. These companies are investing in plant-based product

launches, organic soy expansions, and fortified food formulations to strengthen

market presence.

Global Soybean Food & Beverage Products Market Recent

Developments News:

- In April 2025, COFCO

International expanded its Brazilian operations through strategic hiring

and the construction of a new export terminal, strengthening its

end-to-end agricultural supply chain and enhancing its global trade

footprint.

- In February 2023, Morinaga

Nutritional Foods acquired Tofurky, boosting its tofu production

capabilities and diversifying its plant-based product portfolio to meet

growing consumer demand.

- In March 2022, Otsuka

Pharmaceuticals introduced SOYJOY Nutrition Bars, a line of soy-based

snack bars designed to offer convenient, health-conscious nutrition for

on-the-go consumers.

The Global Soybean Food & Beverage Products Market

is dominated by a few large companies, such as

●

Archer Daniels Midland

●

Cargill

●

DuPont

●

Kerry Group

●

The Scoular Company

●

Fuji Oil Group

●

House Foods Group

●

WhiteWave Foods

●

Eden Foods

●

Pulmuone

●

Dean Foods

●

Hain Celestial Group

●

Northern Soy

●

American Soy Products

●

Sanitarium Health and

Wellbeing

●

Sojaprotein

●

Soy Austria

●

Alpro

●

Vitasoy

●

Kikkoman

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Soybean Food &

Beverage Products Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Soybean Food & Beverage Products Market Scope and Market Estimation

1.2.1.Global Soybean Food &

Beverage Products Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global Soybean Food &

Beverage Products Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Soybean

Food & Beverage Products Market

1.3.2.Application of Global Soybean

Food & Beverage Products Market

1.3.3.Source of Global Soybean

Food & Beverage Products Market

1.3.4.Distribution Channel of

Global Soybean Food & Beverage Products Market

1.3.5.Region of Global Soybean

Food & Beverage Products Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Soybean Food & Beverage Products Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Soybean Food & Beverage Products Market

Estimates & Historical Trend Analysis (2020 - 2024)

4.

Global Soybean Food &

Beverage Products Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Soybean Food & Beverage Products Market Revenue (US$ Bn) Estimates and

Forecasts, by Type, 2020 - 2033

4.1.1.Soybean Food Products

4.1.2.Soybean

Additives/Ingredients

4.1.3.Soybean Oil

5.

Global Soybean Food &

Beverage Products Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Soybean Food & Beverage Products Market Revenue (US$ Bn) Estimates and

Forecasts, by Application, 2020 - 2033

5.1.1.Bakery & Confectionery

5.1.2.Animal Feed

5.1.3.Dairy Products

5.1.4.Functional Food &

Supplements

5.1.5.Meat Products

5.1.6.Infant Foods

5.1.7.Other Applications

6.

Global Soybean Food &

Beverage Products Market Estimates

& Forecast Trend Analysis, by Source

6.1.

Global

Soybean Food & Beverage Products Market Revenue (US$ Bn) Estimates and

Forecasts, by Source, 2020 - 2033

6.1.1.GM

6.1.2.Non-GM/GE

7.

Global Soybean Food &

Beverage Products Market Estimates

& Forecast Trend Analysis, by Distribution Channel

7.1.

Global

Soybean Food & Beverage Products Market Revenue (US$ Bn) Estimates and

Forecasts, by Distribution Channel, 2020 - 2033

7.1.1.Supermarkets

7.1.2.Hypermarkets

7.1.3.Specialty Stores

7.1.4.Online Retailers

7.1.5.Convenience stores

7.1.6.Departmental stores

7.1.7.Other Distribution

Channels

8. Global

Soybean Food & Beverage Products Market

Estimates & Forecast Trend Analysis, by region

1.1.

Global

Soybean Food & Beverage Products Market Revenue (US$ Bn) Estimates and

Forecasts, by region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

9. North America Soybean

Food & Beverage Products Market:

Estimates & Forecast Trend Analysis

9.1.

North

America Soybean Food & Beverage Products Market Assessments & Key

Findings

9.1.1.North America Soybean Food

& Beverage Products Market Introduction

9.1.2.North America Soybean Food

& Beverage Products Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

9.1.2.1. By Type

9.1.2.2. By Application

9.1.2.3. By Source

9.1.2.4. By Distribution

Channel

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Soybean

Food & Beverage Products Market:

Estimates & Forecast Trend Analysis

10.1.

Europe

Soybean Food & Beverage Products Market Assessments & Key Findings

10.1.1.

Europe

Soybean Food & Beverage Products Market Introduction

10.1.2.

Europe

Soybean Food & Beverage Products Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Type

10.1.2.2. By Application

10.1.2.3. By Source

10.1.2.4. By Distribution

Channel

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Soybean

Food & Beverage Products Market:

Estimates & Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Soybean Food & Beverage Products Market Introduction

11.1.2.

Asia

Pacific Soybean Food & Beverage Products Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By Application

11.1.2.3. By Source

11.1.2.4. By Distribution

Channel

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Soybean

Food & Beverage Products Market:

Estimates & Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Soybean Food & Beverage Products

Market Introduction

12.1.2.

Middle East & Africa Soybean Food & Beverage Products

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Type

12.1.2.2. By Application

12.1.2.3. By Source

12.1.2.4. By Distribution

Channel

12.1.2.5.

By

Country

12.1.2.5.1. South

Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi

Arabia

12.1.2.5.4. Rest

of MEA

13. Latin America

Soybean Food & Beverage Products Market: Estimates & Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Soybean Food & Beverage Products Market Introduction

13.1.2.

Latin

America Soybean Food & Beverage Products Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

13.1.2.1. By Type

13.1.2.2. By Application

13.1.2.3. By Source

13.1.2.4. By Distribution

Channel

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Soybean Food & Beverage Products Market Product Mapping

15.2.

Global

Soybean Food & Beverage Products Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

15.3.

Global

Soybean Food & Beverage Products Market Tier Structure Analysis

15.4.

Global

Soybean Food & Beverage Products Market Concentration & Company Market

Shares (%) Analysis, 2023

16.

Company

Profiles

16.1. Archer

Daniels Midland

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2. Cargill

16.3. DuPont

16.4. Kerry Group

16.5. The Scoular

Company

16.6. Fuji Oil

Group

16.7. House Foods

Group

16.8. WhiteWave

Foods

16.9. Eden Foods

16.10. Pulmuone

16.11. Dean Foods

16.12. Hain

Celestial Group

16.13. Northern Soy

16.14. American Soy

Products

16.15. Sanitarium

Health and Wellbeing

16.16. Sojaprotein

16.17. Soy Austria

16.18. Alpro

16.19. Vitasoy

16.20. Kikkoman

16.21. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables